Time for Tactical?

Years ago, it was easy to make money. Those who were around during the 1970s may even remember earning near 20%. A three-month CD in December 1980 earned over 18%, according to data from the Federal Reserve. Such rates are near 0.18% today — far below the core inflation rate (+1.3% year-over-year). At that rate, a $100 investment would grow to only $101.80 over ten years.

Evaporating Interest Rates

And don’t think buying longer-term bonds is the answer, either. Ten-year U.S. Treasury bonds now yield 0.7% compared to over 3% just two years ago. A $100 investment in a zero-coupon 10-year U.S. Treasury held for ten years would grow to only $105.75. Many are concluding that tying up $100 to earn $1.80 or $5.75 over TEN YEARS is not at all appealing. Look at the table below and see what $100 invested in cash or long-term Treasuries generated (above and beyond the initial principal) to during past decades. Creating gains was as easy as falling off a log. Just hold U.S. government-backed Treasury bills or bonds and let compounding do its thing.

Table A

Gain on Starting $100 Investment

10-Year Gain By Decade (ie. January 1950-January 1960)

| Decade | Short-Term Treasury Gain | Long-Term Treasury Gain |

|---|---|---|

| 1950s | $20.28 | $91.48 |

| 1960s | $46.34 | $15.45 |

| 1970s | $84.37 | $71.10 |

| 1980s | $134.33 | $228.07 |

| 1990s | $61.70 | $132.18 |

| 2000s | $31.25 | $109.81 |

| 2010s | $5.31 | $88.63 |

| Average | $54.80 | $105.24 |

| Source: Bloomberg; WCA |

These sorts of returns are not available today and have not been for some time now. Funds that used to find a home in the Treasury market are looking for return elsewhere. We can’t know with certainty what equity markets will return in the future, but it is possible to make a reasoned and educated guess. To do so, we could start with a dividend yield plus growth approach.

What About Stocks?

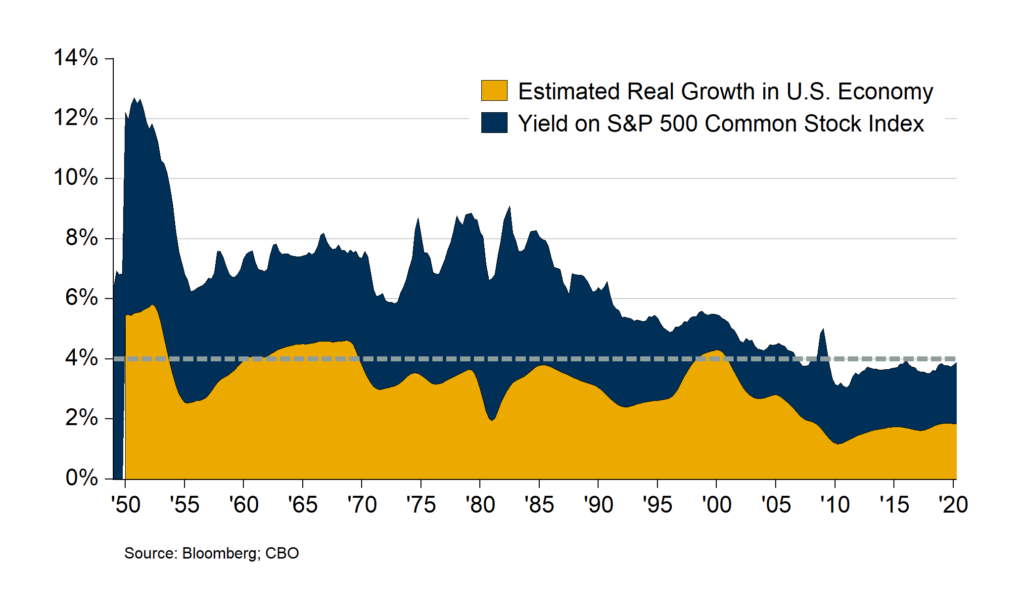

Chart A below starts with a U.S. economy growth estimate from the Congressional Budget Office (yellow area). To this estimate, we add the S&P 500 dividend yield (blue area). What we see is a declining and lower estimate of long-run, real stock returns. We don’t expect reality to match this expectation, but it makes for a reasonable starting point when estimating returns.

