Quality First

There is lots of discussion about the return of speculation. Cryptocurrencies, message board short-squeezes, soaring penny stocks, “blank check” companies, and record issuance of risky debt dominate today’s headlines. It is hard to imagine that, just under a year ago, financial markets were in freefall. Greed replaced fear in the span of a few short months, despite an ongoing pandemic. This week we return our focus to “quality” as a key factor in portfolio construction.

Risk-On!

Notice the chart below. It is a ratio of the most volatile stocks in the S&P 500 divided by the least volatile. When investors are feeling good and loading up on risky stocks, the line rises, and when fearful or uncertain, it falls. Over time, it tends to revert to the mean. Notice how, after November 5, the line shoots straight upward. This “risk-on” condition coincided with both the election and debut of a promising vaccine. These factors, combined with more stimulus expectations, have driven risk appetite to levels not seen in years.

Chart A

Performance of High Beta vs. Low Beta Stocks

Binging on Low Quality

Amid the buying frenzy, a growing number of investors are willing to pay the highest prices for the lowest quality investments. The average yield on U.S. junk bonds dropped below 4% for the first time a week ago, according to a recent Wall Street Journal report. This milestone makes little sense and is why we remain underweight low-quality bonds in tactical asset allocation portfolios. It is also a sign that the forward return for low-quality investments is likely not what it used to be, as yield hungry investors binge on this lowest quality debt.

How We View Quality

Of first importance is the “quality” of an investment. Without it, how can we even begin to figure out whether an investment’s price makes sense? Of course, there are many different definitions of quality. Still, unlike beauty, quality need not be only in the “eye of the beholder.” We can go a long way to quantify it objectively if we ask the right questions.

To us, “quality” is nearly synonymous with “durability.” We come close to capturing this idea by examining a company’s profitability, consistency, and leverage. We expect companies with highly profitable assets to survive better than companies with low profitability during tough times, for example. Similarly, we suspect companies that regularly generate steady cash to be more durable than ones with unpredictable cash flow, especially in tough times. Lastly, more conservatively financed companies with low debt are more likely to endure than those saddled with lots of weighty obligations. Thus, a “quality” firm to us is one with highly profitable assets, consistent cash flows, and low leverage, all else being equal.

