Monday Morning Minute 012218

THE WEEK AHEAD

Growth story continues to lift equities, but faster growth is beginning to stir concerns over rates and inflation.

MACROECONOMIC INSIGHT

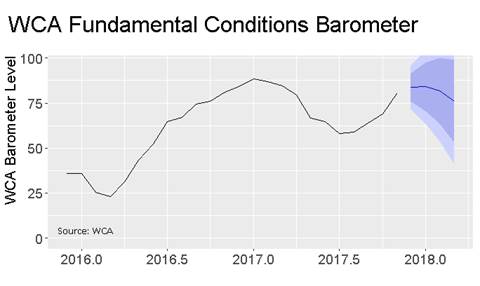

We have seen constant upward revisions to earnings and growth estimates for the last year, creating the backdrop for good equity market performance. A combination of easy monetary policy, improving growth, and strong sentiment are driving continued upside surprises for growth. Leading economic indicators remain strong, employment trends are solid, business investment is picking up, and order rates for durable goods are surging. Our own WCA Fundamental Conditions Barometer (below) surged through the later part of 2017 as tax cuts became factored into the outlook for growth. In short, there continues to be good momentum behind a long-running string of upgrades to the global economic outlook.

But Markets Begin to Discount Faster Rate Hikes Ahead

While all of this good news has added to the case for stocks, it also carries with it reasons for some to worry about higher short-term rates. A recent rise in both the two-year Treasury rate and consumer price inflation to above 2% has increased the potential for more aggressive rate hikes by the Fed, something not currently anticipated by markets. The chart below shows a measure of the expected policy rate changes based on the forward market for the Treasury rate. In this analysis, we subtract from the current 1-year Treasury the same rate an investor could “lock in” one year from now in the forwards market. The main point is that when this spread rises, as has happened recently, it reflects a rising expectation for faster rate hikes ahead.

The Inflation Worry

A bearish argument contemplates excessively strong global growth leading to capacity constraints, higher inflation, and a rapid series of rate increases leading eventually to a recession. Those in this camp will tend to look at capacity constraints in the real economy and the long duration of the business cycle as reason to fear a pickup in inflation ahead, along with aggressive rate hikes. With 80% of countries now generating output higher than what many economists consider to be “potential” output, and with the unemployment rate in the United States and Europe at very low levels, the return of so-called “wage-push” inflation seems like a plausible potential outcome.

We are less convinced that “tight capacity” in labor markets will automatically lead to a rapid increase in the price level for a simple reason. There is a very weak historical relationship between the unemployment rate and inflation, and there is little evidence that shows any convincing connection between wage growth and inflation. The “clear” logic of labor tightness leading to inflation is far from clear when we actually look at the historic evidence. The evidence simply does not support the theory — a regression of inflation on the unemployment rate from 1997-2017 reveals a very low “goodness of fit”, or R-squared, statistic of 0.08.

If we saw a large amount of new money chasing fewer goods, then inflation fears might be better justified. However, with total outstanding credit growing near the same pace as the real output of goods and services, and with few signs of bottlenecks in the global supply chain, we do not see an imminent surge in inflation ahead. Of course, we will continue to monitor the situation and will modify our return expectations if the facts change. For now, however, we are making no change to our outlook for slow increases in rates.

Lower Returns Ahead

As we said in our Viewpoint 2018, we expect to see good growth this year and momentum could carry the bull a while longer. Our long-run return expectations are, however, lower than they have been in recent years due to high starting stock market valuations and compressed risk premiums throughout many areas of the bond market. Allocating capital between stocks and bonds would be further complicated by a regime shift to rapidly rising short-term rates (our risk case). Even without this risk factor, expected long-run risk-adjusted returns are likely, in our view, to be lower than in the past because above-average valuations and below-average volatility measures are expected to gravitate back toward longer-run averages. This process will create a headwind against which improving growth forecasts must push.

If the nascent uptrend in rate expectations continues, this could evolve into a challenge the market will need to overcome in the months ahead. For now, the improving fundamental growth outlook still best explains market behavior. These new trends in inflation and forward rate expectations take on even greater importance as leadership at the Fed transitions from Janet Yellen’s leadership to Mr. Powell’s on February 3.

