Monday Morning Minute 120516

THE WEEK AHEAD

We continue our focus on the potential impact of President-elect Trump’s policy proposals on the economy and our long-run capital market assumptions.

MACRO VIEW

The “Trump” rally signals an expected policy shift based on candidate Trump’s promised economic reforms. His economic plan seeks to achieve faster growth through a combination of proposals designed to lower taxes and regulation. Is this expectation reasonable?

To begin with, the plan, as outlined during the campaign, is large. If implemented as proposed, it would include the largest tax cut since the 1980s. For individuals, the tax plan consolidates seven tax brackets into three, lowers rates at every income level, flattens the tax structure, and introduces other changes. For corporations, income tax rates fall to 15% from 35%, capital investment becomes fully deductible from income, enacts a deemed repatriation of foreign profits at a 10% tax rate, and other changes. We also expect to see proposals on regulation and trade, but specifics on these issues are less clear. This week’s commentary will not seek to address these issues or the macroeconomic effects that financing these expected deficits will likely bring.

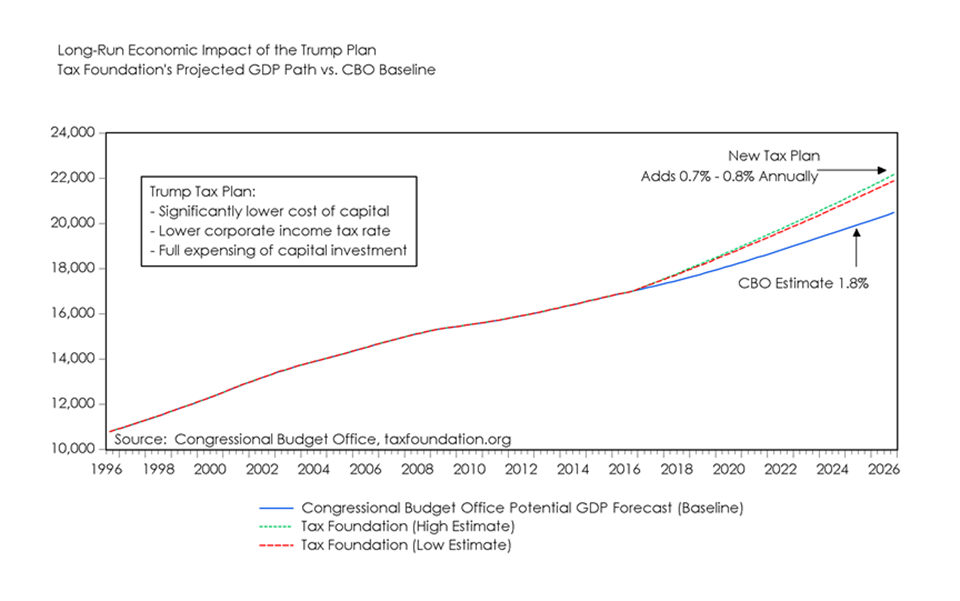

The non-partisan Tax Foundation looked at the president-elect’s plan and estimated its long-run effect on growth (chart, above). They concluded that a significantly lower cost of capital, due to much lower corporate tax rates and expensing of capital expenditures would boost GDP 6.9-8.2% above the Congressional Budget Office’s (CBO’s) forecast level at the end of ten years. The largest impact on the economy comes from changes in expected investment, which are expected to increase by 20.1% to 23.9% above the level currently expected by the CBO. Wages and jobs are also expected to be higher by 5.4-6.3% and 1.8 and 2.2 million, respectively. It is important to note that the study explicitly excluded the effects of any other proposals that were not tax-related. Examples include infrastructure spending, regulatory reform, immigration, and trade. Tariffs, for example, would negatively impact growth while infrastructure investment would further enhance growth.

We continue to believe the president-elect will push first for his domestic policy agenda, led by tax and regulatory reform. A plan to address infrastructure is also likely. The combination of front-loaded tax cuts and spending would pull forward growth as federal deficits initially produce surpluses in the private sector (higher profits and wages). In this scenario, growth could be higher than that modeled out by the tax foundation in the early years, while issues like immigration and trade could weigh on growth in the outer years.