Chart A

Estimating Return: Dividend Plus Growth Approach

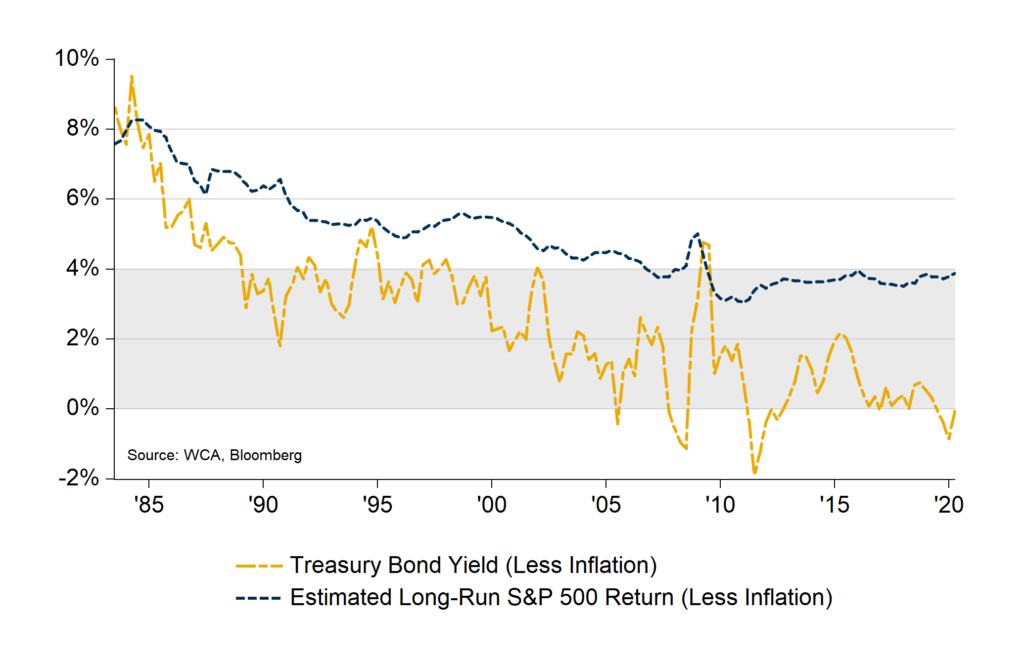

To round out the discussion, it is helpful to look at potential stock returns alongside bond returns. The graph below shows the real, inflation-adjusted yield on long-term U.S. Treasury Bonds (yellow line) alongside our real, inflation-adjusted S&P 500 estimated return from above (blue line). As you can see, the fall in interest rates, decline in dividend yield, and slower growth should lead to a moderation of portfolio returns.

Chart B

Putting it All Together: Stocks and Bonds

What’s an Investor to Do?

Accepting returns the market has to offer, and adjusting lifestyle and expectations, is one viable option. In most respects a very simple and sensible one.

Yet, it is not beyond reason to look to do better. One way to do so is to adopt a tactical strategy to over-or-underweight asset classes in your portfolio. This approach is called Tactical Asset Allocation, or TAA. Such tactical management starts with a strategic portfolio that aligns with your overall goals. From that point, it may be possible to exploit the following to try to improve returns and/or mitigate risk:

- Identifying changes in market environment;

- Identifying valuation problems before others do; or

- Identifying trends within sub-asset classes.

Time to Think Active, Not Passive

It is important to note that such a program is an “overlay” that can compliment an existing financial plan. By our definition, TAA is not about swinging for the fences or timing when to get in or out of the market. What we are describing is an approach to making measured and disciplined tactical bets to try and exploit certain market inefficiencies with the aim of augmenting return and/or mitigating some risk.

We can do little about the starting point for interest rates and valuations. An ongoing and systematic program of tactical adjustments may make sense for an environment of low interest rates and potentially lower future stock returns. The 50% run-up since March has left many feeling elated, frustrated, and/or bewildered. During times like this, it is especially important to return to basics.

