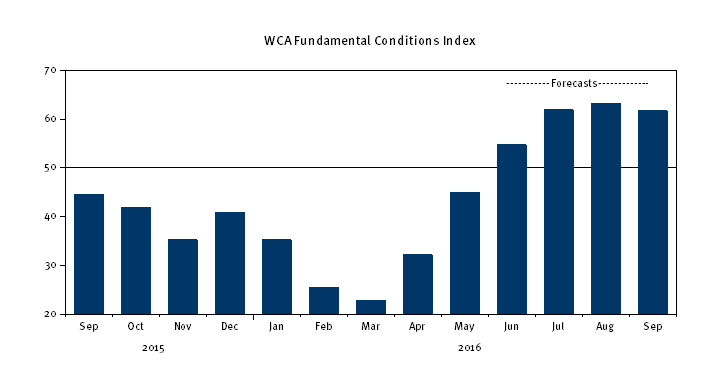

Barometer Improves

The Republican National Convention kicks off in Cleveland this week. Expect politics to dominate headlines. Meanwhile, the basic pattern in the data still suggests an improving economy as we head toward the fall.

MACRO VIEW

The market’s rally of late is accompanied by improvement in the WCA Fundamental Conditions Index*. Through May, the index rose to 45 and is likely to break above 50 by the time all of the data becomes available. Earnings forecasts for the S&P 500 are up four straight months, along with some surveys of business expectations. Oil prices are no longer at lows. Expectation of rate hikes have given way to little, if any, change. Real interest rates are pulling back. Credit spreads are down, market breadth is up, and latest readings on industrial production and retail sales are good. Much of this is feeding into our measurement of changing macro fundamentals. Our forecast is shown below.

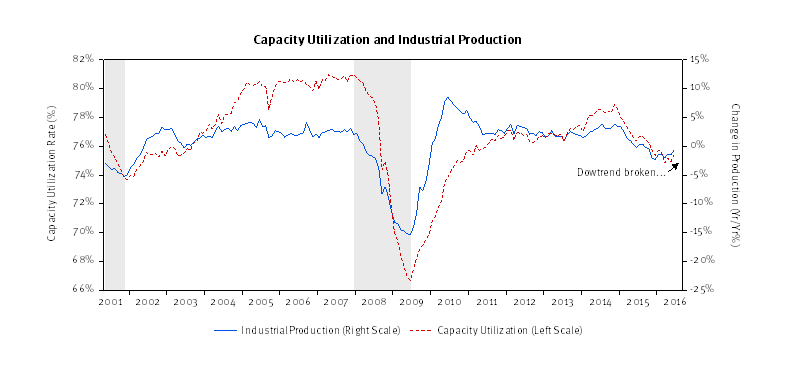

Last week, we saw industrial production rise by a greater-than-expected 0.6%, and capacity utilization tightened by the largest amount since 2014 (below). These are important improvements because industrial production is a fairly reliable signal about the business cycle. Given this level of output, we are growing more comfortable that economic growth is accelerating out of the doldrums seen throughout the fall and early spring. While still early in the bounce back, gathering momentum could lead growth back toward the 2.25% growth rate we forecast at the start of the year.

