To Play it Safe

It is not too soon to start imagining a post-virus world. At some point, this will pass into the history books. For now, personal survivability is paramount until whenever that day comes. Surviving means doing everything possible to stay physically healthy. The investing analog holds as well — the key for investors now is corporate survivability. We believe now is the time to play it safe, focus on quality, and avoid buying low-quality, cheap stocks.

Bad News Ahead

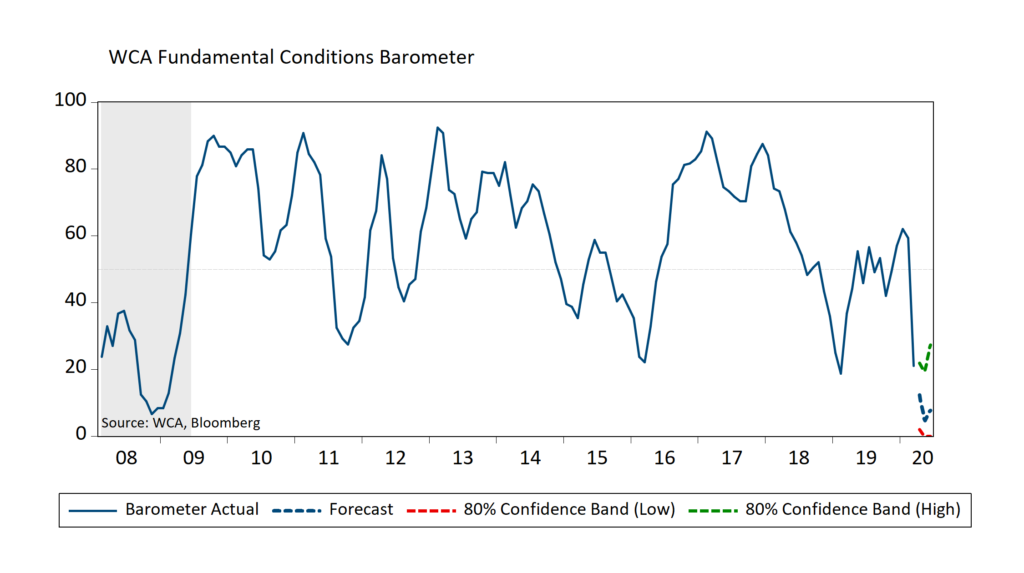

The next phase will be full of bad news about the economy. Last week’s 3.25 million weekly unemployment insurance claims report is a taste of what is likely to come. This week’s March employment report and various purchasing managers’ surveys should be abysmal. An early forecast of the WCA Fundamental Conditions Index puts it at levels not seen since 2008 (chart, below). How could we expect better? Vast swaths of the economic landscape are entirely dark and shuttered. Most now accept that a sharp and sudden recession is upon us.

How Long? How Much?

While most seem to understand a recession is here, a wide range of views exists about the nature of the downturn. Some see a short and sharp contraction followed by a fast and full bounce back. For example, James Bullard, St. Louis Federal Reserve President, last week predicted that “after an unparalleled shock, the economy will boom again.” Others see the risk of a severe and protracted recession. The collapse in GDP, a potential financial crisis, damaged confidence, and the possibility of a “second wave” are all concerns.

We tend to fall somewhere in the middle of these two extremes. There has been a significant monetary and fiscal response and a great deal of vested interests in getting the economy open again. However, the size of the shock and other complicating factors suggest it probably takes more than a few months to get all the way back. If it takes more than a couple of months to fully recover, owning quality and durable businesses will be the best way to play it safe.

Quality at Better Prices

The market is looking to play it safe too. We know this because stocks of companies with below-average debt and above-average profitability are doing better. Companies with above-average debt and below-average profitability are doing worse. We calculated the mean return of low-debt / high-profit Russell 1000 companies since February 19. Those stocks are down an average of 25% through Friday. The higher-debt / lower-profit firms posted an average decline of 40%. As uncertainty mounts, the market seems to be favoring safety as we define it.

A Growing Debt Concern

The last month’s worst performing S&P sectors were energy (-36%), financials (-21%), industrials (-19%), and REITs (-19%). Each of these sectors has significant debt and exposure to global growth. Recessions and bear markets hurt household finances, and increase default risk for loans and mortgages. Owning heavily indebted and highly cyclical stocks is an aggressive and risky proposition when business is interrupted.

More rating downgrades are likely for corporations after a decade of rapid borrowing and a deteriorating average credit profile. A recent Reuters article offers a few interesting points:

Downgrade Doom Looms for Coronavirus-Hit Firms and Markets

Reuters (March 20, 2020)

- Rapid Global Corporate Debt Growth

Global corporate debt rose by 50% since 2008 to over $70 trillion

- More Lower-Grade Debt

The share of bond issuers with the lowest investment grade rating — BBB for S&P and Fitch or Baa3 for Moody’s — has risen to around 45% in Europe from around 14% in 2000, and to 36% in the United States from 29%, according to the Bank of International Settlements.

- Questions About Quality

Ed Altman, who created the Altman Z-Score to sniff out companies in financial distress, examined 350 BBB-rated U.S. companies as of the end of 2019. His research indicated that more than 30% of those companies, with $600 billion or more of bonds, should have been rated “junk.”

Credit Rating Agencies Warn

In anticipation of rising defaults, Moody’s Investor Service released a revised estimate of defaults. They now estimate that speculative-grade defaults could rise to 6.8% over the next 12 months if there is a “short and sharp” recession. Under a “severe” recession case, they estimate the default rate could reach 20.8%. The speculative grade default rate was 3.1% in February before the coronavirus crisis hit the United States.

