Truth About “Passive” Investing

Index funds have gathered a devoted following since their debut in the 1970s. According to the Investment Company Institute, passive indexes and exchange-traded funds (ETFs) were 43% of the $29 trillion mutual fund industry. A main selling point of the funds is their “hands-off” nature, requiring little ongoing research or knowledge. But these funds are more active than you might think. While the funds do mirror an index’s composition, the index itself can change a lot. Those changes can be more significant than you think and introduce unwanted risks.

Set and Forget Strategy

An appeal of passive funds is their ease of use. One security promises to cover the exposure to an entire asset class. A typical representation of large domestic companies, such as the S&P 500, is a famous example. Many turn to funds tied to the S&P 500 to “invest in the market.”

According to S&P Dow Jones Indices, the S&P 500 is widely regarded as the best single gauge of U.S. stocks as it covers 80% of the market value of U.S. stocks. The S&P 500 is an essential index because $15.6 trillion is either indexed directly or benchmarked to it, according to S&P Dow Jones. It is generally taken for granted by many that an investment in the S&P 500 is the way to go if you want to own large U.S. stocks. We are not so sure; index funds are often very active despite being marketed as passive.

A committee at S&P Dow Jones selects stocks for the S&P 500. While total value is a primary determinant of inclusion, other factors such as liquidity, profitability, and country focus are also included. Once chosen, the 500 stocks are weighted in the index based on the total value of each stock. A higher weight is assigned to those companies with the highest prices and most outstanding shares. A fund manager, following the index, will direct more and more of your investment into shares as prices go up and sell shares as they get cheaper. Each decade, about 40% of the companies in the index are replaced for one reason or another. This strategy and others that guide most funds invested today are far from static.

Notice there is no link to fundamental factors like earnings or dividends for the S&P 500’s strategy. Without a fundamental connection, daily buys and sells of securities within the index are driven almost entirely by price movements and momentum. The world’s most famous index is essentially an active momentum strategy focused on “winning” stocks. When the S&P 500 is “outperforming” the average stock, it could mean that speculative momentum has taken hold, forcing managers to pour into highly valued shares. Such momentum strategies can work until momentum breaks down and fundamental considerations take over. Incidentally, Washington Crossing Advisors does not use a market capitalization-weighted philosophy in equity portfolios, favoring a more basic approach.

S&P 500 “Strategy” Comparisons

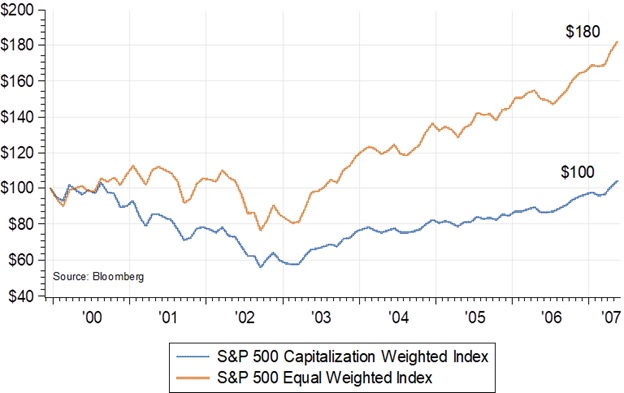

Take, for example, the chart below. It shows the performance of two versions of the S&P 500. One is the traditional version of the index, as described above. The other is a simple version that equally weights the largest 500 companies. The chart covers the December 1999 – October 2007 period because that period sharply contrasts the performance of the market-weighted “strategy” versus the “equal-weighted” strategy. Notice the significant difference in return. A $100 investment in the traditional S&P 500 was about the same in 2007 as in 1999, with a 0% annual return. A $100 investment in a simple equal-weighted version of the S&P 500 was about $180, a 9% return.

As you can see, the “decision” regarding how the portfolio is weighted involves an active choice and ongoing management. The choice can, in some environments, belie the notion that an index fund is the simple “no-brainer” answer that some die-hard indexers believe best solves the investing question. Just because you do not “see” the “action” inside the fund does not mean that “action” is not taking place and those “actions” do matter.

S&P 500 Index (Capitalization Weighted vs Equal Weighted “Strategies”)

Bond Indices, too

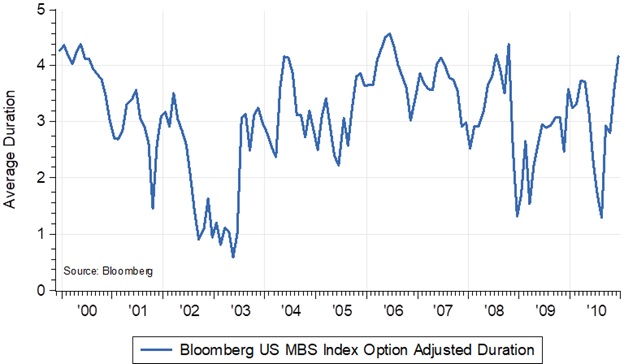

Other indices, generally considered passive, can change in very active ways. Take the popular area of mortgage-backed securities (MBS). These bonds now comprise 20-30% of the entire U.S. bond market and play a significant role in indices that track the bond market. An investor who wants passive exposure could buy a bond index fund to gain exposure to mortgage debt. Even if holdings do not change, a changing rate environment could suddenly and meaningfully alter the risk of bonds in the index.

Take the concept of duration, a primary measure of bond risk that measures the sensitivity of bond prices to changes in interest rates. The duration risk of mortgages held in the Bloomberg U.S. MBS Index, a popular benchmark for mortgage bonds, can change suddenly and in an unintuitive fashion. The chart below shows that mortgage bond duration swung in a wide range from 1 to 4 years. This implies that the fundamental risk factor for the passive index is moving in a very active way.

Fixed Income Risk Factors Change Often, Fast, and Significantly – MBS Option Adjusted Duration

Conclusion

While index funds are popular, you should not assume that the risk factors driving the investment are fixed. In reality, passive funds’ risk exposures can be pretty active. So the alluring idea that investing in such funds is a one-time “set-it-and-forget-it” exercise is misguided. Understanding the changing nature of the risk factors inside the funds remains essential.

Whether investing in individual stocks and bonds or investing in funds, there is no getting around the need to have an active plan for managing a portfolio. For this reason, fundamentals, valuation, and ongoing risk management strategies will remain important considerations. It makes sense to continually ask questions about quality, valuation, and other factors that drive risk and return. And, of course, it is equally important to pay attention to critical changes in your life and what those changes mean for your portfolio.

Passive investing does not mean you should “set it and forget it” because indices are, by nature, active and dynamic. This means that investing a portfolio must be an ongoing active process, no matter how you slice it.