Markets often tell us explicitly what returns to expect and, more often, we are left to make reasonable estimates. Whether the estimates are made explicit or not doesn’t matter. Each investor in a 401(k), index fund, mutual fund, or stock and bond account is making assumptions about return each day. Some will act on assumptions and others will not.

A passive investing approach may have worked in the past, but we think the road ahead may prove frustrating. The time for taking a different and more tactical approach may now be upon us.

Disclosures:

The Washington Crossing Advisors’ High Quality Index and Low Quality Index are objective, quantitative measures designed to identify quality in the top 1,000 U.S. companies. Ranked by fundamental factors, WCA grades companies from “A” (top quintile) to “F” (bottom quintile). Factors include debt relative to equity, asset profitability, and consistency in performance. Companies with lower debt, higher profitability, and greater consistency earn higher grades. These indices are reconstituted annually and rebalanced daily. For informational purposes only, and WCA Quality Grade indices do not reflect the performance of any WCA investment strategy.

Standard & Poor’s 500 Index (S&P 500) is a capitalization-weighted index that is generally considered representative of the U.S. large capitalization market.

The S&P 500 Equal Weight Index is the equal-weight version of the widely regarded Standard & Poor’s 500 Index, which is generally considered representative of the U.S. large capitalization market. The index has the same constituents as the capitalization-weighted S&P 500, but each company in the index is allocated a fixed weight of 0.20% at each quarterly rebalancing.

The information contained herein has been prepared from sources believed to be reliable but is not guaranteed by us and is not a complete summary or statement of all available data, nor is it considered an offer to buy or sell any securities referred to herein. Opinions expressed are subject to change without notice and do not take into account the particular investment objectives, financial situation, or needs of individual investors. There is no guarantee that the figures or opinions forecast in this report will be realized or achieved. Employees of Stifel, Nicolaus & Company, Incorporated or its affiliates may, at times, release written or oral commentary, technical analysis, or trading strategies that differ from the opinions expressed within. Past performance is no guarantee of future results. Indices are unmanaged, and you cannot invest directly in an index.

Asset allocation and diversification do not ensure a profit and may not protect against loss. There are special considerations associated with international investing, including the risk of currency fluctuations and political and economic events. Changes in market conditions or a company’s financial condition may impact a company’s ability to continue to pay dividends, and companies may also choose to discontinue dividend payments. Investing in emerging markets may involve greater risk and volatility than investing in more developed countries. Due to their narrow focus, sector-based investments typically exhibit greater volatility. Small-company stocks are typically more volatile and carry additional risks since smaller companies generally are not as well established as larger companies. Property values can fall due to environmental, economic, or other reasons, and changes in interest rates can negatively impact the performance of real estate companies. When investing in bonds, it is important to note that as interest rates rise, bond prices will fall. High-yield bonds have greater credit risk than higher-quality bonds. Bond laddering does not assure a profit or protect against loss in a declining market. The risk of loss in trading commodities and futures can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. The high degree of leverage that is often obtainable in commodity trading can work against you as well as for you. The use of leverage can lead to large losses as well as gains. Changes in market conditions or a company’s financial condition may impact a company’s ability to continue to pay dividends, and companies may also choose to discontinue dividend payments.

All investments involve risk, including loss of principal, and there is no guarantee that investment objectives will be met. It is important to review your investment objectives, risk tolerance, and liquidity needs before choosing an investment style or manager. Equity investments are subject generally to market, market sector, market liquidity, issuer, and investment style risks, among other factors to varying degrees. Fixed Income investments are subject to market, market liquidity, issuer, investment style, interest rate, credit quality, and call risks, among other factors to varying degrees.

This commentary often expresses opinions about the direction of market, investment sector, and other trends. The opinions should not be considered predictions of future results. The information contained in this report is based on sources believed to be reliable, but is not guaranteed and not necessarily complete.

The securities discussed in this material were selected due to recent changes in the strategies. This selection criterion is not based on any measurement of performance of the underlying security.

Washington Crossing Advisors, LLC is a wholly-owned subsidiary and affiliated SEC Registered Investment Adviser of Stifel Financial Corp (NYSE: SF). Registration with the SEC implies no level of sophistication in investment management.