How Trade Policies Lead to U.S. Debt

This is a third part of a series on China and trade. Part one, click here. Part two, click here.

From the early 2000s up to the financial crisis, debt levels surged in the United States. Borrowing allowed American households to consume not only from current income but from future income as well. The economy surged, but the borrowing led to problems and slower growth later on. But why did debt surge as it did? One possible explanation is that a growing trade deficit with China, and China’s rising trade surplus with the United States, was a root cause.

Recall that China has long been producing far more than Chinese households consume. Savings, in other words, is just the unconsumed portion of a country’s production. Either this amount gets directed into domestic investment or gets shipped abroad. When China exports more than they import, they run a trade surplus, and China’s trading partners run a trade deficit. China, in essence, imports demand from overseas to soak up excess domestic production and funds the imported demand by buying foreign assets.

It doesn’t stop there, however.

Trade Deficits, Capital Surpluses, and Debt

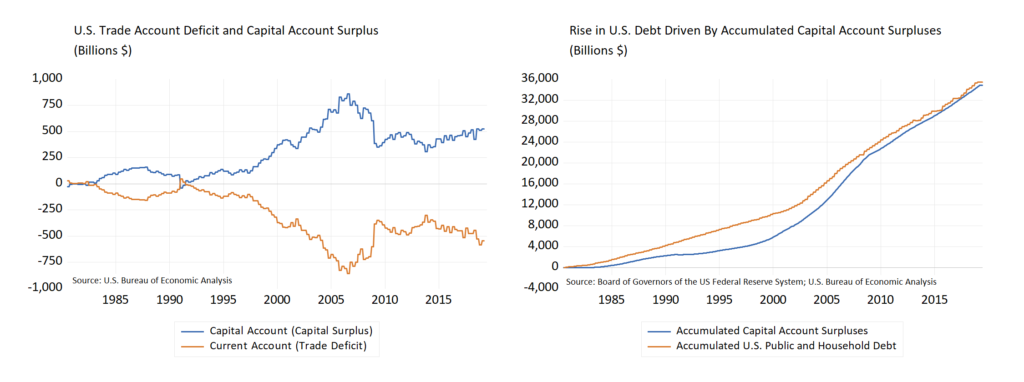

Every dollar the Chinese get in payment for exports must also leave China. Dollars must go because China can only use dollars to purchase something else in dollars abroad or to buy a U.S. asset — typically U.S. government bonds. Because of this simple fact, China’s trade surplus must be matched by an equal amount of capital leaving the country. A capital deficit offsets China’s trade surplus. The United States, on the other hand, runs a trade deficit and a capital surplus (chart, below left).

A persistent deficit must be funded somehow. In the United States, it is easy to see that debt provided much of the funding in recent years. The mortgage boom of the early 2000s and the rise in government debt since 2008 closely matched the accumulated deficit (chart, below right), for example. The surge in U.S. debt can, therefore, be linked directly to trade and trade policies between the United States and China. When China adopts policies that cause them to run a trade surplus against the United States, rising U.S. debt was the natural consequence.

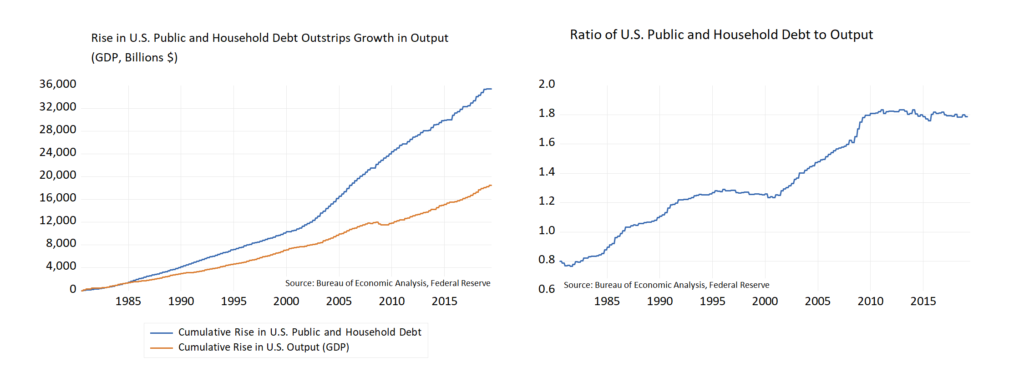

That debt allowed consumption here to rise faster than it would have otherwise and faster than underlying income and output. Rising debt encouraged growth in GDP, but a dollar growth in debt did not equate to a dollar increase in production. Public and household debt in the United States rose by $25 trillion between 2000 and today, but output grew by only $11 trillion (chart, below left). This relationship is not sustainable long-term.

The United States seemed to reach a tipping point in 2010. The rise in U.S. federal government debt after the financial crisis led Standard and Poors’ to downgrade United States’ debt to AA+ from AAA in April 2011. After that, the ratio of debt to GDP leveled out as appetite for more borrowing waned (chart, below right). The United States, in essence, could not or would not continue to incur an ever-rising debt burden since then.

