Five Reasons for Caution

Despite an ongoing economic recovery and bull market in stocks, we see a growing set of reasons suggesting some caution may now be warranted. In this week’s commentary, we will lay out these reasons and offer some ideas for navigating more challenging market environments.

Reason #1: High Starting Valuations

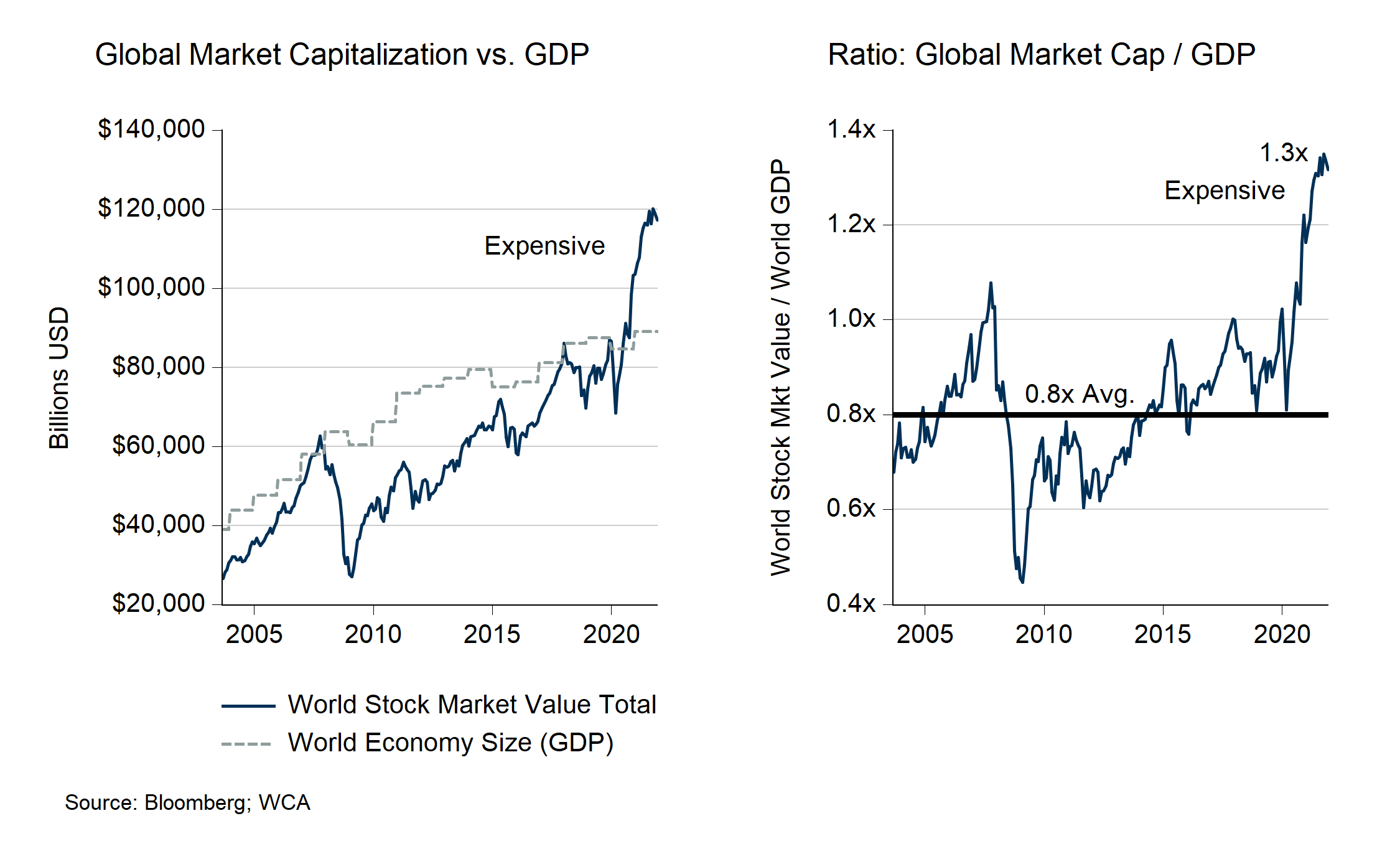

It is no secret that the world’s stock markets are now worth $120 trillion, far above the global economy’s $90 trillion size (Chart A, below-left). While up 13% from a year ago, the two-year return since just before the pandemic is a massive 36%. The ratio of global stock values to the global economy is now 1.3x, well above the historical average (Chart A, below-right). Such high valuations are likely to weigh on returns at some point.

