Quality Over “Style”

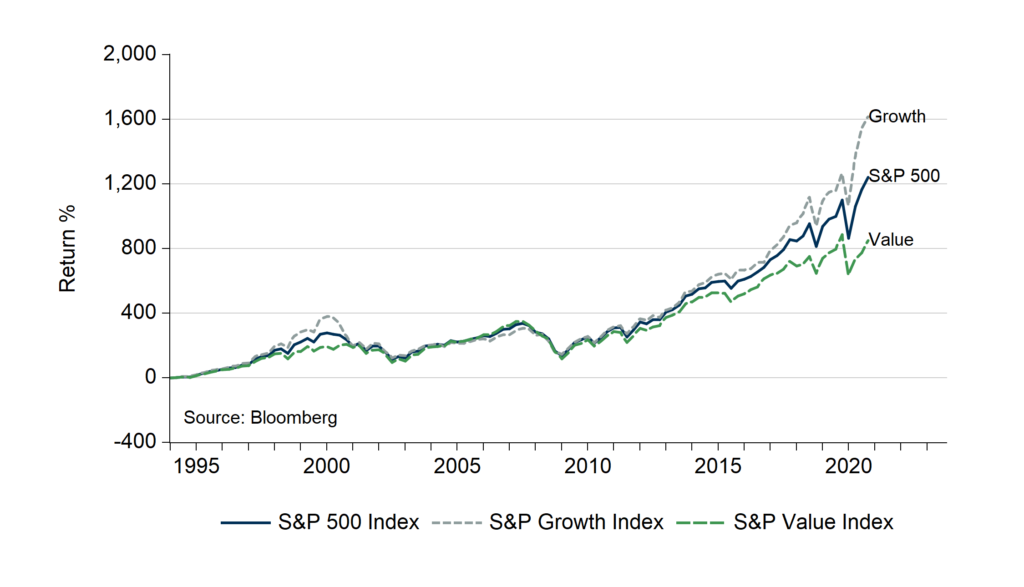

For years, stock investors have fixated on “style,” which means investing in “growth” or “value.” “Value” in this context is usually defined as buying stocks with low price-to-book or low price-to-earnings ratios. Some are now rethinking the very foundations of this framework as the return to value indexes continues to shrink (Chart A, below). Others are leaving behind simplistic notions of “style” investing and looking for all sorts of new factors to find performance. In our view, adding a multitude of new factors to the mix is also the wrong approach. The right perspective simply relates price to a few fundamental quality factors, and avoids looking merely at book value or earnings per share.

Chart A

S&P 500, S&P Growth, and S&P Value Index Total Returns

(March 1994 – November 2020)

What it Means to “Own Equity”

Stockholders own the equity, or leftover value, of a firm’s assets after obligations to others are settled. So long as the value of a company’s assets is worth more than the liabilities, stockholders are “in the money.” But, if assets’ value becomes worth less than debts owed when the debt comes due, default is in the cards. In that case, creditors assume ownership of the company’s assets while stockholders walk away with nothing.

Growth, Debt, and a Knife’s Edge

The best way to avoid such an outcome is to make sure assets are worth more than debts owed when they come due. And the best way to do that is to grow. To quote Bob Dylan: “If you’re not busy being born, you’re busy dying.” This idea is just as fitting for a business as a person. If a firm is not continually giving birth to profitable investments that grow the value of the enterprise, it is probably heading toward the exit.

And there is no better way of ensuring continued growth than by limiting the amount of debt while investing in profitable projects. When these things happen, the chances of default become remote, and it becomes more likely everyone wins. What happens when firms stay in business and value grows? Shareholders’ “leftover” share of a firm’s value compounds, creditors see loans repaid in full and on time, employees enjoy greater job security and opportunity, governments collects more tax revenue, and customers enjoy more choices in products or services. But, when the margin between a firm’s asset values and debts owed becomes thin, stock values can go on a wild ride, and all involved stand a good chance of losing out on a good thing.

In the losing case, when nobody knows what will happen next, the game becomes poised on a knife’s-edge. One mistake or one piece of good luck could decide whether a business collapses or recovers, and formerly steady share prices can start to trade like highly speculative options. To avoid ending up on this knife’s edge, it is crucial to keep in mind that asset values must be worth more than debt. Maintaining a healthy margin between asset values and amounts owed provides financial flexibility, an especially valuable trait during hard times.

The Quality Dimension

For many years, the entire stock market has been viewed along a horizontal continuum from “value” to “growth.” Stocks trading at low prices to earnings or book value are considered “value” and the other half is considered “growth.” This framework has been long enshrined in institutional investment decision making. This systematic bias has, at times, lead to greater risk-taking, especially when debt levels are on the rise and stock prices are not adequately capturing risk.