Recent Trends

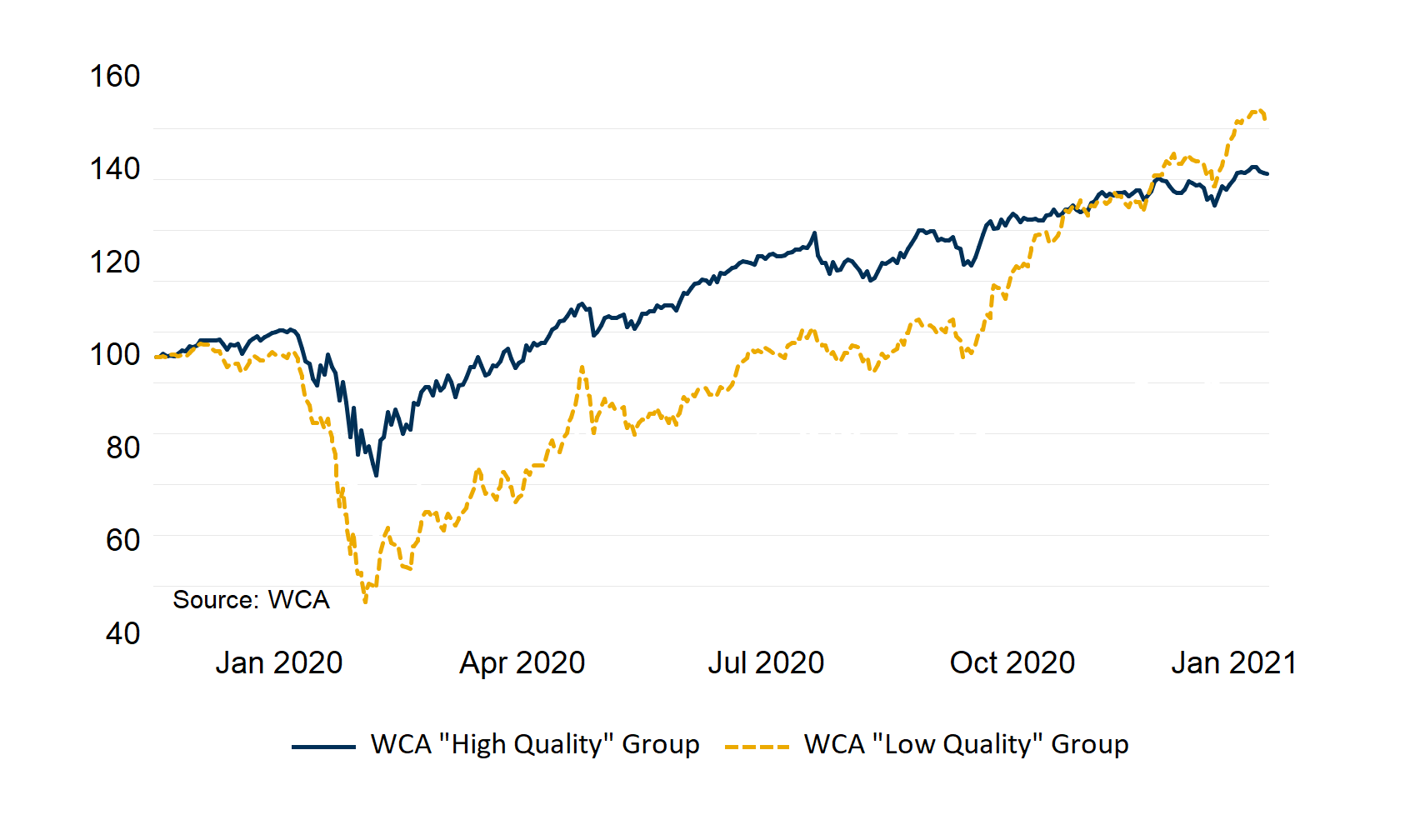

The last year has been a “tale of two markets,” defined mainly by quality. The chart below shows the average price performance of the highest and lowest quality publicly-traded companies in the United States, as judged by Washington Crossing Advisors. To determine quality, we ranked the 1,000 largest along the three dimensions outlined above (profitability, consistency, and leverage). Next, we assigned those companies ranked in the highest 20% across all three areas to Washington Crossing’s (WCA) “High Quality” group. The lowest 20% were assigned to the Washington Crossing “Low Quality” group. We tracked the day-to-day performance of each group’s average, equally-weighted price performance (Chart B, below).

As you can see, the WCA “Low Quality” group recently surged ahead of the WCA “High Quality” group. It is important to note that the overall volatility was far higher over the whole period for lower quality. The “Low Quality” group suffered much more profound losses during the selloff last spring, with losses nearly double that of “High Quality.” As markets swing from fear to greed and back again, the pendulum swings also seem to turn back and forth between low and high quality. Lately, momentum has favored “Low Quality” over “High Quality.”

Graph B

“High” vs. “Low” Quality Recent Performance

January 2020 to February 2021

The Time is Now

While quality may be out of style relative to popular momentum and yield plays for the moment, we are confident the cycle will eventually reverse. For risk-averse investors or investors holding high-momentum stocks, it may pay to focus now on the quality of portfolio holdings. With “high-quality” recently lagging behind “low-quality” stocks, now could be the right time to add higher-quality, lower-momentum investments. History has shown that “quality” has highly desirable characteristics in flat-to-down markets but tends to lag in strongly-trending markets.

As the world again becomes enamored with “fast money,” we remember the lessons of past bull markets and remain steadfast in our commitment to the enduring and oft-overlooked characteristic of “quality.”

S&P 500 — The Standard & Poor’s 500 Index is a capitalization-weighted index that is generally considered representative of the U.S. large capitalization market.

Indices are unmanaged, and it is not possible to invest directly in an index. All benchmark returns presented are provided to represent the investment environment existing during the time periods shown. Actual investment performance will vary due to fees and expenses. For comparison purposes, the benchmarks include the reinvestment of income. The benchmarks are unmanaged and unavailable for direct investment.

The S&P 500 High Beta Index measures the performance of 100 constituents in the S&P 500 that are most sensitive to changes in the market. Constituents are weighted relative to their level of market sensitivity, with each stock assigned a weight proportional to its beta.

The S&P 500 Low Volatility Index measures performance of the 100 least volatile stocks in the S&P 500. The index benchmarks low volatility or low variance strategies for the U.S. stock market. Constituents are weighted relative to the inverse of their corresponding volatility, with the least volatile stocks receiving the highest weights.

Disclosures:

WCA Barometer – We regularly assess changes in fundamental conditions to help guide near-term asset allocation decisions. Analysis incorporates approximately 30 forward-looking indicators in categories ranging from Credit and Capital Markets to U.S. Economic Conditions and Foreign Conditions. From each category of data, we create three diffusion-style sub-indices that measure the trends in the underlying data. Sustained improvement that is spread across a wide variety of observations will produce index readings above 50 (potentially favoring stocks), while readings below 50 would indicate potential deterioration (potentially favoring bonds). The WCA Fundamental Conditions Index combines the three underlying categories into a single summary measure. This measure can be thought of as a “barometer” for changes in fundamental conditions.

Standard & Poor’s 500 Index (S&P 500) is a capitalization-weighted index that is generally considered representative of the U.S. large capitalization market.

The S&P 500® Information Technology comprises those companies included in the S&P 500 that are classified as members of the GICS® information technology sector.

S&P Global (SPGI) is a leading American provider of financial information, analytics, and credit ratings, headquartered in New York, NY. It operates major divisions including S&P Global Ratings, S&P Global Market Intelligence, S&P Global Commodity Insights, S&P Global Mobility, and S&P Dow Jones Indices.

The ICE BofA U.S. High Yield Index is an unmanaged index that tracks the performance of U.S. dollar denominated, below investment-grade rated corporate debt publicly issued in the U.S. domestic market.