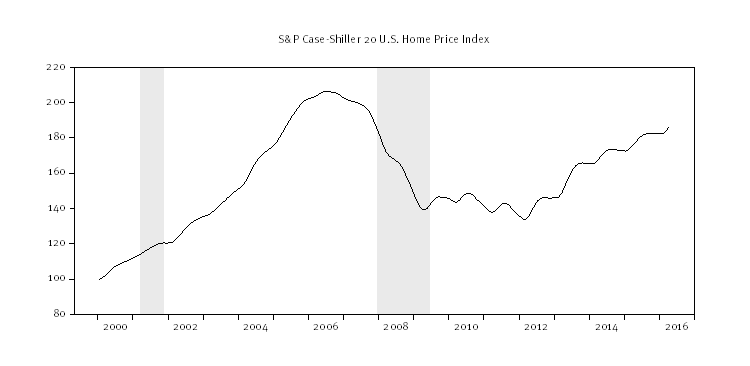

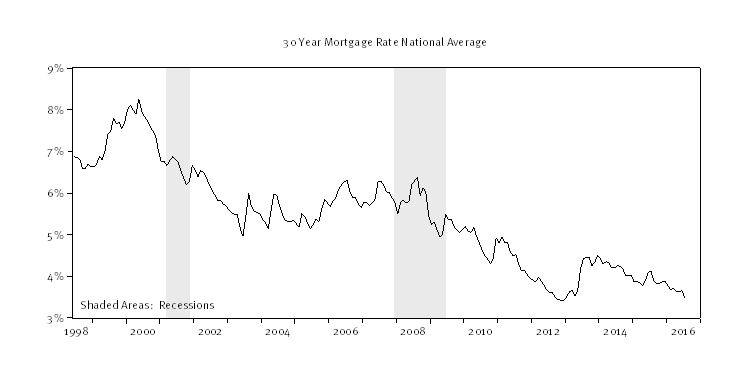

This week will include a host of data about housing. A survey of home builders, monthly building permits and housing starts, mortgage applications, and an independent housing price index. We’ve seen steady improvement in most of these measures and expect more of the same this week. We also note that the 30-year mortgage is back near record lows. The average national 30-year mortgage rate has fallen to 3.5% from the 6-9% level common pre-financial crisis.

So far so good. With a whiff of growth, the Federal Reserve (Fed) seen as “on hold,” and nowhere else to go for yield, equities are getting a bid. At some point, we must address the broader issues of weak profits and investment, low productivity growth, and ultimately when the Fed decides to resume tightening.

ECONOMIC RELEASES THIS WEEK

| Date | Report | Period | Survey | Prior |

| Monday, July 18: | NAHB Housing Market Index | July | 60 | 60 |

| Tuesday, July 19: | Housing Starts M/M | June | 0.5% | -0.3% |

| Building Permits M/M | June | 1.2% | 0.7% | |

| Wednesday, July 20: | No Economic Releases | |||

| Thursday, July 21: | Weekly Jobless Claims | July 16 | — | 254 K |

| Philadelphia Fed Business Outlook | July | 5.0 | 4.7 | |

| Existing Home Sales M/M | June | -1.1% | 1.8% | |

| Friday, July 22: | PMI Manufacturing Index Flash | July | 51.5 | 51.3 |

ASSET ALLOCATION PORTFOLIO POSTURE

LONG-RUN STRATEGIC POSTURE: Our long-run forecasts lead us to overweight large cap domestic growth stocks, high-yield corporate bonds, and gold in the diversified “core” of portfolios. Underweight positions in “core” are long-term U.S. Treasuries, foreign developed equities, and REITs. Meanwhile the equity allocation in the short-term tactical “satellite” portion of portfolios was increased to 40% equity / 60% fixed income from 33% equity / 66% fixed income. Mid-year rebalancing took place at the end of June to reflect updated long-run forecasts.

Kevin Caron, Portfolio Manager

Chad Morganlander, Portfolio Manager

Matthew Battipaglia, Analyst

Suzanne Ashley, Junior Analyst

(973) 549-4052

The information contained herein has been prepared from sources believed to be reliable but is not guaranteed by us and is not a complete summary or statement of all available data, nor is it considered an offer to buy or sell any securities referred to herein. Opinions expressed are subject to change without notice and do not take into account the particular investment objectives, financial situation, or needs of individual investors. There is no guarantee that the figures or opinions forecasted in this report will be realized or achieved. Employees of Stifel, Nicolaus & Company, Incorporated or its affiliates may, at times, release written or oral commentary, technical analysis, or trading strategies that differ from the opinions expressed within. Past performance is no guarantee of future results. Indices are unmanaged, and you cannot invest directly in an index.

Asset allocation and diversification do not ensure a profit and may not protect against loss. There are special considerations associated with international investing, including the risk of currency fluctuations and political and economic events. Investing in emerging markets may involve greater risk and volatility than investing in more developed countries. Due to their narrow focus, sector-based investments typically exhibit greater volatility. Small company stocks are typically more volatile and carry additional risks, since smaller companies generally are not as well established as larger companies. Property values can fall due to environmental, economic, or other reasons, and changes in interest rates can negatively impact the performance of real estate companies. When investing in bonds, it is important to note that as interest rates rise, bond prices will fall. High-yield bonds have greater credit risk than higher quality bonds. The risk of loss in trading commodities and futures can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. The high degree of leverage that is often obtainable in commodity trading can work against you as well as for you. The use of leverage can lead to large losses as well as gains.

The WCA Fundamental Conditions Barometer measures the breadth of changes to a wide variety of fundamental data. The barometer measures the proportion of indicators under review that are moving up or down together. A barometer reading above 50 generally indicates a more bullish environment for the economy and equities, and a lower reading implies the opposite. Quantifying changes this way helps us incorporate new facts into our near-term outlook in an objective and unbiased way. More information on the barometer is found in our latest quarterly report, available at www.washingtoncrossingadvisors.com/insights.html.