China, Trade, and Investment

This is a second part of a series on China and trade. To read part one, click here.

CONQUEST update: Last week we raised gold to overweight and high yield to underweight in the core portion of portfolios on rising geopolitical and trade concerns.

We’ve pointed out that China owes much of its growth to investment (not trade). As discussed last week, much investment is being subsidized by Chinese households. These subsidies have allowed China to grow well over 7% for many years. From the early 1980s, when China had very low levels of investment, to today, as investment rates soar to unprecedented levels, China has become transformed. The speed of China’s transformation is now creating new pressures for change. It is well understood that for China to be on a more stable footing for future growth, consumption must pick up as a share of the economy, for example.

For consumption to rise as a percent of the economy over time, the rate of growth of consumption must be sustained at a rate higher than the overall economy for many years. So far this is not evident. And China has done little to implement reforms that would meaningfully boost wages and consumption for the average Chinese citizen. As we noted last week, we think China will continue to push for more investment spending and expanded government stimulus for a while longer.

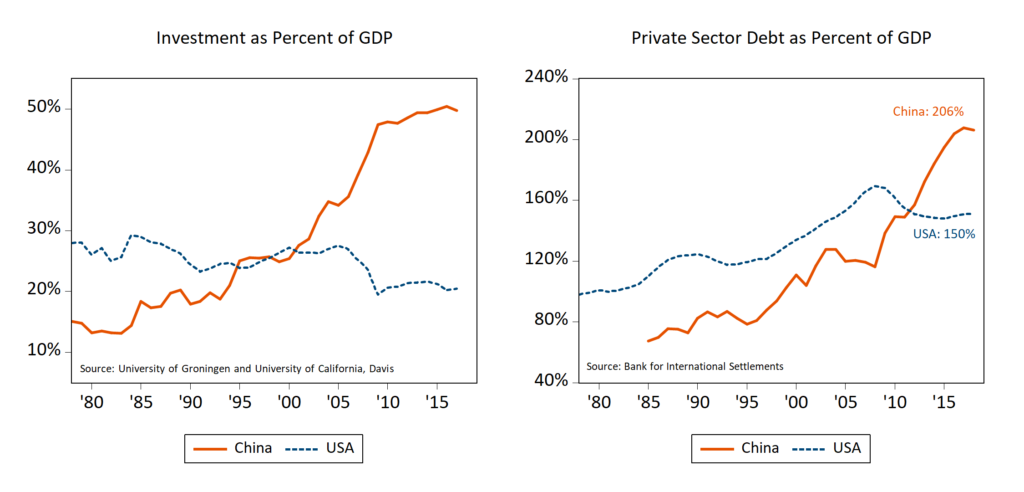

Investment Levels Unprecedented

If China opts to go this route, it runs the risk that bad investments will accumulate and lead to troubled loans and defaults. It wasn’t always this way, though. Investments made in the 1980s and 1990s produced real and sustainable returns. This is because, as the chart below shows, China was clearly underinvested in the late 1970s, before a set of reforms “opened up” China. Back then, investment was about 12% of GDP, compared to today’s 50% levels (graph, below left). By comparison, investment in the United States tends to range from 20-30% of GDP. As you can see by this measure of investment as a percent of GDP, China has swung from significantly underinvested in the late 1970s to significantly overinvested today.

Debt Levels Surging

The strong tendency for returns to fall over time with ever greater levels of investment is well understood. At some point, if the economy is not producing enough new real output from new investments to service rising debt, defaults will be inevitable. It is important to point out that much recent investment has been fueled by large amounts of private sector debt — especially true since 2010. China’s private sector’s debt-to-GDP ratio now stands at 206% (chart, above right). That same ratio topped out at just 170% in the United States before the weight of bad mortgage debts led to the start of the 2008-2009 financial crisis. The sheer dollar value of private sector debt in China now stands at $27 trillion — a $20 trillion increase since 2009. The unprecedented rise in China’s investment share of GDP is matched by an unprecedented rise in private sector debt.

Seen This Before

This is not really a new story. Other countries like Japan in the 1980s, or Brazil in the 1970s, or the Soviet Union in the 1950s and 1960s, or Germany in the 1930s all experienced periods of rapid growth. Each of these countries eventually lost the ability to sustain such rapid growth, and each growth “miracle” ended. In each case the end of the high growth period led to a period of slow growth, accompanied by a reconciliation of bad debts accumulated during the high-growth years. In each case, the global economy made progress despite retrenchment in the country suffering the adjustment process.

