Equity Risk Premium: What’s It All About?

Page through any investment brochure, factsheet, or presentation, and you’ll eventually get to the disclosure language claiming “All investing involves risk.” For fixed income investors, credit spreads over risk-free U.S. treasuries provide a sense of the interest rate, reinvestment, and credit risk they assume when buying corporate bonds. Along the same lines, stock investors must consider inherent risks in the equity markets when facing investing decisions. The Equity Risk Premium (ERP) indicates the price of risk in equities and is a key metric in determining the appeal of owning stocks versus bonds or other assets at any given time.

What is ERP?

Before diving into the significance and implications of ERP, we should define what it is and how it is calculated. In general, the Equity Risk Premium is driven by macroeconomic uncertainty and general investor appetite or aversion for risk. There are several different ways to calculate or extrapolate what the current market ERP is, but for the purposes of this commentary, we aim to keep things simple by subtracting the 10-year Treasury Yield from the S&P 500 12-Month Forward Earnings Yield. In doing so, we get a general sense of what investors expect to be compensated for buying stocks.

Where Are We Today?

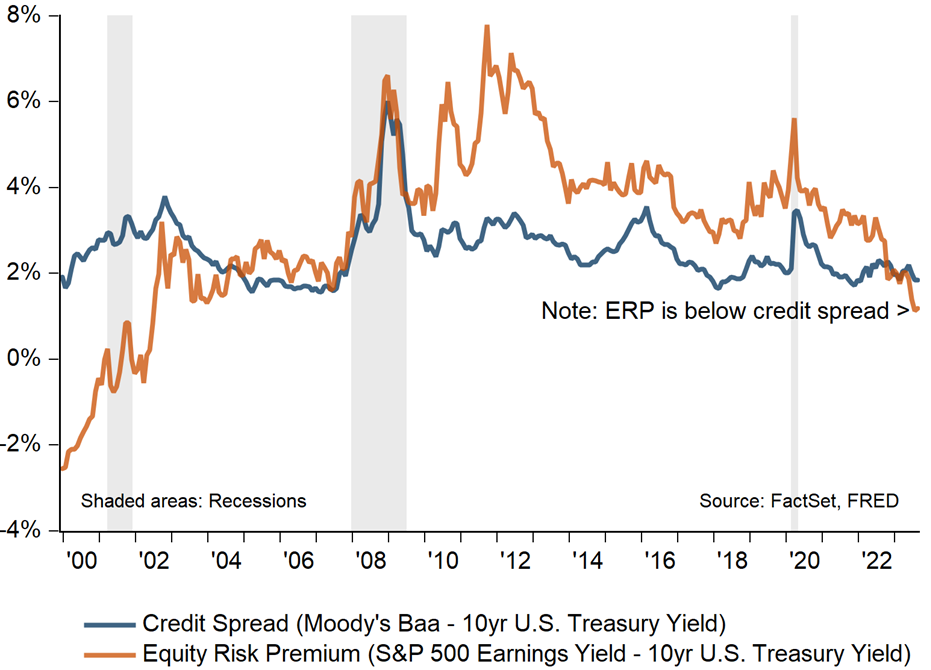

The chart below shows historical Corporate Bond Spreads and ERP calculations in relation to where the metric stands today. As we can see, the risk premium is close to post-Global Financial Crisis lows, even as recession risks have increased. The ERP is indicating a less attractive stock market where investors are not adequately compensated for taking on additional risk. This can be attributed to a few factors, most notably to the rise in 10-year Treasury Yields and lofty stock market valuations. As government bond yields rise, it becomes harder to justify investment in more risky stock assets. Additionally, as company valuations become richer, investors are less willing to take on the added risks of buying expensive equities.

Equity Risk Premium and Corporate Bond Spreads (Baa-UST)

One of the most interesting observations of today’s Equity Risk Premium relates to the bond market. As previously mentioned, the ERP is at a historically low level – so much so, that it is less than investment grade credit spreads over Treasuries. Effectively, investors are being paid a bigger premium to invest in bonds over stocks. If that seems odd, it’s because it is…the relationship is typically reversed.

Portfolio Implications

At Washington Crossing Advisors, we spend a lot of time assessing investment risk across our portfolios. In particular, our Conquest Asset Allocation ETF models make monthly tactical tilts based on macroeconomic inputs, including risk premiums, valuations, and corporate spreads. With the ERP at relative historic lows and high valuations, our tilts have remained neutral, favoring neither stocks nor bonds. As always, we remain vigilant to market conditions and the associated risk premiums that investors have assigned to stocks and bonds.