The Case for Quality

A significant shift in financial markets occurred roughly twenty years ago. It was June 2000, and Federal Reserve Chairman Alan Greenspan had just raised the short-term interest rate to 6.5%. Within months, a falling stock market would lead the economy into a short and shallow recession. Unbeknownst to anyone at that time, the central bank would soon begin cutting rates further than they ever had before. In so doing, they would usher in a new era of easy credit. In this commentary, we make a case for investing in quality, especially during this ultra-easy credit era.

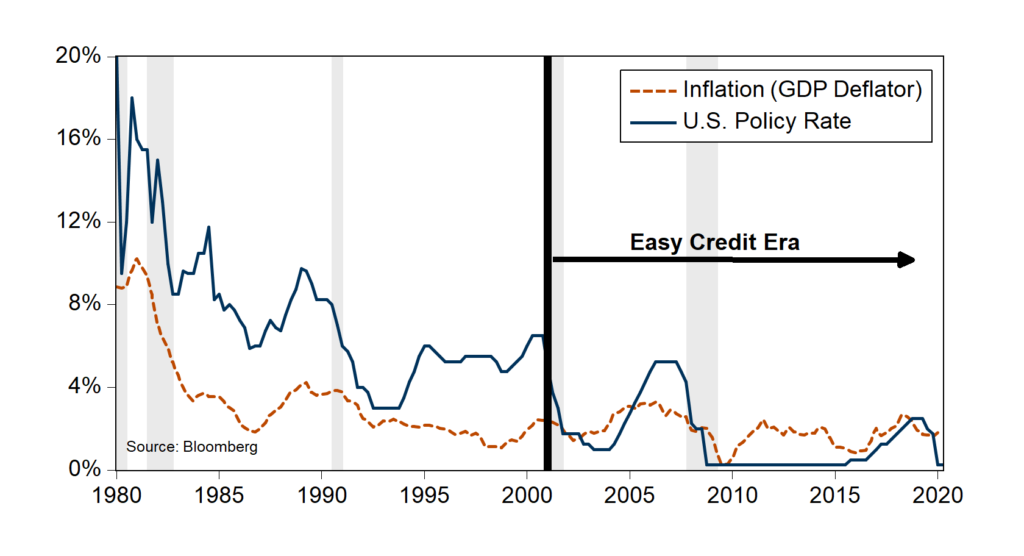

Why do we call this an “easy credit” era? Because interest rates are being held at or below the inflation rate, a signal of “accommodative” or “easy” monetary conditions. The chart below shows the relationship between interest rates and inflation. The interest rate shown is the policy rate set by the Federal Reserve. The inflation rate is the broad measure of economy-wide inflation called the “deflator.” Note that after the 2001 recession, the rate of interest tended to be below inflation (except for a short period in 2006-2007). Such low rates tend to encourage borrowing, thereby stimulating the economy.

Easy Credit Era (2001-Today)

In the twenty years since the easy credit era began, total debt has grown to $80 trillion — 3.8 times the size of the U.S. economy. By this measure, borrowings have returned to levels last seen in 2008. In 1980, 1990, and 2000, the ratio was 1.6 times, 2.3 times, and 2.7 times, respectively. The reality of rising debt, especially for some businesses, adds an element of risk. Interest cost on debt, after all, is a fixed cost that can amplify swings in income and profitability and raises the likelihood of default. However, above-average stock multiples and tight credit spreads suggest markets are not focused on these risks. If the legacy of twenty years of easy credit is heightened risk, it makes sense to lean against those trends when constructing a portfolio.

Rising Significance of “Quality”

An oft-overlooked dimension of investing, “quality” denotes dependability, sturdiness, and consistency. It can contribute to return, but it is harder to quantify. For us, it means three things: financial flexibility, productive assets, and consistency. What’s more, the market should recognize and reward these positive characteristics versus riskier companies, especially during uncertain or difficult times.

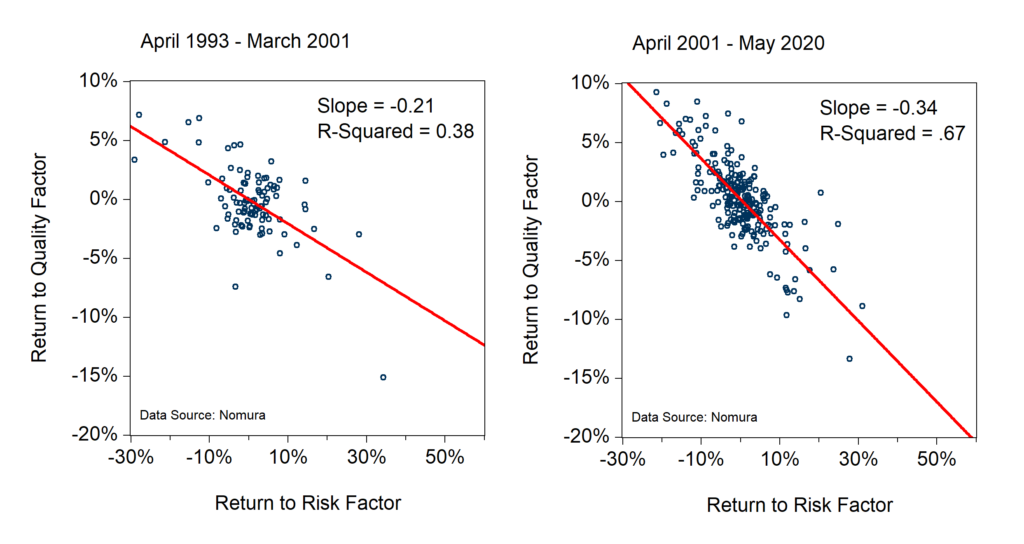

To test this hypothesis, we performed a rigorous statistical analysis (charts below) based on a set of fundamental factor return indices. These indices are designed to isolate returns to a given factor such as leverage (debt/equity), profitability (return on assets), earnings consistency (volatility of operating earnings), dividend yield, etc. Using these fundamentally-driven returns, we examined the relationship between “quality” and “risk.” In the analysis below, “quality” is the average factor return based on profitability, earnings consistency, and balance sheet leverage. Return to “risk” is evaluated as the return on a portfolio of stocks based on rolling 60-month betas versus the Russell 1000 index of large-cap domestic stocks.

