The Illusion of Perpetual Growth

Stock prices are more than numbers on a screen. They tell us what market participants believe. These beliefs are distilled into prices that reveal investors’ changing expectations about the future. The expectations are not those of a CEO or a handful of analysts — they are the aggregate judgment of all the actual buyers and sellers of stocks who set prices each day.

By applying a basic valuation framework[1] to the five hundred largest U.S. companies, we can tease out what the market assumes about long-run growth in perpetuity. This is not about next quarter or even the next decade. It is about what investors seem to collectively believe will happen — now and forever. The recent run-up in high flying growth and AI stocks suggests this is a good time to revisit where growth expectations and valuations intersect.

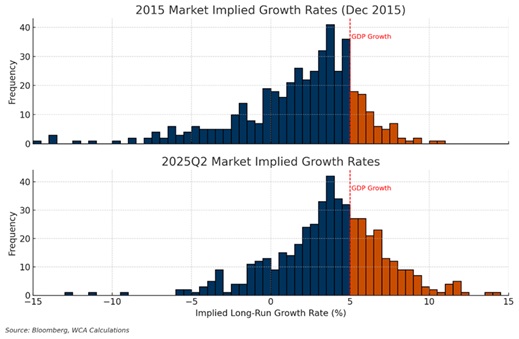

Evolving Growth Expectations (2015 vs. 2025)

The above charts show the distribution of growth expectations priced into S&P 500 stocks in 2015 and now. We show that there are far more companies today whose valuations are predicated upon realization of growth rates well beyond the growth that the economy is likely to deliver. In the charts, a red dashed line marks 5 percent and is labeled “GDP Growth.” That marker is not arbitrary. In the past decade, U.S. nominal GDP grew at an average annual rate of roughly 5.4 percent; looking ahead, the Congressional Budget Office projects nominal GDP closer to 4 percent over the coming decade. Against that backdrop, the market’s current pricing is striking. When more growth expectations exceed this level of about 5%, we believe the chances for disappointment grow and losses can be significant. This is why we maintain conservative growth estimates when valuing companies.

A decade ago, the market was conservatively estimating growth. For example, in 2015, the market implied perpetuity growth rate baked into S&P 500 companies’ valuations clustered around a reasonable 3–5 percent (blue bars in the top chart above), with only a minority priced above the economy’s long-run growth (orange bars). Roughly seven in ten firms were priced with growth expectations at or below overall GDP growth. The market’s center of gravity sat near the system’s anchor.

Today the distribution looks very different (bottom chart above). Growth expectations are now much higher on average, and there is a far thicker concentration of companies with growth expectations above the economy’s trend (orange bars). A large share of firms now rests on the assumption that growth will outpace GDP in perpetuity. Looked at by market capitalization (rather than numbers of companies), the tilt is even more pronounced: over 60% of the S&P 500 index value is priced as if superior growth can be sustained forever, with a meaningful slice (about $8 trillion in market value) priced with an implied perpetuity growth assumption above 10%.

The Problem with Perpetuity

Here is the central problem: no company can grow faster than the economy forever. The math simply will not allow it. A firm compounding at 10 percent while the economy grows at 5 percent eventually overtakes the economy itself — an impossibility. Compounding exposes the flaw.

History points the same way. Champions of one era rarely dominate the next. Competition, technology, and regulation erode even the strongest franchises. IBM, Intel, General Electric, General Motors — each at times seemed impervious to the law of large numbers and competition. But each one aged in time and growth slowed. Yet the market periodically assumes a new “fountain of youth” for a new crop of companies, but ascent, challenge, and mean reversion will remain the rule. Over time, growth must converge toward the pace of the economy and system as a whole.

What the Market Is Really Saying

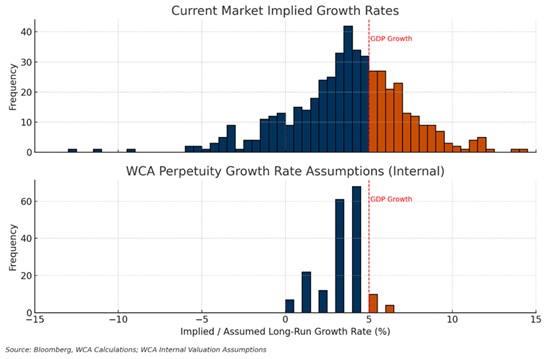

If above-GDP growth “in perpetuity” is impossible, what do today’s prices mean? They reflect optimism and imprecision—the belief that a few special firms can maintain extraordinary advantages for an unusually long time, as if forever. We see this in the evolution of the graph above. The graph also shows that distribution also has a heavy left tail: some companies are priced as if they will shrink indefinitely. This polarization — exuberance for perceived “permanent” winners and resignation about “permanent” losers — is a snapshot of sentiment, not an equilibrium that can endure.

