Markets Digest Brexit

Britain’s decision to leave the European Union (EU) reflects widespread dissatisfaction with EU governance. The rejection of EU governance highlights the inherently unstable nature of the organization. If individual members experienced long-run benefits, defections would not occur. Instead, the people of Europe would press for a formal merger. If individual members become dissatisfied, these countries are likely to break away. Why would a dissatisfied and democratic country like the United Kingdom look to remain? Most, including us, believed the vote would lean toward maintaining the status-quo. This exit vote marks the first tangible step backward from the decades old vision of a united Europe.

A Specter of Dis-Union Haunts Europe

Europe’s financial and political leaders will redouble efforts to shore up the remaining union. Britain and the EU will negotiate the terms of separation against the backdrop of next year’s French and German elections. The British referendum may feed existing anti-EU sentiment, raising the specter of further defections. For this reason, we see the Brexit vote as a significant political event in the evolution of the Eurozone project. We expect the uncertainty that will come with Britain’s exit to be rancorous and lengthy.

We do not expect Britain’s exit from the EU to significantly harm growth in the near-term. The UK accounts for roughly 4% of global GDP, and a localized recession in the UK would have little impact on global output. For the United States, the total value of imports and exports to the U.K. is roughly $100 billion, or 0.5% of GDP. This $100 billion is also small relative to the $4.9 trillion value of total U.S. trade (imports plus exports). As you can see, the direct impact on the U.S. economy from a localized U.K. recession should be modest.

What about confidence? Could an extended bout of market unrest undo the small amount of forward momentum we are seeing in the data? This is a risk scenario that needs to be monitored. For now, however, we see markets adjusting rationally to unexpected news. The Dow Jones Industrial Average fell over 600 points Friday. This 3% drop erased significant gains just prior to the vote, leaving the total equity decline for the week was just over 1%. The cost to insure against European sovereign defaults rose, but is far below levels seen during prior episodes of stress. In short, it is far too early to conclude that the Brexit will have a lasting negative impact on confidence or investment.

Meanwhile, Back at Home

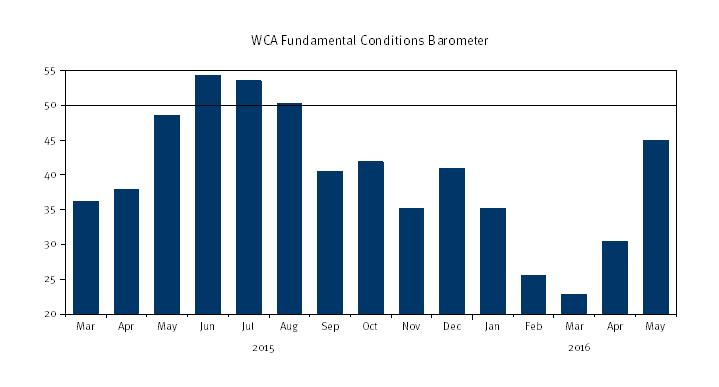

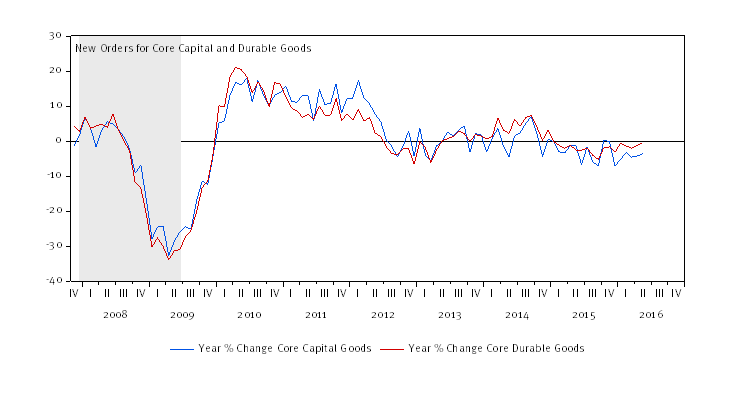

As the Brexit drama grew to a crescendo, we continue to see some improvement in the data. The WCA Fundamental Conditions Barometer rose in May to 45. Through May, we saw some improvement in financial conditions and global manufacturing. Recent volatility and weak reports on June business investment suggest growth will remain slow. The first chart below shows the recent improvement in our WCA Fundamental Conditions Barometer. The second chart below shows the still negative performance for core durable and capital goods orders. In short, there seems to be mixed-but-improving fundamental economic data, but investment and earnings trends are likely to remain a drag.

