The WCA VICTORY PORTFOLIO seeks capital appreciation through a value-driven, flexible-mandate. Candidate companies may vary in size, sector, and style. When fully invested, the portfolio seeks to invest in 20-30 companies that are:

Growing

Portfolio candidates should have a demonstrated ability to grow shareholder value over time. The compounding effect of profitable growth is a powerful driver to returns and why this is a primary focus of our analysis.

Consistently Profitable

Not all growth is good growth. Growth can be achieved from unprofitable investments, but detracts from shareholder wealth over time. Therefore, we seek businesses that are demonstrating the profitable use of capital in generating cash flow and returns to investors.

Well-Capitalized

Companies should have relatively low amounts of debt. As a general rule, we believe that companies with less debt on the balance sheet have greater financial flexibility. This flexibility becomes even more valuable during periods of economic distress.

Attractively Valued

Candidate companies should trade at a discount to our estimate of intrinsic value under a set of conservative assumptions. In so doing, we hope to establish a “margin of safety” that helps us to avoid unnecessary risk without sacrificing return. In situations where valuations do not reflect underlying risk, the portfolio may hold cash.

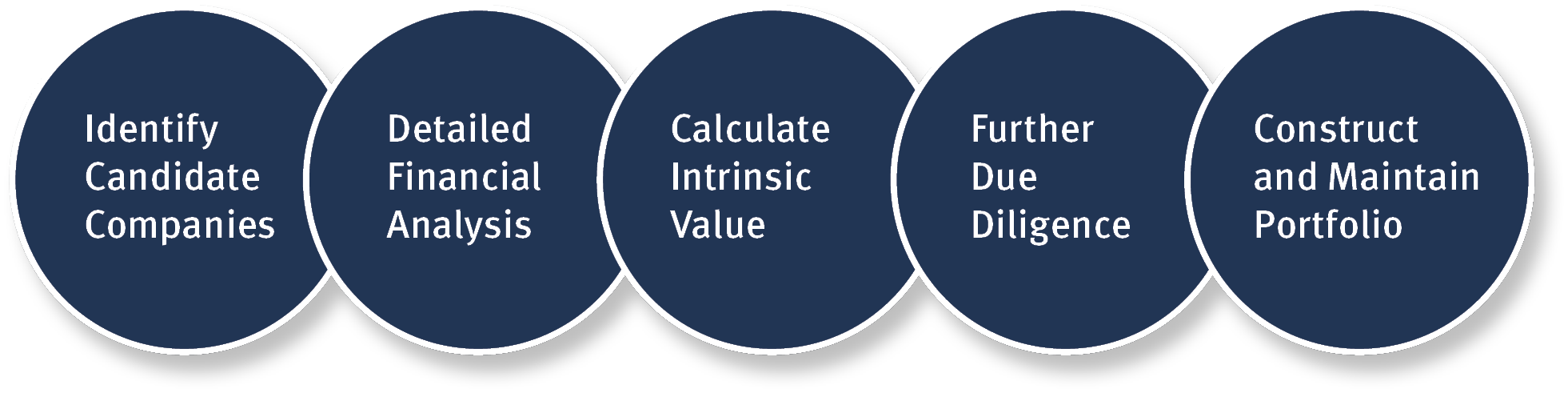

Investment Process

From a universe of over 1,500 companies, we identify those that appear to be consistently profitable, growing, and well-capitalized firms. Candidate companies are subjected to a detailed financial analysis and quantitative valuation process in an effort to establish a reasonable estimate of intrinsic value. We consider qualitative aspects, including industry dynamics, competitive forces, and management quality, as part of a further due diligence process. Portfolios are constructed of 20-30 securities when fully invested with a typical position size near 4%. In situations where we are unable to find investments that meet our criteria, we may seek opportunities elsewhere or hold cash as appropriate. We will sell a security if the price moves beyond our assessment of value, long-run fundamental prospects decline, or if the balance sheet becomes excessively risky. We will continue to hold a security if the company’s earnings power and our assessment of value rises ahead of the stock price.

Our discipline is simple, rigorous, and systematic. We believe the wisdom of this approach is a key element to our long-run success.

Imagine this: The U.S. economy had a stellar year last year, outperforming Europe with a robust 2.5% growth rate. This is a far better performance than almost anyone imagined. It

At Washington Crossing Advisors (WCA), we go to great lengths describing the high quality businesses selected in our Rising Dividend and Victory equity portfolios. We believe in buying quality companies

Page through any investment brochure, factsheet, or presentation, and you’ll eventually get to the disclosure language claiming “All investing involves risk.” For fixed income investors, credit spreads over risk-free U.S.

Many managers use textbook financial ratios such as return on equity, debt to equity, and earnings per share variability to evaluate the quality and value of a company. However, these

Consistency is a big part of quality. Our search for consistency leads us to companies that generate dependable growth. And the most consistent growth engine of the world’s economy —

The only sure thing in investing is the uncertain.

When we began the year, bearishness was rampant. Most Wall Street forecasters were expecting a recession, and the International Monetary Fund (IMF)

What comes around goes around. What has been going on for the past few years may now be coming to an end. From the pandemic lows of March 2020, low-quality

This morning’s lead story in the Wall Street Journal is about the resilient U.S. economy. According to the report, strong hiring, consumer spending, stock market, and housing trends are all

The S&P 500 is up 8.8% for the year through May 25. So, we should start celebrating a bull market, right?

But look deeper, and a different picture emerges. Take away

Like it or not, debt negotiations and shutdowns are integral to the political process, recurring over the past 50 years. The fear of a budget impasse, shutdown, default, and debt

Consistency is not flashy. Consistency does not take center stage. Consistency does not make headlines. Yet, consistency wins the day when predictability is in short supply, as it is now.

With

Index funds have gathered a devoted following since their debut in the 1970s. According to the Investment Company Institute, passive indexes and exchange-traded funds (ETFs) were 43% of the $29