Impact on Interest Rates

In 2005, before he became the Chairman of the U.S. Federal Reserve, Ben Bernanke delivered a speech wherein he laid out his “global savings glut” hypothesis. He said that capital outflows from emerging to advanced economies were responsible for driving up the price of safe assets like government bonds, which also pushed global interest rates down. In essence, trade policies and forced excess savings in places like China were forcing down global interest rates below levels suggested by macroeconomic fundamentals.

If he is right, the fact that much of the global government bond market continues to have negative interest rates seems to point to the continued imbalances. The imbalances lie at the heart of United States-China tension and tensions within the European Union.

Portfolio Implications

There is a clear and well-established link between trade imbalances and debt. Debt has grown far faster than productive capacity both here and in China. This buildup of excess debt is unsustainable over the long-run. The introduction of large amounts of excess debt into the global financial system increases risk, especially for governments, households, and firms that rely on leverage. Leverage creates a fixed cost, interest, and amplifies swings in profitability to owners of assets. Creditors to levered governments, households, and businesses are also at risk as a rise in debt in a borrowers capital structure increases the likelihood of default.

Separately, the period of ultra-low global interest rates is also not likely to persist. If the “global savings glut” proves to be unsustainable — as we expect it eventually will — macroeconomic fundamentals should assert themselves in global bond markets. In this case, it is important to avoid chasing “yield for yield’s sake” investments. Equity investments should be based on the expected future earnings power of businesses, and not based on “current yield.” Careful consideration of a firms capital structure and debt serviceability of the issuer should be paramount in selecting bonds. Lastly, portfolios should be able to adapt to sudden or unexpected fundamental changes in the economy.

Kevin Caron, CFA, Senior Portfolio Manager

Chad Morganlander, Senior Portfolio Manager

Matthew Battipaglia, Portfolio Manager

Steve Lerit, CFA, Client Portfolio Manager

Suzanne Ashley, Analyst

(973) 549-4168

www.washingtoncrossingadvisors.com

www.stifel.com

Disclosures

WCA Fundamental Conditions Barometer Description: We regularly assess changes in fundamental conditions to help guide near-term asset allocation decisions. The analysis incorporates approximately 30 forward-looking indicators in categories ranging from Credit and Capital Markets to U.S. Economic Conditions and Foreign Conditions. From each category of data, we create three diffusion-style sub-indices that measure the trends in the underlying data. Sustained improvement that is spread across a wide variety of observations will produce index readings above 50 (potentially favoring stocks), while readings below 50 would indicate potential deterioration (potentially favoring bonds). The WCA Fundamental Conditions Index combines the three underlying categories into a single summary measure. This measure can be thought of as a “barometer” for changes in fundamental conditions.

The information contained herein has been prepared from sources believed to be reliable but is not guaranteed by us and is not a complete summary or statement of all available data, nor is it considered an offer to buy or sell any securities referred to herein. Opinions expressed are subject to change without notice and do not take into account the particular investment objectives, financial situation, or needs of individual investors. There is no guarantee that the figures or opinions forecasted in this report will be realized or achieved. Employees of Stifel, Nicolaus & Company, Incorporated or its affiliates may, at times, release written or oral commentary, technical analysis, or trading strategies that differ from the opinions expressed within. Past performance is no guarantee of future results. Indices are unmanaged, and you cannot invest directly in an index.

Asset allocation and diversification do not ensure a profit and may not protect against loss. There are special considerations associated with international investing, including the risk of currency fluctuations and political and economic events. Investing in emerging markets may involve greater risk and volatility than investing in more developed countries. Due to their narrow focus, sector-based investments typically exhibit greater volatility. Small company stocks are typically more volatile and carry additional risks, since smaller companies generally are not as well established as larger companies. Property values can fall due to environmental, economic, or other reasons, and changes in interest rates can negatively impact the performance of real estate companies. When investing in bonds, it is important to note that as interest rates rise, bond prices will fall. High-yield bonds have greater credit risk than higher-quality bonds. The risk of loss in trading commodities and futures can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. The high degree of leverage that is often obtainable in commodity trading can work against you as well as for you. The use of leverage can lead to large losses as well as gains.

All investments involve risk, including loss of principal, and there is no guarantee that investment objectives will be met. It is important to review your investment objectives, risk tolerance and liquidity needs before choosing an investment style or manager. Equity investments are subject generally to market, market sector, market liquidity, issuer, and investment style risks, among other factors to varying degrees. Fixed Income investments are subject to market, market liquidity, issuer, investment style, interest rate, credit quality, and call risks, among other factors to varying degrees.

This commentary often expresses opinions about the direction of market, investment sector and other trends. The opinions should not be considered predictions of future results. The information contained in this report is based on sources believed to be reliable, but is not guaranteed and not necessarily complete.

Washington Crossing Advisors LLC is a wholly owned subsidiary and affiliated SEC Registered Investment Adviser of Stifel Financial Corp (NYSE: SF).