Monday Morning Minute 081318

THE WEEK AHEAD

Against a good global backdrop, Turkey reminds us that risk still exists.

THE CASE OF TURKEY

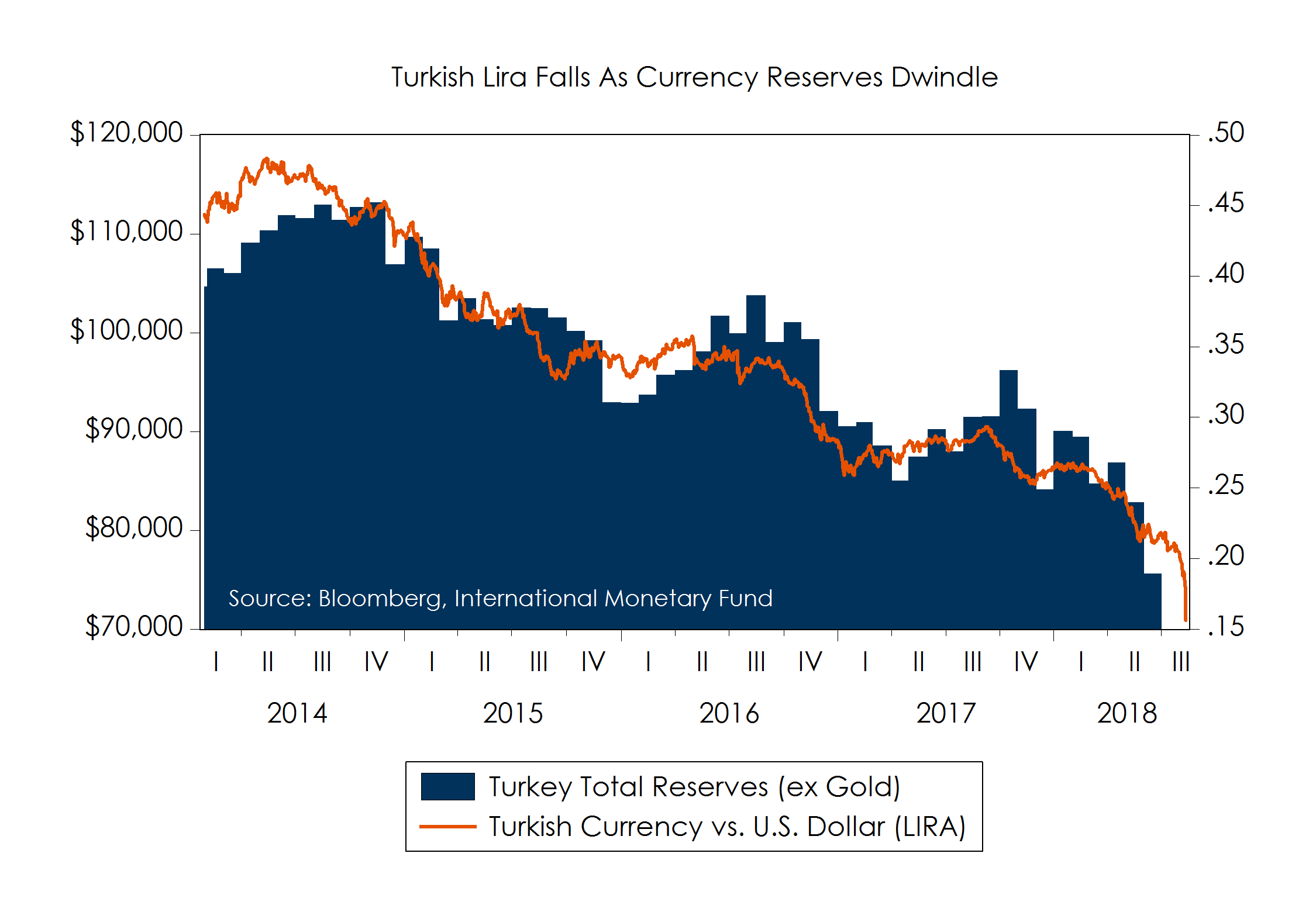

Although the background for growth, particularly in the United States, appears good, we are reminded that the world is not without risk. The latest example of an economy in crisis is Turkey. After a period of heady growth, the country has fallen victim to a sliding currency, skyrocketing inflation and interest rates, and capital flight. The chart below shows the slide in the currency (orange line, right scale) superimposed on top of a declining stock of currency reserves (blue bars, left scale). Those reserves are held by Turkey and used to implement policies designed to protect and effect the currency’s exchange rate. A dwindling supply of reserves leaves the currency, and the Turkish economy, vulnerable. However, Turkey’s troubles aren’t actually rooted in the currency, but other deeply-rooted structural issues in our view.

Turkey – An Emerging Market

Emerging markets like Turkey are different from our own. A desire to play catch-up with the developed world often leads emerging markets to press hard for growth. Turkey, under President Recep Tayyip Erdogan’s leadership, tried to generate this growth by driving up investment. Because Turkey did not have enough of its own savings to pay for such high levels of investment, they turned to foreign borrowing to make up the difference. Over time, this investment-led growth strategy can lead to unsustainable growth in debt, a prelude to today’s crisis.