An alternative and we think better, way of doing things is to add a “quality” dimension along a vertical axis (Chart B, below). Quality, being a more durable factor than value, is deeply rooted in the ability of a firm to remain in business as a going concern. Investment decisions, profitability of assets, and creditworthiness are essential to such flexibility. The price paid for an enterprise should be set against this backdrop of “quality.” This quality/price perspective is common in other areas like bond investing and we think stock investors evaluate equity investments the same way.

Chart B

Adding a Quality Dimension to “Growth / Value”

A Better Way

As the world piles on debt, we see quality and flexibility becoming increasingly valuable factors to consider. How cheaply a firm’s assets’ leftover equity value can be bought won’t matter much if the firm can’t remain afloat, after all. So, instead of buying “growth at a reasonable price,” we will look to buy “quality at reasonable prices.” Relating price to quality is the “first principle” of investing, and a framework for evaluating investments, therefore, should never focus on price alone.

Disclosures:

The Washington Crossing Advisors’ High Quality Index and Low Quality Index are objective, quantitative measures designed to identify quality in the top 1,000 U.S. companies. Ranked by fundamental factors, WCA grades companies from “A” (top quintile) to “F” (bottom quintile). Factors include debt relative to equity, asset profitability, and consistency in performance. Companies with lower debt, higher profitability, and greater consistency earn higher grades. These indices are reconstituted annually and rebalanced daily. For informational purposes only, and WCA Quality Grade indices do not reflect the performance of any WCA investment strategy.

Standard & Poor’s 500 Index (S&P 500) is a capitalization-weighted index that is generally considered representative of the U.S. large capitalization market.

The S&P 500 Equal Weight Index is the equal-weight version of the widely regarded Standard & Poor’s 500 Index, which is generally considered representative of the U.S. large capitalization market. The index has the same constituents as the capitalization-weighted S&P 500, but each company in the index is allocated a fixed weight of 0.20% at each quarterly rebalancing.

The information contained herein has been prepared from sources believed to be reliable but is not guaranteed by us and is not a complete summary or statement of all available data, nor is it considered an offer to buy or sell any securities referred to herein. Opinions expressed are subject to change without notice and do not take into account the particular investment objectives, financial situation, or needs of individual investors. There is no guarantee that the figures or opinions forecast in this report will be realized or achieved. Employees of Stifel, Nicolaus & Company, Incorporated or its affiliates may, at times, release written or oral commentary, technical analysis, or trading strategies that differ from the opinions expressed within. Past performance is no guarantee of future results. Indices are unmanaged, and you cannot invest directly in an index.

Asset allocation and diversification do not ensure a profit and may not protect against loss. There are special considerations associated with international investing, including the risk of currency fluctuations and political and economic events. Changes in market conditions or a company’s financial condition may impact a company’s ability to continue to pay dividends, and companies may also choose to discontinue dividend payments. Investing in emerging markets may involve greater risk and volatility than investing in more developed countries. Due to their narrow focus, sector-based investments typically exhibit greater volatility. Small-company stocks are typically more volatile and carry additional risks since smaller companies generally are not as well established as larger companies. Property values can fall due to environmental, economic, or other reasons, and changes in interest rates can negatively impact the performance of real estate companies. When investing in bonds, it is important to note that as interest rates rise, bond prices will fall. High-yield bonds have greater credit risk than higher-quality bonds. Bond laddering does not assure a profit or protect against loss in a declining market. The risk of loss in trading commodities and futures can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. The high degree of leverage that is often obtainable in commodity trading can work against you as well as for you. The use of leverage can lead to large losses as well as gains. Changes in market conditions or a company’s financial condition may impact a company’s ability to continue to pay dividends, and companies may also choose to discontinue dividend payments.

All investments involve risk, including loss of principal, and there is no guarantee that investment objectives will be met. It is important to review your investment objectives, risk tolerance, and liquidity needs before choosing an investment style or manager. Equity investments are subject generally to market, market sector, market liquidity, issuer, and investment style risks, among other factors to varying degrees. Fixed Income investments are subject to market, market liquidity, issuer, investment style, interest rate, credit quality, and call risks, among other factors to varying degrees.

This commentary often expresses opinions about the direction of market, investment sector, and other trends. The opinions should not be considered predictions of future results. The information contained in this report is based on sources believed to be reliable, but is not guaranteed and not necessarily complete.

The securities discussed in this material were selected due to recent changes in the strategies. This selection criterion is not based on any measurement of performance of the underlying security.

Washington Crossing Advisors, LLC is a wholly-owned subsidiary and affiliated SEC Registered Investment Adviser of Stifel Financial Corp (NYSE: SF). Registration with the SEC implies no level of sophistication in investment management.