Monday Morning Minute 101016

THE WEEK AHEAD

The Federal Reserve releases minutes from their latest Federal Open Market Committee (FOMC) meeting Wednesday, and retail sales figures are due Friday.

MACRO VIEW

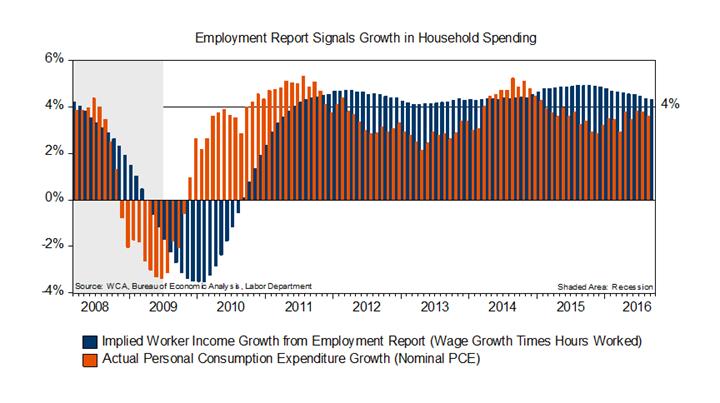

Friday’s employment report suggests that income and spending are still growing. Six and one quarter years from the recession’s end, we see that the average wages and total numbers of hours worked are expanding. We estimate that hours will be expanding at a 1.5% yearly rate and wages will be growing at 2.5%. Combining these figures, total income should be expanding near 4%, and this pace is consistent with an expansion in consumer spending also in the ballpark of 4% (chart below). And since there is a close correlation between consumer spending and GDP growth, we may also intuit that the economy is still on a growth path.

While growth in hours worked is slowing toward 1.5% versus 2.5% last year, wage growth is picking up. By our estimate, hourly earnings are growing near 2.5% versus 2% a year ago. This raises the question whether the uptick in wage pressure signals the start of aggressive rate hikes by the Federal Reserve (Fed).

We don’t think so. Here’s why.

Core inflation remains below the Fed’s 2% target, and the connection between wages and inflation is a dubious one. Fed Chair Janet Yellen has expressed her own doubts that an initial wage increase must necessarily lead to inflation. She argued that after an initial pickup in wage growth, higher real wages should attract more workers back into the labor force, should put a lid on wage growth, and stabilize the falling unemployment rate.

Friday’s employment report supports her basic argument. The labor force participation rate, the percentage of working age people either having or looking for jobs, is up 0.5% from a year ago. This is the strongest annual advance in the labor force participation rate since 1996.

If Chair Yellen is right, unemployment should stay near 5%, wage acceleration should stall, inflation should remain low, and policy rates can continue to rise gradually.

ECONOMIC RELEASES THIS WEEK

| Date | Report | Period | Survey | Prior |

| Monday, October 10: | Columbus Day: Banks Closed, Markets Open | |||

| Tuesday, October 11: | NFIB Small Business Optimism | September | 95.1 | 94.4 |

| Wednesday, October 12: | FOMC Minutes from September Meeting | |||

| JOLTS Job Openings | August | 5.825 M | 5.871 M | |

| Thursday, October 13: | Weekly Jobless Claims | October 8 | — | 249 K |

| Import Price Index M/M | September | 0.1% | -0.2% | |

| Import Price Index Y/Y | September | — | -2.2% | |

| Friday, October 14: | PPI Final Demand M/M | September | 0.2% | 0.0% |

| PPI Ex Food & Energy M/M | September | 0.1% | 0.1% | |

| PPI Ex Food, Energy & Trade M/M | September | — | 0.3% | |

| PPI Final Demand Y/Y | September | 0.6% | 0.0% | |

| PPI Ex Food & Energy Y/Y | September | 1.2% | 1.0% | |

| PPI Ex Food, Energy & Trade Y/Y | September | — | 1.2% | |

| Retail Sales M/M | September | 0.5% | -0.3% | |

| Retail Sales Ex Auto M/M | September | 0.4% | -0.1% | |

| Retail Sales Ex Auto & Gas M/M | September | — | -0.1% | |

| Business Inventories | August | 0.1% | 0.0% | |

| Consumer Sentiment | October | 91.9 | 91.2 |

ASSET ALLOCATION PORTFOLIO POSTURE

LONG-RUN STRATEGIC POSTURE: Our long-run forecasts lead us to overweight large cap domestic growth stocks, high-yield corporate bonds, and gold in the diversified “core” of portfolios. Underweight positions in “core” are long-term U.S. Treasuries, foreign developed equities, and REITs. The equity allocation in the short-term tactical”satellite” portion of portfolios currently stands at 60% equity/40% fixed income.

The information contained herein has been prepared from sources believed to be reliable but is not guaranteed by us and is not a complete summary or statement of all available data, nor is it considered an offer to buy or sell any securities referred to herein. Opinions expressed are subject to change without notice and do not take into account the particular investment objectives, financial situation, or needs of individual investors. There is no guarantee that the figures or opinions forecasted in this report will be realized or achieved. Employees of Stifel, Nicolaus & Company, Incorporated or its affiliates may, at times, release written or oral commentary, technical analysis, or trading strategies that differ from the opinions expressed within. Past performance is no guarantee of future results. Indices are unmanaged, and you cannot invest directly in an index.

Asset allocation and diversification do not ensure a profit and may not protect against loss. There are special considerations associated with international investing, including the risk of currency fluctuations and political and economic events. Investing in emerging markets may involve greater risk and volatility than investing in more developed countries. Due to their narrow focus, sector-based investments typically exhibit greater volatility. Small company stocks are typically more volatile and carry additional risks, since smaller companies generally are not as well established as larger companies. Property values can fall due to environmental, economic, or other reasons, and changes in interest rates can negatively impact the performance of real estate companies. When investing in bonds, it is important to note that as interest rates rise, bond prices will fall. High-yield bonds have greater credit risk than higher quality bonds. The risk of loss in trading commodities and futures can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. The high degree of leverage that is often obtainable in commodity trading can work against you as well as for you. The use of leverage can lead to large losses as well as gains.

The WCA Fundamental Conditions Barometer measures the breadth of changes to a wide variety of fundamental data. The barometer measures the proportion of indicators under review that are moving up or down together. A barometer reading above 50 generally indicates a more bullish environment for the economy and equities, and a lower reading implies the opposite. Quantifying changes this way helps us incorporate new facts into our near-term outlook in an objective and unbiased way. More information on the barometer is found in our latest quarterly report, available at www.washingtoncrossingadvisors.com/insights.html.