In Turkey’s case, investment needs exceeded Turkey’s savings by about 5-6%. Looked at another way, Turkey consumed too much and under saved at home, resulting in a 5-6% trade deficit. Either way you look at it, it is easy to see that the main cause of Turkey’s problems isn’t any new development, but the result of years of insufficient domestic savings to pay for such investment. Eventually, either investment rates must come down, or savings rates must go up. There is no other way to bring Turkey’s domestic savings into alignment with domestic investment.

Any excess overhang of debt only makes matters even more complicated. Turkey’s debts to foreigners now exceeds 50% of annual economic output (a level which raises concerns for us), and much of this debt needs to be rolled over in the next year (at a time when interest rates have soared to 17%). As if this wasn’t enough, debt repayment will be made more difficult by the continuing slide in the Lira, which makes foreign debts more costly to repay.

As you can see, emerging markets like Turkey, who borrow heavily in foreign currency to fund growth, have a much different set of risks than developed countries like our own. Emerging market risks are further complicated when debt levels are elevated and the currency is weakening. Such a process is clearly underway in Turkey where a 50% year-over-year slide in the nation’s currency is driving up inflation (now 15%), encouraging capital flight, freezing investor risk appetite (Turkey’s stock market is in a bear market), forcing higher interest rates (now 17%), and threatening a nationwide economic downturn.

Politics are becoming increasingly important for Turkey. The main issue now is whether the Turkish government will implement necessary adjustment measures, or try to forestall needed change. We have seen little that suggests that President Erdogan appears ready to abandon his prior set of economic policies. Instead, he appears intent on doubling-down on a centralized, growth-at-all-costs economic model. We will need to wait and see what happens politically, especially if Turkey’s currency crisis worsens and other nations decide how to respond.

Turkey’s problems are not unique. Emerging market debt-and-currency crises have happened many times before and are almost certain to happen again in the future. These risks create not only the potential for loss but also create the potential for higher returns in the future. We simply must remember that, along with faster growth and return potential, emerging markets have special risks that are different from our own markets. Therefore, we place a greater emphasis on debt, liquidity, politics, and balance of payments in our evaluation process and when assessing the long-run risk and return potential for emerging market investments.

TACTICAL CALLS

Tactical Satellite (Based on 3-6 Month Outlook)

- Overweight Stocks vs. Bonds

Kevin Caron, CFA, Senior Portfolio Manager

Chad Morganlander, Senior Portfolio Manager

Matthew Battipaglia, Portfolio Manager

Suzanne Ashley, Analyst

(973) 549-4168

www.washingtoncrossingadvisors.com

Disclosures

WCA Fundamental Conditions Barometer Description: We regularly assess changes in fundamental conditions to help guide near-term asset allocation decisions. The analysis incorporates approximately 30 forward-looking indicators in categories ranging from Credit and Capital Markets to U.S. Economic Conditions and Foreign Conditions. From each category of data, we create three diffusion-style sub-indices that measure the trends in the underlying data. Sustained improvement that is spread across a wide variety of observations will produce index readings above 50 (potentially favoring stocks), while readings below 50 would indicate potential deterioration (potentially favoring bonds). The WCA Fundamental Conditions Index combines the three underlying categories into a single summary measure. This measure can be thought of as a “barometer” for changes in fundamental conditions.

The information contained herein has been prepared from sources believed to be reliable but is not guaranteed by us and is not a complete summary or statement of all available data, nor is it considered an offer to buy or sell any securities referred to herein. Opinions expressed are subject to change without notice and do not take into account the particular investment objectives, financial situation, or needs of individual investors. There is no guarantee that the figures or opinions forecasted in this report will be realized or achieved. Employees of Stifel, Nicolaus & Company, Incorporated or its affiliates may, at times, release written or oral commentary, technical analysis, or trading strategies that differ from the opinions expressed within. Past performance is no guarantee of future results. Indices are unmanaged, and you cannot invest directly in an index.

Asset allocation and diversification do not ensure a profit and may not protect against loss. There are special considerations associated with international investing, including the risk of currency fluctuations and political and economic events. Investing in emerging markets may involve greater risk and volatility than investing in more developed countries. Due to their narrow focus, sector-based investments typically exhibit greater volatility. Small company stocks are typically more volatile and carry additional risks, since smaller companies generally are not as well established as larger companies. Property values can fall due to environmental, economic, or other reasons, and changes in interest rates can negatively impact the performance of real estate companies. When investing in bonds, it is important to note that as interest rates rise, bond prices will fall. High-yield bonds have greater credit risk than higher-quality bonds. The risk of loss in trading commodities and futures can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. The high degree of leverage that is often obtainable in commodity trading can work against you as well as for you. The use of leverage can lead to large losses as well as gains.

All investments involve risk, including loss of principal, and there is no guarantee that investment objectives will be met. It is important to review your investment objectives, risk tolerance and liquidity needs before choosing an investment style or manager. Equity investments are subject generally to market, market sector, market liquidity, issuer, and investment style risks, among other factors to varying degrees. Fixed Income investments are subject to market, market liquidity, issuer, investment style, interest rate, credit quality, and call risks, among other factors to varying degrees.

This commentary often expresses opinions about the direction of market, investment sector and other trends. The opinions should not be considered predictions of future results. The information contained in this report is based on sources believed to be reliable, but is not guaranteed and not necessarily complete.

The securities discussed in this material were selected due to recent changes in the strategies. This selection criteria is not based on any measurement of performance of the underlying security.

Washington Crossing Advisors LLC is a wholly owned subsidiary and affiliated SEC Registered Investment Adviser of Stifel Financial Corp (NYSE: SF).