Washington Crossing Advisors’ Approach

To highlight the contrast, we now show two distributions (chart below): the current market-implied growth for the S&P 500 companies and Washington Crossing Advisors’ own internal assumptions used in our intrinsic-value work on high quality dividend growth stocks, which we identify using the WCA High Quality Index. While many companies are being priced with heady growth expectations, we use far more conservative assumptions — generally clustered around 3–5 percent, with very few of our assumptions set above estimated long-run GDP growth (5 percent). The aim here is straightforward: reduce the risk of overpaying for narratives that require impossible things to happen. If market valuations later realign with more realistic expectations, we expect better entry points for quality firms currently priced to perfection or beyond.

Today’s Dilemma

For investors, this environment carries opportunity and danger. The danger is apparent: when expectations are stretched, small disappointments can trigger large drawdowns. We saw this in spades in the 2000-2002 market meltdown. The opportunity lies in the other direction: firms priced for secular decline may prove more resilient, offering value precisely because they have been written off.

Perhaps the broader lesson is patience and humility. Prices can and do embed unreasonable growth assumptions, but over time the economy imposes discipline. This is why economics and markets are inextricably tied. Markets’ expected growth must ultimately reconcile with the broader economy’s ability to deliver that growth. Forgetting this invites delusion — and potentially severe and rapid losses when the stock market’s moorings to fundamentals become untethered. And this is precisely why Washington Crossing Advisors maintains a valuation discipline alongside an emphasis on quality and income growth. Where we can buy quality businesses without assuming the impossible, we believe risk and reward are more sensibly aligned.

Footnote

[1] Gordon Growth Model (Enterprise View). The Gordon Growth model values a stream of cash flows assuming a constant growth rate into perpetuity. In our application, we take an enterprise-value perspective: we subtract the cash-flow-to-EV yield from the firm’s weighted average cost of capital (WACC). The difference is the implied long-run (perpetuity) growth rate embedded in today’s price.

Contacts:

Kevin Caron, CFA, Senior Portfolio Manager

Chad Morganlander, Senior Portfolio Manager

Matthew Battipaglia, Portfolio Manager

Steve Lerit, CFA, Head of Portfolio Risk

Suzanne Ashley, Relationship Manager

Eric Needham, Sales Director

Jeff Battipaglia, Sales and Marketing

(973) 549-4168

www.washingtoncrossingadvisors.com

Disclosures:

WCA Barometer – We regularly assess changes in fundamental conditions to help guide near-term asset allocation decisions. Analysis incorporates approximately 30 forward-looking indicators in categories ranging from Credit and Capital Markets to U.S. Economic Conditions and Foreign Conditions. From each category of data, we create three diffusion-style sub-indices that measure the trends in the underlying data. Sustained improvement that is spread across a wide variety of observations will produce index readings above 50 (potentially favoring stocks), while readings below 50 would indicate potential deterioration (potentially favoring bonds). The WCA Fundamental Conditions Index combines the three underlying categories into a single summary measure. This measure can be thought of as a “barometer” for changes in fundamental conditions.

Standard & Poor’s 500 Index (S&P 500) is a capitalization-weighted index that is generally considered representative of the U.S. large capitalization market.

S&P Global (SPGI) is a leading American provider of financial information, analytics, and credit ratings, headquartered in New York, NY. It operates major divisions including S&P Global Ratings, S&P Global Market Intelligence, S&P Global Commodity Insights, S&P Global Mobility, and S&P Dow Jones Indices.

The ICE BofA U.S. High Yield Index is an unmanaged index that tracks the performance of U.S. dollar denominated, below investment-grade rated corporate debt publicly issued in the U.S. domestic market.

The S&P 500 Growth measures constituents from the S&P 500 that are classified as growth stocks based on three factors: sales growth, the ratio of earnings change to price, and momentum.

The S&P 500 Value Index measures constituents from the S&P 500 that are classified as value stocks based on three factors: the ratios of book value, earnings and sales to price.

The S&P 500 Equal Weight Index is the equal-weight version of the widely regarded Standard & Poor’s 500 Index, which is generally considered representative of the U.S. large capitalization market. The index has the same constituents as the capitalization-weighted S&P 500, but each company in the index is allocated a fixed weight of 0.20% at each quarterly rebalancing.