As you can see in the charts below, the linkage between these factors became far more significant since the beginning of the easy credit era in 2001 through today than before the era began (1993-2001). The increased importance of quality is evidenced by a steeper slope of the line and higher explanatory power (r-squared) in 2001-2020 versus 1993-2001. The evidence is clear — markets are now more discerning over issues like debt, profitability, and consistency that determine “quality” than in the past. In past decades, when interest costs were high and falling and economic growth was faster, “quality” was less important. But that is no longer the case — now, it is crucial to focus on “quality” in stock selection.

“Quality“ More Significant Now

Analysis of Fundamental Factor Returns (1993-2001 vs. 2001-2020)

Chart Explanation: When quality decreases, risk increases. When quality increases, risk decreases. There is a trade-off between quality and risk. And since 2001, the trade-off between risk and quality has become larger and more explicit.

Conclusion

Easy credit and rising debt often lead to excesses that get corrected through painful defaults, dilution, or business failure. Evidence suggests that markets may be underestimating risks such as wider cyclical swings or default associated with today’s extended credit cycle. To compensate for these risks, focusing on the “quality” dimension of investing is of increasing importance.

Disclosures:

The Washington Crossing Advisors’ High Quality Index and Low Quality Index are objective, quantitative measures designed to identify quality in the top 1,000 U.S. companies. Ranked by fundamental factors, WCA grades companies from “A” (top quintile) to “F” (bottom quintile). Factors include debt relative to equity, asset profitability, and consistency in performance. Companies with lower debt, higher profitability, and greater consistency earn higher grades. These indices are reconstituted annually and rebalanced daily. For informational purposes only, and WCA Quality Grade indices do not reflect the performance of any WCA investment strategy.

Standard & Poor’s 500 Index (S&P 500) is a capitalization-weighted index that is generally considered representative of the U.S. large capitalization market.

The S&P 500 Equal Weight Index is the equal-weight version of the widely regarded Standard & Poor’s 500 Index, which is generally considered representative of the U.S. large capitalization market. The index has the same constituents as the capitalization-weighted S&P 500, but each company in the index is allocated a fixed weight of 0.20% at each quarterly rebalancing.

The information contained herein has been prepared from sources believed to be reliable but is not guaranteed by us and is not a complete summary or statement of all available data, nor is it considered an offer to buy or sell any securities referred to herein. Opinions expressed are subject to change without notice and do not take into account the particular investment objectives, financial situation, or needs of individual investors. There is no guarantee that the figures or opinions forecast in this report will be realized or achieved. Employees of Stifel, Nicolaus & Company, Incorporated or its affiliates may, at times, release written or oral commentary, technical analysis, or trading strategies that differ from the opinions expressed within. Past performance is no guarantee of future results. Indices are unmanaged, and you cannot invest directly in an index.

Asset allocation and diversification do not ensure a profit and may not protect against loss. There are special considerations associated with international investing, including the risk of currency fluctuations and political and economic events. Changes in market conditions or a company’s financial condition may impact a company’s ability to continue to pay dividends, and companies may also choose to discontinue dividend payments. Investing in emerging markets may involve greater risk and volatility than investing in more developed countries. Due to their narrow focus, sector-based investments typically exhibit greater volatility. Small-company stocks are typically more volatile and carry additional risks since smaller companies generally are not as well established as larger companies. Property values can fall due to environmental, economic, or other reasons, and changes in interest rates can negatively impact the performance of real estate companies. When investing in bonds, it is important to note that as interest rates rise, bond prices will fall. High-yield bonds have greater credit risk than higher-quality bonds. Bond laddering does not assure a profit or protect against loss in a declining market. The risk of loss in trading commodities and futures can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. The high degree of leverage that is often obtainable in commodity trading can work against you as well as for you. The use of leverage can lead to large losses as well as gains. Changes in market conditions or a company’s financial condition may impact a company’s ability to continue to pay dividends, and companies may also choose to discontinue dividend payments.

All investments involve risk, including loss of principal, and there is no guarantee that investment objectives will be met. It is important to review your investment objectives, risk tolerance, and liquidity needs before choosing an investment style or manager. Equity investments are subject generally to market, market sector, market liquidity, issuer, and investment style risks, among other factors to varying degrees. Fixed Income investments are subject to market, market liquidity, issuer, investment style, interest rate, credit quality, and call risks, among other factors to varying degrees.

This commentary often expresses opinions about the direction of market, investment sector, and other trends. The opinions should not be considered predictions of future results. The information contained in this report is based on sources believed to be reliable, but is not guaranteed and not necessarily complete.

The securities discussed in this material were selected due to recent changes in the strategies. This selection criterion is not based on any measurement of performance of the underlying security.

Washington Crossing Advisors, LLC is a wholly-owned subsidiary and affiliated SEC Registered Investment Adviser of Stifel Financial Corp (NYSE: SF). Registration with the SEC implies no level of sophistication in investment management.