We are not saying that China’s story must follow any of the countries stories mentioned above exactly. No two stories are ever identical. But we would be remiss if we did not point out that China, given unprecedented investment levels (50% of GDP) and growth in private debt (to above 206% of GDP), is a likely candidate for trouble. And it seems to us that the size of China’s imbalances are much larger than the examples mentioned above. Longer term, we still believe that China could turn out well provided they follow through on earlier promises to develop their consumer sector, transition to a more globally integrated economy, and develop necessary institutional infrastructure (regulatory frameworks, legal systems, market structures, etc.). We believe this is China’s best hope to achieve long-run, sustainable growth, and is a large opportunity for the rest of global economy as well.

What It Means for Your Portfolio

As debt levels have grown in China and elsewhere around the world, the potential exists for greater volatility. Global deflationary pressures remain elevated should bad debts need to be worked out. In such an environment, we think it makes sense to build a portfolio strategy that emphasizes consistent businesses and well-capitalized balance sheets. It also makes sense to maintain a more active approach to asset allocation, an approach that can adapt to sudden changes in fundamental conditions.

The ongoing trade dispute between the United States and China further complicates what is already a difficult situation, especially for China as they seek to manage such rapid and unbalanced growth.

Kevin Caron, CFA, Senior Portfolio Manager

Chad Morganlander, Senior Portfolio Manager

Matthew Battipaglia, Portfolio Manager

Steve Lerit, CFA, Client Portfolio Manager

Suzanne Ashley, Analyst

(973) 549-4168

www.washingtoncrossingadvisors.com

www.stifel.com

Disclosures

WCA Fundamental Conditions Barometer Description: We regularly assess changes in fundamental conditions to help guide near-term asset allocation decisions. The analysis incorporates approximately 30 forward-looking indicators in categories ranging from Credit and Capital Markets to U.S. Economic Conditions and Foreign Conditions. From each category of data, we create three diffusion-style sub-indices that measure the trends in the underlying data. Sustained improvement that is spread across a wide variety of observations will produce index readings above 50 (potentially favoring stocks), while readings below 50 would indicate potential deterioration (potentially favoring bonds). The WCA Fundamental Conditions Index combines the three underlying categories into a single summary measure. This measure can be thought of as a “barometer” for changes in fundamental conditions.

The information contained herein has been prepared from sources believed to be reliable but is not guaranteed by us and is not a complete summary or statement of all available data, nor is it considered an offer to buy or sell any securities referred to herein. Opinions expressed are subject to change without notice and do not take into account the particular investment objectives, financial situation, or needs of individual investors. There is no guarantee that the figures or opinions forecasted in this report will be realized or achieved. Employees of Stifel, Nicolaus & Company, Incorporated or its affiliates may, at times, release written or oral commentary, technical analysis, or trading strategies that differ from the opinions expressed within. Past performance is no guarantee of future results. Indices are unmanaged, and you cannot invest directly in an index.

Asset allocation and diversification do not ensure a profit and may not protect against loss. There are special considerations associated with international investing, including the risk of currency fluctuations and political and economic events. Investing in emerging markets may involve greater risk and volatility than investing in more developed countries. Due to their narrow focus, sector-based investments typically exhibit greater volatility. Small company stocks are typically more volatile and carry additional risks, since smaller companies generally are not as well established as larger companies. Property values can fall due to environmental, economic, or other reasons, and changes in interest rates can negatively impact the performance of real estate companies. When investing in bonds, it is important to note that as interest rates rise, bond prices will fall. High-yield bonds have greater credit risk than higher-quality bonds. The risk of loss in trading commodities and futures can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. The high degree of leverage that is often obtainable in commodity trading can work against you as well as for you. The use of leverage can lead to large losses as well as gains.

All investments involve risk, including loss of principal, and there is no guarantee that investment objectives will be met. It is important to review your investment objectives, risk tolerance and liquidity needs before choosing an investment style or manager. Equity investments are subject generally to market, market sector, market liquidity, issuer, and investment style risks, among other factors to varying degrees. Fixed Income investments are subject to market, market liquidity, issuer, investment style, interest rate, credit quality, and call risks, among other factors to varying degrees.

This commentary often expresses opinions about the direction of market, investment sector and other trends. The opinions should not be considered predictions of future results. The information contained in this report is based on sources believed to be reliable, but is not guaranteed and not necessarily complete.

Washington Crossing Advisors LLC is a wholly owned subsidiary and affiliated SEC Registered Investment Adviser of Stifel Financial Corp (NYSE: SF).