[table id=22 /]

Keep in mind that the Trump plan envisions 4% growth versus a 1.5% – 2.0% CBO expectation under existing assumptions. The difference between the existing CBO baseline and President-elect Trump’s 4% goal is a very large 2-2.5%. We recently increased our 2017-2019 expected growth rate by 1% from 2 – 3% growth to 3 – 4% growth in recognition of a higher probability of increased fiscal stimulus.

The lighter tax on investment, changes to regulation, and fiscal push are the broad outlines of this “pro-growth” plan. The scenarios laid out above are but our initial attempt at reconciling how we might get to President-elect Trump’s 4% growth under an optimistic set of circumstances. Taking into consideration the direct effects on growth from anticipated investment and before factoring in non-tax related policies, we believe such a growth target is reasonable in a good case scenario.

ECONOMIC RELEASES THIS WEEK

| Date | Report | Period | Survey | Prior |

| Monday, December 5: | ISM Non-Mfg Index | November | 55.0 | 54.8 |

| Tuesday, December 6: | International Trade | October | -$41.2 B | -$36.4 B |

| Nonfarm Productivity | 3Q16 | 3.2% | 3.1% | |

| Unit Labor Costs | 3Q16 | 0.3% | 0.3% | |

| Factory Orders | October | 2.6% | 0.3% | |

| Factory Orders Ex Transportation | October | — | 0.6% | |

| Wednesday, December 7: | JOLTS | October | — | 5.486 M |

| Thursday, December 8: | Weekly Jobless Claims | December 3 | — | 268 K |

| Friday, December 9: | Consumer Sentiment | December | 94.1 | 93.8 |

ASSET ALLOCATION PORTFOLIO POSTURE

Based on our long-run capital market expectations, the “core” equity allocation in portfolios are underweight foreign equities / overweight large cap domestic growth, and underweight REITs / overweight Gold. The “core” bond allocation is underweight long-term Treasuries / overweight corporate high-yield bonds.

Based on shorter-term expectations, the “tactical” allocation within portfolios is underweight bonds / overweight stocks.

The information contained herein has been prepared from sources believed to be reliable but is not guaranteed by us and is not a complete summary or statement of all available data, nor is it considered an offer to buy or sell any securities referred to herein. Opinions expressed are subject to change without notice and do not take into account the particular investment objectives, financial situation, or needs of individual investors. There is no guarantee that the figures or opinions forecasted in this report will be realized or achieved. Employees of Stifel, Nicolaus & Company, Incorporated or its affiliates may, at times, release written or oral commentary, technical analysis, or trading strategies that differ from the opinions expressed within. Past performance is no guarantee of future results. Indices are unmanaged, and you cannot invest directly in an index.

Asset allocation and diversification do not ensure a profit and may not protect against loss. There are special considerations associated with international investing, including the risk of currency fluctuations and political and economic events. Investing in emerging markets may involve greater risk and volatility than investing in more developed countries. Due to their narrow focus, sector-based investments typically exhibit greater volatility. Small company stocks are typically more volatile and carry additional risks, since smaller companies generally are not as well established as larger companies. Property values can fall due to environmental, economic, or other reasons, and changes in interest rates can negatively impact the performance of real estate companies. When investing in bonds, it is important to note that as interest rates rise, bond prices will fall. High-yield bonds have greater credit risk than higher quality bonds. The risk of loss in trading commodities and futures can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. The high degree of leverage that is often obtainable in commodity trading can work against you as well as for you. The use of leverage can lead to large losses as well as gains.

The WCA Fundamental Conditions Barometer measures the breadth of changes to a wide variety of fundamental data. The barometer measures the proportion of indicators under review that are moving up or down together. A barometer reading above 50 generally indicates a more bullish environment for the economy and equities, and a lower reading implies the opposite. Quantifying changes this way helps us incorporate new facts into our near-term outlook in an objective and unbiased way. More information on the barometer is found in our latest quarterly report, available at www.washingtoncrossingadvisors.com/insights.html.