ECONOMIC DATA THIS WEEK

| Date | Report | Period | Prior |

| Monday, Jan 15: | Martin Luther King Jr. Day | ||

| Tuesday, Jan 16: | Empire State Manufacturing Survey | Jan | 18.0 |

| Wednesday, Jan 17: | Industrial Production M/M | Dec | 0.2% |

| Manufacturing M/M | Dec | 0.2% | |

| Capacity Utilization Rate | Dec | 77.1% | |

| NAHB Housing Market Index | Jan | 74 | |

| Fed Beige Book | |||

| Foreign Demand for LT U.S. Securities | Nov | $23.2B | |

| Thursday, Jan 18: | Weekly Jobless Claims | 1/13 | 261K |

| Housing Starts | Dec | 1.297M | |

| Philadelphia Fed Business Outlook Survey | Jan | 26.2 | |

| Friday, Jan 19: | Consumer Sentiment | Jan | 95.9 |

| Source: Bloomberg |

ASSET ALLOCATION PORTFOLIO POSTURE

Based on shorter-term expectations, the “tactical satellite” allocation within portfolios is:

Overweight Stocks vs. Bonds

Kevin Caron, CFA, Senior Portfolio Manager

Chad Morganlander, Senior Portfolio Manager

Matthew Battipaglia, Portfolio Manager

Suzanne Ashley, Analyst

(973) 549-4052

______________________________________________________________________________________________________________________________________

Disclosures

WCA Fundamental Conditions Barometer Description: We regularly assess changes in fundamental conditions to help guide near-term asset allocation decisions. The analysis incorporates approximately 30 forward-looking indicators in categories ranging from Credit and Capital Markets to U.S. Economic Conditions and Foreign Conditions. From each category of data, we create three diffusion-style sub-indices that measure the trends in the underlying data. Sustained improvement that is spread across a wide variety of observations will produce index readings above 50 (potentially favoring stocks), while readings below 50 would indicate potential deterioration (potentially favoring bonds). The WCA Fundamental Conditions Index combines the three underlying categories into a single summary measure. This measure can be thought of as a “barometer” for changes in fundamental conditions.

The information contained herein has been prepared from sources believed to be reliable but is not guaranteed by us and is not a complete summary or statement of all available data, nor is it considered an offer to buy or sell any securities referred to herein. Opinions expressed are subject to change without notice and do not take into account the particular investment objectives, financial situation, or needs of individual investors. There is no guarantee that the figures or opinions forecasted in this report will be realized or achieved. Employees of Stifel, Nicolaus & Company, Incorporated or its affiliates may, at times, release written or oral commentary, technical analysis, or trading strategies that differ from the opinions expressed within. Past performance is no guarantee of future results. Indices are unmanaged, and you cannot invest directly in an index.

Asset allocation and diversification do not ensure a profit and may not protect against loss. There are special considerations associated with international investing, including the risk of currency fluctuations and political and economic events. Investing in emerging markets may involve greater risk and volatility than investing in more developed countries. Due to their narrow focus, sector-based investments typically exhibit greater volatility. Small company stocks are typically more volatile and carry additional risks, since smaller companies generally are not as well established as larger companies. Property values can fall due to environmental, economic, or other reasons, and changes in interest rates can negatively impact the performance of real estate companies. When investing in bonds, it is important to note that as interest rates rise, bond prices will fall. High-yield bonds have greater credit risk than higher-quality bonds. The risk of loss in trading commodities and futures can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. The high degree of leverage that is often obtainable in commodity trading can work against you as well as for you. The use of leverage can lead to large losses as well as gains.

All investments involve risk, including loss of principal, and there is no guarantee that investment objectives will be met. It is important to review your investment objectives, risk tolerance and liquidity needs before choosing an investment style or manager. Equity investments are subject generally to market, market sector, market liquidity, issuer, and investment style risks, among other factors to varying degrees. Fixed Income investments are subject to market, market liquidity, issuer, investment style, interest rate, credit quality, and call risks, among other factors to varying degrees.

This commentary often expresses opinions about the direction of market, investment sector and other trends. The opinions should not be considered predictions of future results. The information contained in this report is based on sources believed to be reliable, but is not guaranteed and not necessarily complete.

The securities discussed in this material were selected due to recent changes in the strategies. This selection criteria is not based on any measurement of performance of the underlying security.

Washington Crossing Advisors LLC is a wholly owned subsidiary and affiliated SEC Registered Investment Adviser of Stifel Financial Corp (NYSE: SF).