The S&P 500 Growth measures constituents from the S&P 500 that are classified as growth stocks based on three factors: sales growth, the ratio of earnings change to price, and momentum.

The S&P 500 Value Index measures constituents from the S&P 500 that are classified as value stocks based on three factors: the ratios of book value, earnings and sales to price.

The S&P 500 Equal Weight Index is the equal-weight version of the widely regarded Standard & Poor’s 500 Index, which is generally considered representative of the U.S. large capitalization market. The index has the same constituents as the capitalization-weighted S&P 500, but each company in the index is allocated a fixed weight of 0.20% at each quarterly rebalancing.

The WCA Rising Dividend Custom Benchmark is a rules-based benchmark constructed by Washington Crossing Advisors to represent a universe of large capitalization U.S. companies that meet certain quality and dividend growth criteria, including proprietary screens for profitability, earnings consistency, and balance sheet strength, along with minimum market capitalization and dividend growth requirements. The benchmark is reconstituted and rebalanced quarterly and is intended to serve as a style-appropriate benchmark for the WCA Rising Dividend strategy.

The Washington Crossing Advisors’ High Quality Index and Low Quality Index are objective, quantitative measures designed to identify quality in the top 1,000 U.S. companies. Ranked by fundamental factors, WCA grades companies from “A” (top quintile) to “F” (bottom quintile). Factors include debt relative to equity, asset profitability, and consistency in performance. Companies with lower debt, higher profitability, and greater consistency earn higher grades. These indices are reconstituted annually and rebalanced daily. For informational purposes only, and WCA Quality Grade indices do not reflect the performance of any WCA investment strategy.

The risk of loss in trading commodities and futures can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. The high degree of leverage that is often obtainable in commodity trading can work against you as well as for you. The use of leverage can lead to large losses as well as gains.

The information contained herein has been prepared from sources believed to be reliable but is not guaranteed by us and is not a complete summary or statement of all available data, nor is it considered an offer to buy or sell any securities referred to herein. Opinions expressed are subject to change without notice and do not take into account the particular investment objectives, financial situation, or needs of individual investors. There is no guarantee that the figures or opinions forecast in this report will be realized or achieved. Employees of Stifel, Nicolaus & Company, Incorporated or its affiliates may, at times, release written or oral commentary, technical analysis, or trading strategies that differ from the opinions expressed within. Past performance is no guarantee of future results. Indices are unmanaged, and you cannot invest directly in an index.

Asset allocation and diversification do not ensure a profit and may not protect against loss. There are special considerations associated with international investing, including the risk of currency fluctuations and political and economic events. Changes in market conditions or a company’s financial condition may impact a company’s ability to continue to pay dividends, and companies may also choose to discontinue dividend payments. Investing in emerging markets may involve greater risk and volatility than investing in more developed countries. Due to their narrow focus, sector-based investments typically exhibit greater volatility. Small-company stocks are typically more volatile and carry additional risks since smaller companies generally are not as well established as larger companies. Property values can fall due to environmental, economic, or other reasons, and changes in interest rates can negatively impact the performance of real estate companies. When investing in bonds, it is important to note that as interest rates rise, bond prices will fall. High-yield bonds have greater credit risk than higher-quality bonds. Bond laddering does not assure a profit or protect against loss in a declining market. The risk of loss in trading commodities and futures can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. The high degree of leverage that is often obtainable in commodity trading can work against you as well as for you. The use of leverage can lead to large losses as well as gains. Changes in market conditions or a company’s financial condition may impact a company’s ability to continue to pay dividends, and companies may also choose to discontinue dividend payments.

All investments involve risk, including loss of principal, and there is no guarantee that investment objectives will be met. It is important to review your investment objectives, risk tolerance, and liquidity needs before choosing an investment style or manager. Equity investments are subject generally to market, market sector, market liquidity, issuer, and investment style risks, among other factors to varying degrees. Fixed Income investments are subject to market, market liquidity, issuer, investment style, interest rate, credit quality, and call risks, among other factors to varying degrees.

Beta is a measure of the volatility, or systematic risk, of a security or a portfolio relative to the market as a whole. A beta of one is considered as risky as the benchmark and is therefore likely to provide expected returns approximate to those of the benchmark during both up and down periods. A portfolio with a beta of two would move approximately twice as much as the benchmark.

Standard deviation is a measure of the volatility of a security’s or portfolio’s returns in relation to the mean return. The larger the standard deviation, the greater the volatility of return in relation to the mean return.

Changes in market conditions or a company’s financial condition may impact a company’s ability to continue to pay dividends, and companies may also choose to discontinue dividend payments

This commentary often expresses opinions about the direction of market, investment sector, and other trends. The opinions should not be considered predictions of future results. The information contained in this report is based on sources believed to be reliable, but is not guaranteed and not necessarily complete.

The securities discussed in this material were selected due to recent changes in the strategies. This selection criterion is not based on any measurement of performance of the underlying security.

Washington Crossing Advisors, LLC is a wholly-owned subsidiary and affiliated SEC Registered Investment Adviser of Stifel Financial Corp (NYSE: SF). Registration with the SEC implies no level of sophistication in investment management.