In our view, the Brexit-related spike in volatility will likely remain contained. If we are right, the passage of time will clear away some of the immediate uncertainty and eventually lead to a better outlook for equities.

ECONOMIC RELEASES THIS WEEK

| Date | Report | Period | Survey | Prior |

| Monday, June 27: | Advance Goods Trade Balance | May | -$59.2B | -$57.5B |

| Dallas Fed Manf. Activity | June | -15.0 | -20.8 | |

| Tuesday, June 28: | GDP Annualized Q/Q | 1Q2016 | 1.0% | 0.8% |

| S&P Case-Shiller HPI 20-city, SA – M/M | April | — | 0.9% | |

| S&P Case-Shiller HPI 20-city, NSA – M/M | April | 0.7% | 0.9% | |

| S&P Case-Shiller HPI 20-city, NSA – Y/Y | April | 5.5% | 5.4% | |

| Consumer Confidence | June | 93.1 | 92.6 | |

| Wednesday, June 29: | Personal Income | May | 0.3% | 0.4% |

| Personal Spending | May | 0.3% | 1.0% | |

| Pending Home Sales Index – M/M | May | -1.0% | 5.1% | |

| Thursday, June 30: | Weekly Jobless Claims | June 25 | — | 259K |

| Chicago PMI | June | 50.4 | 49.3 | |

| Friday, July 1: | ISM Manufacturing Index | June | 51.4 | 51.3 |

| PMI Manufacturing Index | June | — | 50.7 | |

| Construction Spending M/M | May | 0.6% | -1.8% | |

| Domestic Vehicle Sales | June | — | 13.33M | |

| Total Vehicle Sales | June | 17.35M | 17.37M |

ASSET ALLOCATION PORTFOLIO POSTURE

LONG-RUN STRATEGIC POSTURE: Our macro outlook is for slow growth and stubbornly low inflation. The start of policy normalization following years of zero interest rate policy in the United States comes at a time of weakening global growth and mixed signals from the domestic economy. We continue to view the United States economy as best positioned to weather the overall weak global environment that resurfaced in 2015.

The information contained herein has been prepared from sources believed to be reliable but is not guaranteed by us and is not a complete summary or statement of all available data, nor is it considered an offer to buy or sell any securities referred to herein. Opinions expressed are subject to change without notice and do not take into account the particular investment objectives, financial situation, or needs of individual investors. There is no guarantee that the figures or opinions forecasted in this report will be realized or achieved. Employees of Stifel, Nicolaus & Company, Incorporated or its affiliates may, at times, release written or oral commentary, technical analysis, or trading strategies that differ from the opinions expressed within. Past performance is no guarantee of future results. Indices are unmanaged, and you cannot invest directly in an index.

Asset allocation and diversification do not ensure a profit and may not protect against loss. There are special considerations associated with international investing, including the risk of currency fluctuations and political and economic events. Investing in emerging markets may involve greater risk and volatility than investing in more developed countries. Due to their narrow focus, sector-based investments typically exhibit greater volatility. Small company stocks are typically more volatile and carry additional risks, since smaller companies generally are not as well established as larger companies. Property values can fall due to environmental, economic, or other reasons, and changes in interest rates can negatively impact the performance of real estate companies. When investing in bonds, it is important to note that as interest rates rise, bond prices will fall. High-yield bonds have greater credit risk than higher quality bonds. The risk of loss in trading commodities and futures can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. The high degree of leverage that is often obtainable in commodity trading can work against you as well as for you. The use of leverage can lead to large losses as well as gains.

The WCA Fundamental Conditions Barometer measures the breadth of changes to a wide variety of fundamental data. The barometer measures the proportion of indicators under review that are moving up or down together. A barometer reading above 50 generally indicates a more bullish environment for the economy and equities, and a lower reading implies the opposite. Quantifying changes this way helps us incorporate new facts into our near-term outlook in an objective and unbiased way. More information on the barometer is found in our latest quarterly report, available at www.washingtoncrossingadvisors.com/insights.html.

The Dow Jones Industrial Average is an index that shows how 30 large, publicly owned companies based in the United States have traded during a standard trading session in the stock market.

Kevin Caron, Portfolio Manager

Chad Morganlander, Portfolio Manager

Matthew Battipaglia, Analyst

Suzanne Ashley, Junior Analyst