Next Up: The Fed

The world economy continues to grow at half-speed as emerging economies downshift from a period of rapid and credit-fueled growth. At the same time, developed economies like the United States appear to be growing at a slow-but-steady pace. Before the last recession, emerging economies grew near 9% and developed economies grew near 3%. Today, those growth rates stand nearer to 4% and 1.8%, respectively. The world’s economies are collectively growing at a little more than half as fast as they were just a few years ago.

Financial market conditions are tightening, however, and this introduces some downside risk. Financial market conditions are becoming tighter for commodity-producers and many emerging market countries in particular. Rising funding costs increases the odds that growth slows further in emerging markets. Emerging market banks are tightening lending standards and non-performing loans at banks are on the rise. As the cost of borrowing in emerging markets goes up, it becomes harder for these economies to grow and increases the potential for recessions.

Notably, China’s economy continues to slow, and it is likely that more government policy easing is on the way. Other countries are being forced to actually tighten monetary despite weakness in order to maintain credibility, avoid capital flight and inflation, preserve a stable currency and promote stability. Brazil’s government debt was cut to junk status by Standard & Poor’s last week, for example. The net result of all this is further uncertainty over global growth and increased “tail risk.”

Next Up: The Fed

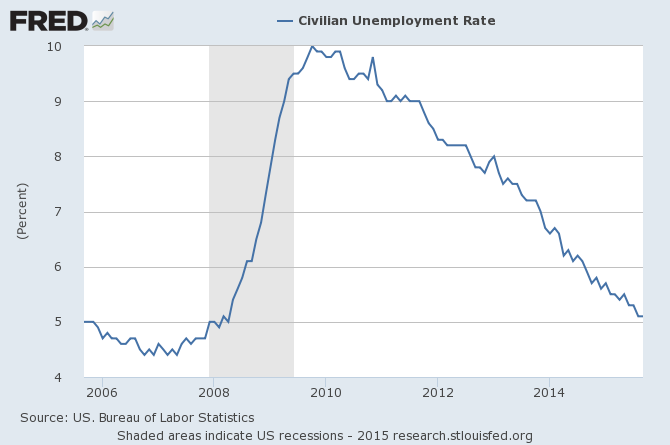

This sets the stage for the Federal Reserve (Fed) to decide on interest rates this week. With last month’s unemployment rate reaching 5.1% (below), the evidence continues to mount that slack in the economy is abating. A 5.1% unemployment rate is at the low end of the Fed’s longer run forecast range of 5.0 – 5.8%. This suggests some tightening is appropriate. The Fed risks falling “behind the curve” if they delay the hike and labor conditions tighten further. As for inflation, the Fed sees the current weakness as largely temporary and tied to weak commodities. If inflation does start to pick up, the Fed could end up having to tighten faster than markets expect. Thus, the Fed should move on rates but look to control expectations for future rate hikes in our view.

Higher rates would come with some benefits too. There has been a dislocation between where rates have been and what is normal given growth potential. For over seven years now, 0% rates have made it hard for pensions and insurance companies to function properly. Savers and those on a fixed income have also had difficulty financing themselves. By denying savers a positive real rate, the purchasing power of savings is lost and incentives to save are undermined. All of this can impose longer-term costs on society and weigh on potential long-term growth. The sooner that artificially low rates become aligned with normal rates, the smaller the negative side effects from misalignment of policy and market rates.

The Good

One important takeaway for us is the fact that the U.S. economy continues to make forward progress. Otherwise, the Fed would not be looking to tighten in the first place. Automobile sales in the U.S. are back above 17 million units per year. Orders for capital goods are near $70 billion per month, suggesting decent corporate investment. Jobless claims sit near multi-decade lows. The ratio of the population working is rising and the unemployment rate is falling. Orders for durable goods are rising faster than inventories. Consumer spending is growing near 3%. These are the positive developments that are guiding our decision to focus portfolios on domestic issues.

The Bad

On the financial market front, a pickup in volatility has introduced some risks that need to be monitored. In recent months we’ve seen the number of stocks declining outpace the number advancing. The yield curve has flattened somewhat, reflecting lower inflation expectations. The spread between corporate bonds and Treasuries is wider now than a year ago (mostly energy related). Inflation expectations have dropped alongside commodity weakness and slowing overseas growth.

The improving economic data, together with mixed financial market conditions, leads us to a balanced posture in portfolios. Portfolios are tactically allocated close to their “neutral” policy weights from a stock / bond perspective. We continue to focus on quality and value in equity selection and expect equity returns to provide positive but smaller long-run returns going forward. Market response to this week Fed’s action (or lack thereof) will be important in determining what comes next for markets and portfolios.

Portfolio Posture

LONG-RUN STRATEGIC POSTURE: Strategic allocations are set to reflect our long-run forecasts for key asset classes. We expect policy rates to remain low as central banks continue to push lower-for-longer rate strategies. Eventually, rates should rise back to more normal levels, but this is expected to happen gradually and unevenly. Fixed income returns are expected to lag current yields as rates rise. Equity returns may track moderate growth in global Gross Domestic Product (GDP) with little to no further lift from margin expansion (margins are already elevated). Equity valuations appear reasonable and in line with historic multiples, so no additional return is being attributed to margin expansion.

Kevin Caron, Portfolio Manager

Chad Morganlander, Portfolio Manager

Matthew Battipaglia, Analyst

Suzanne Ashley, Junior Analyst

The information contained herein has been prepared from sources believed to be reliable but is not guaranteed by us and is not a complete summary or statement of all available data, nor is it considered an offer to buy or sell any securities referred to herein. Opinions expressed are subject to change without notice and do not take into account the particular investment objectives, financial situation, or needs of individual investors. There is no guarantee that the figures or opinions forecasted in this report will be realized or achieved. Employees of Stifel, Nicolaus & Company, Incorporated or its affiliates may, at times, release written or oral commentary, technical analysis, or trading strategies that differ from the opinions expressed within. Past performance is no guarantee of future results. Indices are unmanaged, and you cannot invest directly in an index.

Asset allocation and diversification do not ensure a profit and may not protect against loss. There are special considerations associated with international investing, including the risk of currency fluctuations and political and economic events. Investing in emerging markets may involve greater risk and volatility than investing in more developed countries. Due to their narrow focus, sector-based investments typically exhibit greater volatility. Small company stocks are typically more volatile and carry additional risks, since smaller companies generally are not as well established as larger companies. Property values can fall due to environmental, economic, or other reasons, and changes in interest rates can negatively impact the performance of real estate companies. When investing in bonds, it is important to note that as interest rates rise, bond prices will fall. High-yield bonds have greater credit risk than higher quality bonds. The risk of loss in trading commodities and futures can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. The high degree of leverage that is often obtainable in commodity trading can work against you as well as for you. The use of leverage can lead to large losses as well as gains.