Monday Morning Minute 082718

THE WEEK AHEAD

The economy continues to power along, led by strengthening investment.

Investment

The economy is doing far better than we had expected a few years ago. Mired in sub-par growth for years, the U.S. economy is accelerating by most measures we follow. Jobs are plentiful, corporate profits are up, and wealth measures are full. The economy grew by 4.1% in the second quarter, the best pace since 2014.

Business investment is also turning up after a two year lull in 2014-2015. Through July, core capital goods orders surged to nearly the highest levels on record. 8.5% year-over-year to $69.6 billion. Annualized, this pace amounts to roughly $800 billion, or 4% of gross domestic product. Four percent is at the low end of the historic range, however.

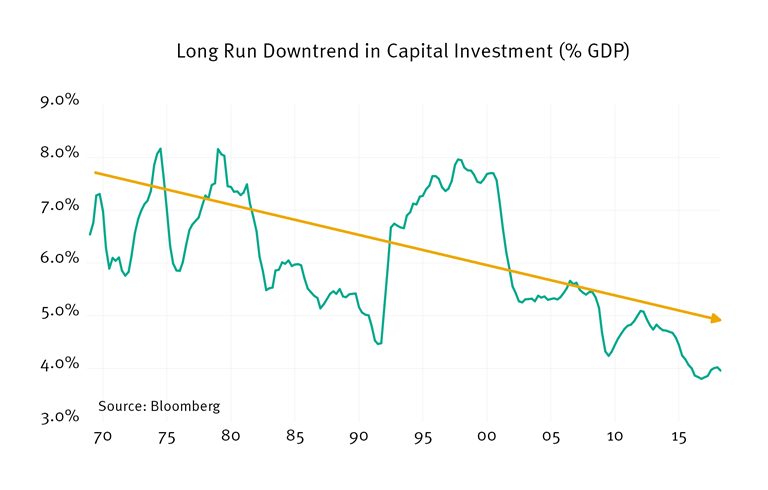

One of the primary drivers of long-run returns is the sustained growth of the underlying economy. Our economy has endured nearly 20 years of declining capital investment (chart A, below). In some ways, this is the mirror image of the go-go 1990’s capital spending cycle. The pendulum swings both ways, and it would be good indeed to see a reversal in this long-running downtrend.

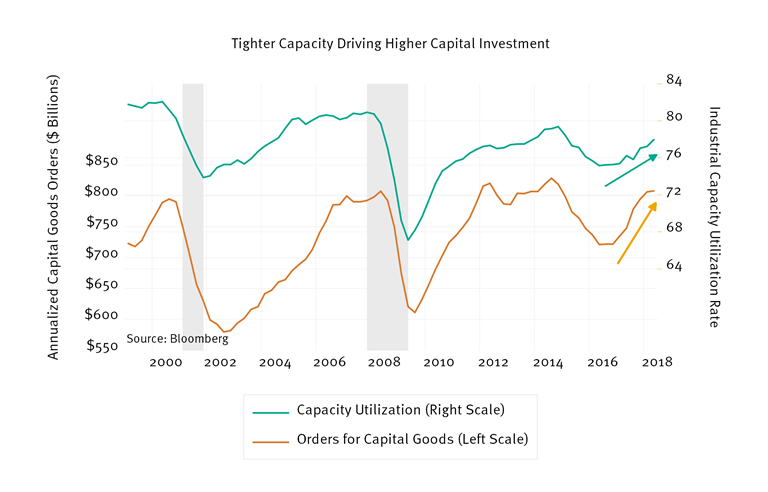

Now, we see that underinvestment is leading to tight industrial production capacity. Strong final demand by for product is pushing the physical limits of our domestic production (Chart B, below). Similar “tightness” can be seen in labor markets, where the unemployment rate is set to hit 3.8%. Only for a brief time in the late 1960s and early 2000s has there been so few job seekers available to fill openings.