Chart A

Global Market Cap Rises Faster than Global Economy

Reason #2: Surging Debt

The pandemic led to a record surge in global debt, another reason for caution. According to the Bank of International Settlements, total global debt grew by a record $27 trillion to $220 trillion in 2020 (Chart B, below-left). The addition of $27 trillion of debt came in a year when the global economy only grew $3 trillion. While this might be acceptable for a short while in response to an extraordinary event, continued lopsided growth in the debt/economy ratio is not sustainable in our view. Pandemic-related debt-financed government spending caused global debt to surge to a record 256% of global GDP (Chart B, below-right).

Chart B

Surge in Global Debt

Unfortunately, the globe’s debt dynamics have not been a one-year event, as debt has grown far faster than the economy since the 2008-2009 financial crisis. Over the 2008-2020 period, global debt obligations rose $92 trillion, but the global economy only grew by $23 trillion. In other words, it took $1.00 of debt to generate $0.25 of growth. The failure of debt to translate into an equivalent rise in worldwide output and income points to an unsustainable path for debt growth. As debt growth outstrips increases in global income, the likelihood of default rises, especially for borrowers who lack credibility or are overly dependent on borrowing. A sharp rise in interest rates would further complicate matters for heavily levered economies, households, and firms. (Note: We discuss how default and leverage is related in a non-linear way in this commentary titled “Leverage and Quality.”)