The WCA Rising Dividend Custom Benchmark is a rules-based benchmark constructed by Washington Crossing Advisors to represent a universe of large capitalization U.S. companies that meet certain quality and dividend growth criteria, including proprietary screens for profitability, earnings consistency, and balance sheet strength, along with minimum market capitalization and dividend growth requirements. The benchmark is reconstituted and rebalanced quarterly and is intended to serve as a style-appropriate benchmark for the WCA Rising Dividend strategy.

The Washington Crossing Advisors’ High Quality Index and Low Quality Index are objective, quantitative measures designed to identify quality in the top 1,000 U.S. companies. Ranked by fundamental factors, WCA grades companies from “A” (top quintile) to “F” (bottom quintile). Factors include debt relative to equity, asset profitability, and consistency in performance. Companies with lower debt, higher profitability, and greater consistency earn higher grades. These indices are reconstituted annually and rebalanced daily. For informational purposes only, and WCA Quality Grade indices do not reflect the performance of any WCA investment strategy.

The risk of loss in trading commodities and futures can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. The high degree of leverage that is often obtainable in commodity trading can work against you as well as for you. The use of leverage can lead to large losses as well as gains.

The information contained herein has been prepared from sources believed to be reliable but is not guaranteed by us and is not a complete summary or statement of all available data, nor is it considered an offer to buy or sell any securities referred to herein. Opinions expressed are subject to change without notice and do not take into account the particular investment objectives, financial situation, or needs of individual investors. There is no guarantee that the figures or opinions forecast in this report will be realized or achieved. Employees of Stifel, Nicolaus & Company, Incorporated or its affiliates may, at times, release written or oral commentary, technical analysis, or trading strategies that differ from the opinions expressed within. Past performance is no guarantee of future results. Indices are unmanaged, and you cannot invest directly in an index.

Asset allocation and diversification do not ensure a profit and may not protect against loss. There are special considerations associated with international investing, including the risk of currency fluctuations and political and economic events. Changes in market conditions or a company’s financial condition may impact a company’s ability to continue to pay dividends, and companies may also choose to discontinue dividend payments. Investing in emerging markets may involve greater risk and volatility than investing in more developed countries. Due to their narrow focus, sector-based investments typically exhibit greater volatility. Small-company stocks are typically more volatile and carry additional risks since smaller companies generally are not as well established as larger companies. Property values can fall due to environmental, economic, or other reasons, and changes in interest rates can negatively impact the performance of real estate companies. When investing in bonds, it is important to note that as interest rates rise, bond prices will fall. High-yield bonds have greater credit risk than higher-quality bonds. Bond laddering does not assure a profit or protect against loss in a declining market. The risk of loss in trading commodities and futures can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. The high degree of leverage that is often obtainable in commodity trading can work against you as well as for you. The use of leverage can lead to large losses as well as gains. Changes in market conditions or a company’s financial condition may impact a company’s ability to continue to pay dividends, and companies may also choose to discontinue dividend payments.

All investments involve risk, including loss of principal, and there is no guarantee that investment objectives will be met. It is important to review your investment objectives, risk tolerance, and liquidity needs before choosing an investment style or manager. Equity investments are subject generally to market, market sector, market liquidity, issuer, and investment style risks, among other factors to varying degrees. Fixed Income investments are subject to market, market liquidity, issuer, investment style, interest rate, credit quality, and call risks, among other factors to varying degrees.

Beta is a measure of the volatility, or systematic risk, of a security or a portfolio relative to the market as a whole. A beta of one is considered as risky as the benchmark and is therefore likely to provide expected returns approximate to those of the benchmark during both up and down periods. A portfolio with a beta of two would move approximately twice as much as the benchmark.

Standard deviation is a measure of the volatility of a security’s or portfolio’s returns in relation to the mean return. The larger the standard deviation, the greater the volatility of return in relation to the mean return.

Changes in market conditions or a company’s financial condition may impact a company’s ability to continue to pay dividends, and companies may also choose to discontinue dividend payments

This commentary often expresses opinions about the direction of market, investment sector, and other trends. The opinions should not be considered predictions of future results. The information contained in this report is based on sources believed to be reliable, but is not guaranteed and not necessarily complete.

The securities discussed in this material were selected due to recent changes in the strategies. This selection criterion is not based on any measurement of performance of the underlying security.

Washington Crossing Advisors, LLC is a wholly-owned subsidiary and affiliated SEC Registered Investment Adviser of Stifel Financial Corp (NYSE: SF). Registration with the SEC implies no level of sophistication in investment management.