Investment spending may also be seeing a lift because of recent tax reforms. Lower corporate tax rates, and accelerated depreciation, can add incentives for businesses to push ahead with capital commitments. We saw similar upswings in capital spending following past tax changes which featured bonus depreciation. The 2002-2003 tax reforms under President Bush and the 2008-2009 stimulus act under President Obama both included accelerated depreciation, which gave a near-term boost to investment and growth.

On the horizon, we still need to see business navigate the trade issue. Negotiations between American and Chinese officials broke down last week. This increases the likelihood that the U.S. will move ahead with planned tariffs on 25% of $200 billion of Chinese goods. Mounting trade uncertainty could cause companies to slow investment, but we don’t see actual signs of this yet.

TACTICAL CALLS

Tactical Satellite (Based on 3-6 Month Outlook)

- Overweight Stocks vs. Bonds

Kevin Caron, CFA, Senior Portfolio Manager

Chad Morganlander, Senior Portfolio Manager

Matthew Battipaglia, Portfolio Manager

Suzanne Ashley, Analyst

(973) 549-4168

www.washingtoncrossingadvisors.com

_______________________________________________________________________________________________________________________________________

Disclosures

WCA Fundamental Conditions Barometer Description: We regularly assess changes in fundamental conditions to help guide near-term asset allocation decisions. The analysis incorporates approximately 30 forward-looking indicators in categories ranging from Credit and Capital Markets to U.S. Economic Conditions and Foreign Conditions. From each category of data, we create three diffusion-style sub-indices that measure the trends in the underlying data. Sustained improvement that is spread across a wide variety of observations will produce index readings above 50 (potentially favoring stocks), while readings below 50 would indicate potential deterioration (potentially favoring bonds). The WCA Fundamental Conditions Index combines the three underlying categories into a single summary measure. This measure can be thought of as a “barometer” for changes in fundamental conditions.

The information contained herein has been prepared from sources believed to be reliable but is not guaranteed by us and is not a complete summary or statement of all available data, nor is it considered an offer to buy or sell any securities referred to herein. Opinions expressed are subject to change without notice and do not take into account the particular investment objectives, financial situation, or needs of individual investors. There is no guarantee that the figures or opinions forecasted in this report will be realized or achieved. Employees of Stifel, Nicolaus & Company, Incorporated or its affiliates may, at times, release written or oral commentary, technical analysis, or trading strategies that differ from the opinions expressed within. Past performance is no guarantee of future results. Indices are unmanaged, and you cannot invest directly in an index.

Asset allocation and diversification do not ensure a profit and may not protect against loss. There are special considerations associated with international investing, including the risk of currency fluctuations and political and economic events. Investing in emerging markets may involve greater risk and volatility than investing in more developed countries. Due to their narrow focus, sector-based investments typically exhibit greater volatility. Small company stocks are typically more volatile and carry additional risks, since smaller companies generally are not as well established as larger companies. Property values can fall due to environmental, economic, or other reasons, and changes in interest rates can negatively impact the performance of real estate companies. When investing in bonds, it is important to note that as interest rates rise, bond prices will fall. High-yield bonds have greater credit risk than higher-quality bonds. The risk of loss in trading commodities and futures can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. The high degree of leverage that is often obtainable in commodity trading can work against you as well as for you. The use of leverage can lead to large losses as well as gains.

All investments involve risk, including loss of principal, and there is no guarantee that investment objectives will be met. It is important to review your investment objectives, risk tolerance and liquidity needs before choosing an investment style or manager. Equity investments are subject generally to market, market sector, market liquidity, issuer, and investment style risks, among other factors to varying degrees. Fixed Income investments are subject to market, market liquidity, issuer, investment style, interest rate, credit quality, and call risks, among other factors to varying degrees.

This commentary often expresses opinions about the direction of market, investment sector and other trends. The opinions should not be considered predictions of future results. The information contained in this report is based on sources believed to be reliable, but is not guaranteed and not necessarily complete.

The securities discussed in this material were selected due to recent changes in the strategies. This selection criteria is not based on any measurement of performance of the underlying security.

Washington Crossing Advisors LLC is a wholly owned subsidiary and affiliated SEC Registered Investment Adviser of Stifel Financial Corp (NYSE: SF).