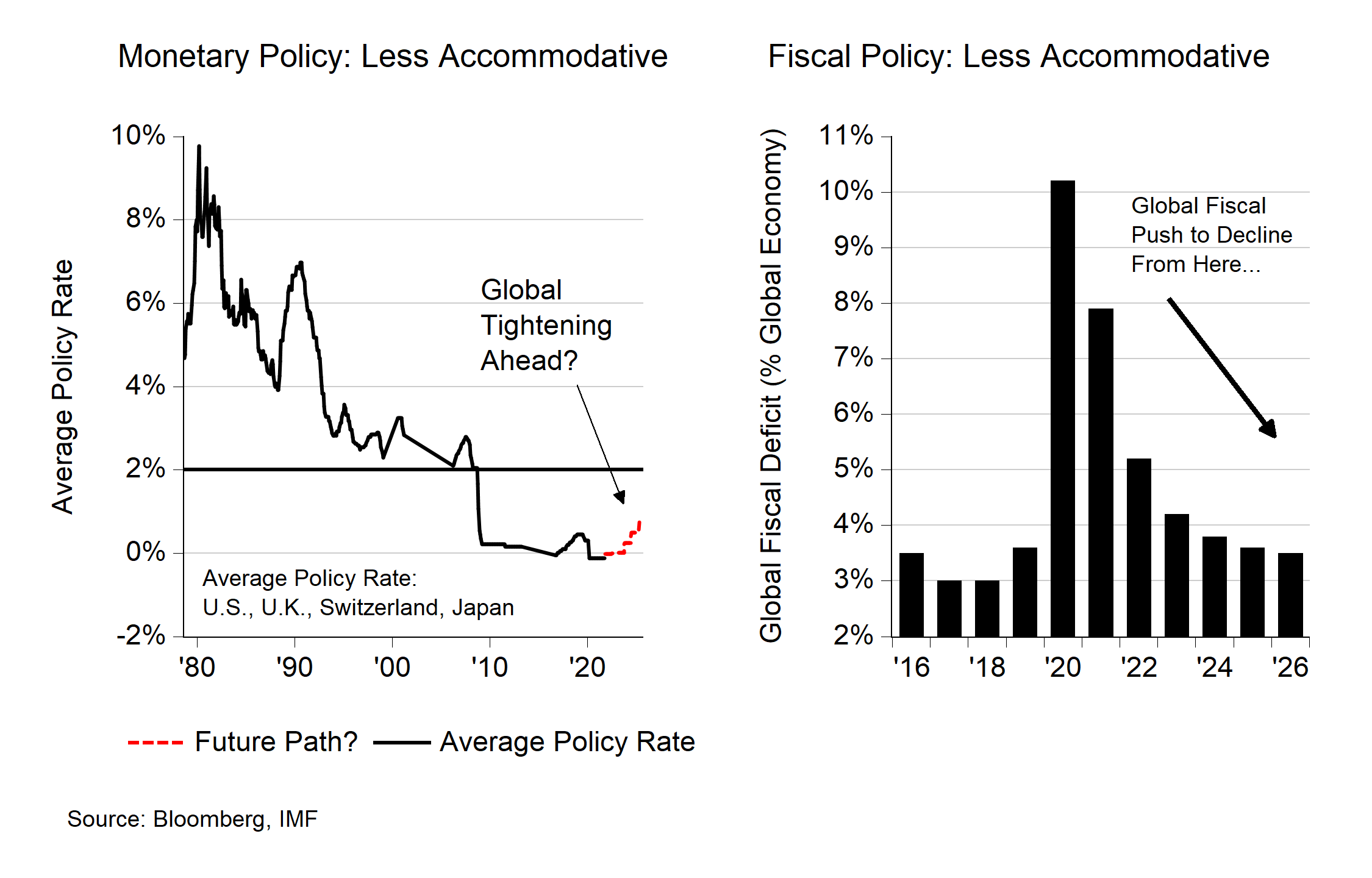

Reason #3: Weakening Policy Supports

A significant catalyst for markets in 2020-2021 came from government policy. The two main policy spigots, monetary and fiscal policy, were wide open worldwide. Now, the flow from those spigots seems ready to slow to a trickle. Recent pronouncements from the Federal Reserve (Fed), for example, point to a faster-than-expected wind-down of asset purchases. Interest rate hikes could also come faster than expected. This acceleration toward monetary tightening comes in response to a wave of unanticipated inflation (+6% year-year). These actions set the stage for less accommodative global monetary policy, in our view, after a long and extraordinary period of ease.

Chart C (below-left) shows how global rates have been held well below 2% for over a decade. Now, amid rising inflation, it seems plausible that global rates could again begin to creep higher over the next couple of years. This, coupled with a lessening of asset purchases, would constitute a meaningful shift away from the ultra-accommodative policy to which markets have become accustomed.

Lastly, global government fiscal deficits are also set to come down. Chart C (below-right) shows the IMF’s forecast path for the aggregated fiscal deficits of all governments worldwide. Deficits surged to 10% of global GDP as direct payments were made to households and businesses at the onset of the pandemic. These payments helped to support demand and employment when needed. However, these same deficits which provided a source of needed funds to the private sector during the pandemic are now set to fall away. If so, the short-term economic impulse of transfer payments to households and businesses should also subside, creating a drag on near-term growth.