The Other Side

We don’t know how this will play out, but we will “hope for the best” while we “prepare for the worst.” The key here is to play it safe and look for companies that can survive difficult times. Therefore, we focus on owning companies with lower debt, good pre-virus profitability, and consistent cash flows. We can find many good-quality stocks at better prices today than a few months ago. These are the principles of WCAs Victory and Rising Dividend equity strategies.

Someday, when this all passes, we will say we played it safe by focusing first on quality and durability.

Recent Commentaries

Kevin R. Caron, CFA | Senior Portfolio Manager | 973-549-4051

Chad Morganlander | Senior Portfolio Manager | 973-549-4052

Matthew Battipaglia | Portfolio Manager | 973-549-4047

Steve Lerit, CFA | Client Portfolio Manager | 973-549-4028

Fixed Income Group

Paul Clark, CFA | Senior Portfolio Manager | 415-364-2635

Rick Marrone | Senior Portfolio Manager | 415-364-2917

Daniel Urbanowicz | Senior Portfolio Manager | 973-549-4335

Client Relations

Suzanne Ashley | Internal Relationship Manager | 973-549-4168

Eric Needham | External Sales and Marketing | 312-771-6010

www.washingtoncrossingadvisors.com

S&P 500 — The Standard & Poor’s 500 Index is a capitalization-weighted index that is generally considered representative of the U.S. large capitalization market.

The S&P 500 High Beta Index measures the performance of 100 constituents in the S&P 500 that are most sensitive to changes in the market. Constituents are weighted relative to their level of market sensitivity, with each stock assigned a weight proportional to its beta.

The S&P 500 Low Volatility Index measures performance of the 100 least volatile stocks in the S&P 500. The index benchmarks low volatility or low variance strategies for the U.S. stock market. Constituents are weighted relative to the inverse of their corresponding volatility, with the least volatile stocks receiving the highest weights.

Disclosures:

The Washington Crossing Advisors’ High Quality Index and Low Quality Index are objective, quantitative measures designed to identify quality in the top 1,000 U.S. companies. Ranked by fundamental factors, WCA grades companies from “A” (top quintile) to “F” (bottom quintile). Factors include debt relative to equity, asset profitability, and consistency in performance. Companies with lower debt, higher profitability, and greater consistency earn higher grades. These indices are reconstituted annually and rebalanced daily. For informational purposes only, and WCA Quality Grade indices do not reflect the performance of any WCA investment strategy.

Standard & Poor’s 500 Index (S&P 500) is a capitalization-weighted index that is generally considered representative of the U.S. large capitalization market.

The S&P 500 Equal Weight Index is the equal-weight version of the widely regarded Standard & Poor’s 500 Index, which is generally considered representative of the U.S. large capitalization market. The index has the same constituents as the capitalization-weighted S&P 500, but each company in the index is allocated a fixed weight of 0.20% at each quarterly rebalancing.

The information contained herein has been prepared from sources believed to be reliable but is not guaranteed by us and is not a complete summary or statement of all available data, nor is it considered an offer to buy or sell any securities referred to herein. Opinions expressed are subject to change without notice and do not take into account the particular investment objectives, financial situation, or needs of individual investors. There is no guarantee that the figures or opinions forecast in this report will be realized or achieved. Employees of Stifel, Nicolaus & Company, Incorporated or its affiliates may, at times, release written or oral commentary, technical analysis, or trading strategies that differ from the opinions expressed within. Past performance is no guarantee of future results. Indices are unmanaged, and you cannot invest directly in an index.

Asset allocation and diversification do not ensure a profit and may not protect against loss. There are special considerations associated with international investing, including the risk of currency fluctuations and political and economic events. Changes in market conditions or a company’s financial condition may impact a company’s ability to continue to pay dividends, and companies may also choose to discontinue dividend payments. Investing in emerging markets may involve greater risk and volatility than investing in more developed countries. Due to their narrow focus, sector-based investments typically exhibit greater volatility. Small-company stocks are typically more volatile and carry additional risks since smaller companies generally are not as well established as larger companies. Property values can fall due to environmental, economic, or other reasons, and changes in interest rates can negatively impact the performance of real estate companies. When investing in bonds, it is important to note that as interest rates rise, bond prices will fall. High-yield bonds have greater credit risk than higher-quality bonds. Bond laddering does not assure a profit or protect against loss in a declining market. The risk of loss in trading commodities and futures can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. The high degree of leverage that is often obtainable in commodity trading can work against you as well as for you. The use of leverage can lead to large losses as well as gains. Changes in market conditions or a company’s financial condition may impact a company’s ability to continue to pay dividends, and companies may also choose to discontinue dividend payments.

All investments involve risk, including loss of principal, and there is no guarantee that investment objectives will be met. It is important to review your investment objectives, risk tolerance, and liquidity needs before choosing an investment style or manager. Equity investments are subject generally to market, market sector, market liquidity, issuer, and investment style risks, among other factors to varying degrees. Fixed Income investments are subject to market, market liquidity, issuer, investment style, interest rate, credit quality, and call risks, among other factors to varying degrees.

This commentary often expresses opinions about the direction of market, investment sector, and other trends. The opinions should not be considered predictions of future results. The information contained in this report is based on sources believed to be reliable, but is not guaranteed and not necessarily complete.

The securities discussed in this material were selected due to recent changes in the strategies. This selection criterion is not based on any measurement of performance of the underlying security.

Washington Crossing Advisors, LLC is a wholly-owned subsidiary and affiliated SEC Registered Investment Adviser of Stifel Financial Corp (NYSE: SF). Registration with the SEC implies no level of sophistication in investment management.