The Stock Market: Parallels and Contrasts with 1999

Similarities

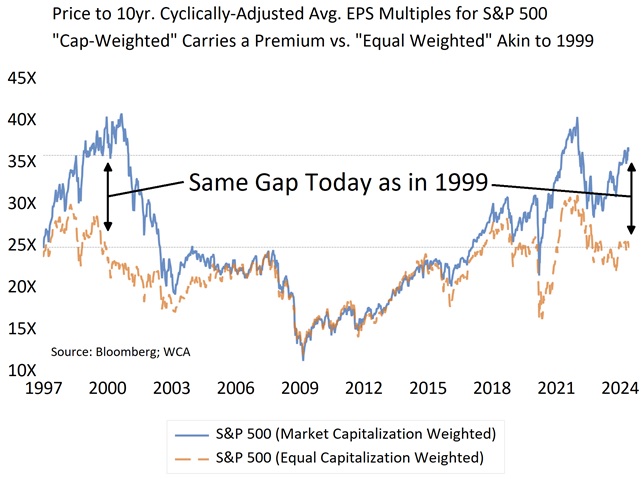

In both 1999 and today, the stock market exhibits strong momentum and a herd mentality, particularly among the largest, most valuable companies. This is evidenced by the significant valuation differential between the market capitalization-weighted S&P 500 index and its equally-weighted counterpart. Currently, this differential is as pronounced as it was in 1999, just before a significant technology stock correction. As we delve deeper, it’s crucial to remember that while trees do not grow to the sky, the same holds true for stock valuations.

Valuations Adjusted for Cyclicality

Valuing stocks using long-run averages of earnings, such as those used in the graph below, helps smooth out short-term volatility and provides a more stable measure of company earnings. Averaging earnings in this way is sometimes called “cyclically adjusted.” This approach offers a clearer picture of valuation by accounting for cyclical fluctuations and reducing the impact of temporary market anomalies. The following chart will illustrate this concept clearly, highlighting the importance of adjusting valuations for cyclicality in today’s environment.

Distortion in Multiples

The current disparity in price-to-earnings multiples between the market capitalization-weighted S&P 500 (blue, solid line) and the equally-weighted S&P 500 (orange, dashed line) highlights the overvaluation of mega-cap stocks. The market cap-weighted index trades at a 16-multiple point premium over the equal-weighted index, reminiscent of the late 1990s.

Historical Context and Consolidation

After the exuberance of the late 1990s, a period of consolidation ensued, where the valuation of average stocks did not rise to meet those of mega-cap growth stocks. Instead, the multiples for leading growth stocks moved lower and converged with the multiple of the “average” company represented by the equal-weighted S&P 500 index. How did this happen? From the end of 1999 to March 2003, the market capitalization-weighted S&P 500 declined by 42%, while the equally-weighted version fell by only 19%. This corrective period began a realignment of multiples between high-growth, high valuation companies and average companies, a trend that persisted well into the late 2010s.

Differences from 1999

Today’s technology companies, unlike many of the unprofitable dot-com businesses of 1999, are highly profitable with strong cash flow and margins. For instance, the cash flow margin for leading tech firms is around 32%, significantly higher than the overall 20% margin for the S&P 500. The broader consumer base and the widespread adoption of annuitized cloud services have reduced some of the cyclicality inherent in the tech sector compared to the 1990s. AI also presents the potential for sustained above-average growth, potentially filling the earnings gap illustrated by the valuation disparity.

Conclusion

Despite the optimism surrounding mega-cap tech stocks, similar to the late 1990s, headwinds are likely to challenge their continued dominance. Investors should consider rebalancing portfolios that drifted or selling overvalued stocks, acknowledging that extraordinary growth rates cannot persist indefinitely. The adage “Trees do not grow to the sky” remains pertinent, suggesting a more cautious approach moving forward. Instead of chasing the sky, it is wiser to plant roots in the ground by buying quality stocks at reasonable prices.