Chart C

Less Accommodative Policy Ahead

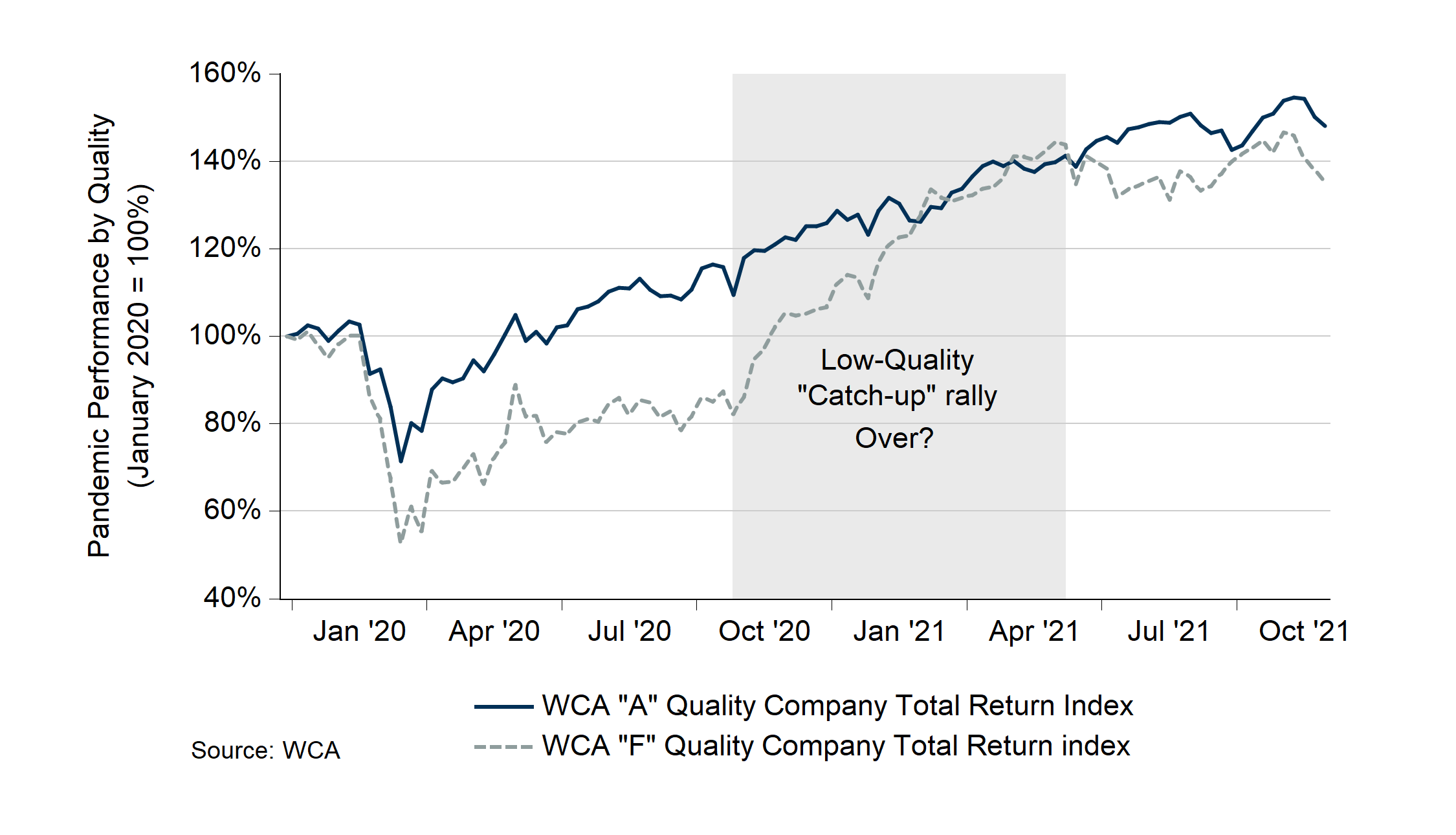

Reason #4: High Quality Outperforming Low

It is worth noting that leadership seems to be shifting inside the market. Specifically, we are starting to see greater relative strength in high versus low quality issues, just as the omicron variant fears grip markets. Based on our WCA Quality grade indices, for example, low-quality stocks are down roughly 3% compared with a 1% decline for high-quality stocks in the past month. Should this trend continue, it will end the period of low-quality leadership we’ve chronicled over the past year (Chart D, below). Markets tend to gravitate toward lower debt, higher profitability, more consistent businesses when uncertainty is on the rise.

Chart D

Low-Quality Ceding Leadership to High-Quality?

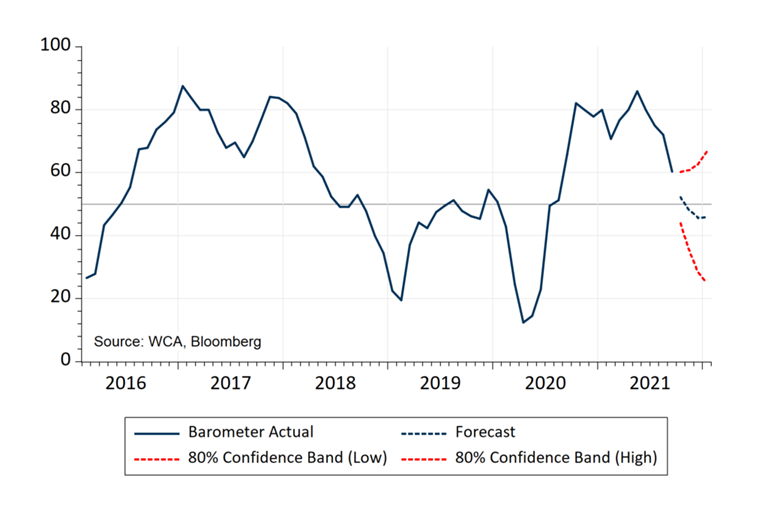

Reason #5: Fading WCA Barometer

We have been watching our WCA Fundamental Conditions Barometer fade through the summer and into the fall (Chart E, below). While not in “bearish” territory — we would consider a forecast reading well below 50 to be “bearish” — some cooling of momentum in the underlying data began to materialize. The barometer tracks, consolidates, and forecasts a range of indicators from market based risk measures, to industrial activity, employment, trade, and a range of foreign inputs. As our forecast for the barometer cooled, we scaled back equity exposure to a more neutral posture (in tactical asset allocation portfolios). We discuss the tactical move in greater detail here.

Chart E

WCA Barometer Returns to Earth

Portfolio Posture

As we near the end of 2021, our top-down tactical observations and bottom-up work led us to pair risk in recent months to a more neutral stance. Likewise, a bottom-up designed portfolio should now focus on flexibility, consistency, and durability and less on high-yield and outsized growth, in our view. The set of challenges outlined above makes such principles even more relevant today.

While it is impossible to time bouts of market turmoil, high valuations, greater debt, and slowing growth can all contribute to unexpected negative surprises. This is why we think it makes sense to focus now on building a flexible, high-quality portfolio for whatever may come next.

WCA Fundamental Conditions Barometer:

We regularly assess changes in fundamental conditions to help guide near-term asset allocation decisions. The analysis incorporates approximately 30 forward-looking indicators in categories ranging from Credit and Capital Markets to U.S. Economic Conditions and Foreign Conditions. From each category of data, we create three diffusion-style sub-indices that measure the trends in the underlying data. Sustained improvement that is spread across a wide variety of observations will produce index readings above 50 (potentially favoring stocks), while readings below 50 would indicate potential deterioration (potentially favoring bonds). The WCA Fundamental Conditions Index combines the three underlying categories into a single summary measure. This measure can be thought of as a “barometer” for changes in fundamental conditions.

Disclosures:

The Washington Crossing Advisors’ High Quality Index and Low Quality Index are objective, quantitative measures designed to identify quality in the top 1,000 U.S. companies. Ranked by fundamental factors, WCA grades companies from “A” (top quintile) to “F” (bottom quintile). Factors include debt relative to equity, asset profitability, and consistency in performance. Companies with lower debt, higher profitability, and greater consistency earn higher grades. These indices are reconstituted annually and rebalanced daily. For informational purposes only, and WCA Quality Grade indices do not reflect the performance of any WCA investment strategy.

Standard & Poor’s 500 Index (S&P 500) is a capitalization-weighted index that is generally considered representative of the U.S. large capitalization market.

The S&P 500 Equal Weight Index is the equal-weight version of the widely regarded Standard & Poor’s 500 Index, which is generally considered representative of the U.S. large capitalization market. The index has the same constituents as the capitalization-weighted S&P 500, but each company in the index is allocated a fixed weight of 0.20% at each quarterly rebalancing.

The information contained herein has been prepared from sources believed to be reliable but is not guaranteed by us and is not a complete summary or statement of all available data, nor is it considered an offer to buy or sell any securities referred to herein. Opinions expressed are subject to change without notice and do not take into account the particular investment objectives, financial situation, or needs of individual investors. There is no guarantee that the figures or opinions forecast in this report will be realized or achieved. Employees of Stifel, Nicolaus & Company, Incorporated or its affiliates may, at times, release written or oral commentary, technical analysis, or trading strategies that differ from the opinions expressed within. Past performance is no guarantee of future results. Indices are unmanaged, and you cannot invest directly in an index.

Asset allocation and diversification do not ensure a profit and may not protect against loss. There are special considerations associated with international investing, including the risk of currency fluctuations and political and economic events. Changes in market conditions or a company’s financial condition may impact a company’s ability to continue to pay dividends, and companies may also choose to discontinue dividend payments. Investing in emerging markets may involve greater risk and volatility than investing in more developed countries. Due to their narrow focus, sector-based investments typically exhibit greater volatility. Small-company stocks are typically more volatile and carry additional risks since smaller companies generally are not as well established as larger companies. Property values can fall due to environmental, economic, or other reasons, and changes in interest rates can negatively impact the performance of real estate companies. When investing in bonds, it is important to note that as interest rates rise, bond prices will fall. High-yield bonds have greater credit risk than higher-quality bonds. Bond laddering does not assure a profit or protect against loss in a declining market. The risk of loss in trading commodities and futures can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. The high degree of leverage that is often obtainable in commodity trading can work against you as well as for you. The use of leverage can lead to large losses as well as gains. Changes in market conditions or a company’s financial condition may impact a company’s ability to continue to pay dividends, and companies may also choose to discontinue dividend payments.

All investments involve risk, including loss of principal, and there is no guarantee that investment objectives will be met. It is important to review your investment objectives, risk tolerance, and liquidity needs before choosing an investment style or manager. Equity investments are subject generally to market, market sector, market liquidity, issuer, and investment style risks, among other factors to varying degrees. Fixed Income investments are subject to market, market liquidity, issuer, investment style, interest rate, credit quality, and call risks, among other factors to varying degrees.

This commentary often expresses opinions about the direction of market, investment sector, and other trends. The opinions should not be considered predictions of future results. The information contained in this report is based on sources believed to be reliable, but is not guaranteed and not necessarily complete.

The securities discussed in this material were selected due to recent changes in the strategies. This selection criterion is not based on any measurement of performance of the underlying security.

Washington Crossing Advisors, LLC is a wholly-owned subsidiary and affiliated SEC Registered Investment Adviser of Stifel Financial Corp (NYSE: SF). Registration with the SEC implies no level of sophistication in investment management.