Strong Job Gains

Last week’s jobs report was solid. A total 287,000 jobs were added in June, bringing the quarterly average to 147,000 per month. The June number follows a very weak May reading, however. There is considerable volatility in the month-to-month data, so it is important not to become overly fixated on one month. Comparing the second quarter average job gain of 147,000 to last year’s second quarter job gain of 205,000 paints a weaker picture. Overall, we see an economy that is still expanding but, as a result of slower global growth, has downshifted into a slower gear. Our hypothesis, that we are on a slow-but-positive growth trajectory, will be put to the test again this week with the release of industrial production and retail sales.

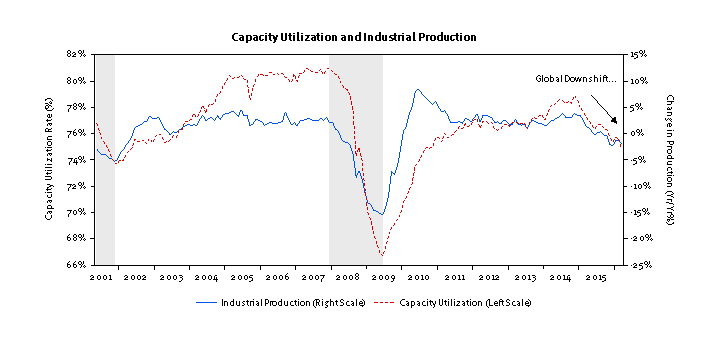

As the chart below shows, both industrial production and capacity utilization slid through 2015 as China and other foreign economies downshifted throughout 2015. While other data has shown some sign of improvement in global trends, the recent Brexit concerns and related rise in stress among some European banks is likely to weigh on momentum, at least temporarily. For the slide in global and domestic growth to be arrested, we need to see evidence of a turn in industrial output and further positive readings from the consumer. According to a Bloomberg survey, June industrial production is expected to have risen 0.2% versus last month’s -0.4% decline when data is released Friday.

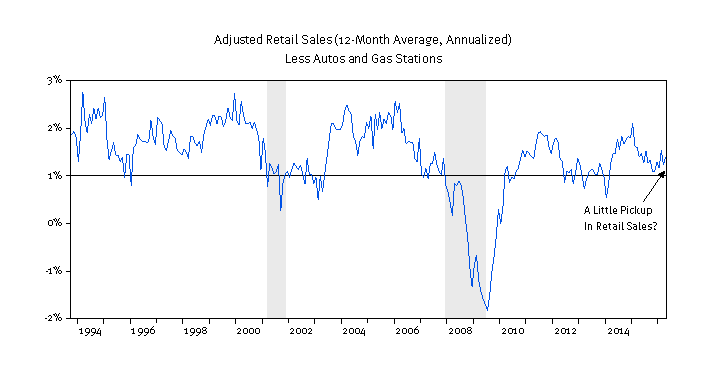

On the consumer front, we will see steady progress. Retail sales, excluding automobiles and gasoline, are holding relatively steady between 1-2% growth (chart below). Steady consumer demand is helping to bring inventory levels in line with sales. As inventories are gradually drawn down, the drag from an inventory “overhang” tends to fade, and growth improves. Thus a steady retail performance is critical to any expectation for a rebound in economic output in the second half of this year. Friday’s June retail sales report is expected to deliver steady 0.3% growth in sales, in line with last month’s reading. While this rate seems a little optimistic to us given employment and wage trends, continued positive readings are consistent with continued GDP growth near 2%.

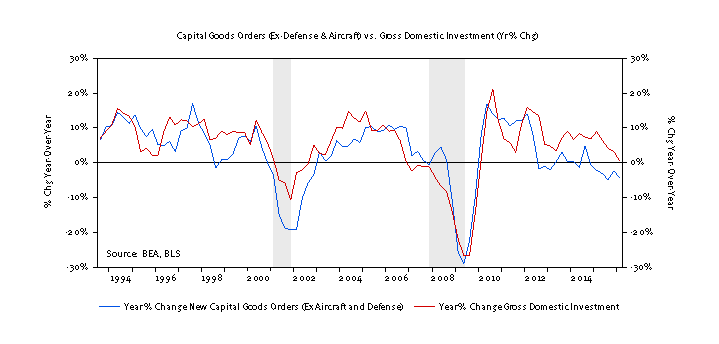

Apart from industrial production and retail sales, we continue to monitor several other trends with interest. Corporate profits and investment are at the top of this short-list. We note that S&P 500 index corporate profits are expected to be down -5.6% year-over-year through the second quarter, according to FactSet. This would mark five quarters of declines and the longest losing streak since the recession. Investment trends are also weak, mirroring profits. A slowing in durable goods orders over the past year is not a good trend in this regard. Should declining profits and investment be joined with a third impulse from rising risk aversion, the chances of a longer and more severe global downturn increase materially. A plunge in global bond yields into negative territory underscores these risks.

For our growth forecast to be met this year, it is important that the pickup seen in the data through the spring continue as we move through the summer months. This week’s data on industrial production and retail sales provide us with a couple additional, but important, data points to test the second-half “pickup” hypothesis.

ECONOMIC RELEASES THIS WEEK

| Date | Report | Period | Survey | Prior |

| Monday, July 11: | Labor Market Conditions Index | June | — | -4.8 |

| Tuesday, July 12: | JOLTS Job Openings | May | — | 5.788 M |

| Wednesday, July 13: | Fed Beige Book | |||

| Monthly Treasury Budget Statement | June | $34.3 B | — | |

| Import Price Index M/M | June | 0.5% | 1.4% | |

| Import Price Index Y/Y | June | -4.8% | -5.0% | |

| Thursday, July 14: | Weekly Jobless Claims | July 9 | — | 254 K |

| PPI-FD M/M | June | 0.3% | 0.4% | |

| PPI-FD Ex Food & Energy M/M | June | 0.1% | 0.3% | |

| PPI-FD Ex Food, Energy & Trade M/M | June | — | -0.1% | |

| PPI-FD Y/Y | June | 0.0% | -0.1% | |

| PPI-FD Ex Food & Energy Y/Y | June | 1.0% | 1.2% | |

| PPI-FD Ex Food, Energy & Trade Y/Y | June | — | 0.8% | |

| Friday, July 15: | CPI M/M | June | 0.2% | 0.2% |

| CPI Ex Food & Energy M/M | June | 0.2% | 0.2% | |

| CPI Y/Y | June | 1.0% | 1.0% | |

| CPI Ex Food & Energy Y/Y | June | 2.2% | 2.2% | |

| Retail Sales M/M | June | 0.1% | 0.5% | |

| Retail Sales Ex Auto M/M | June | 0.4% | 0.4% | |

| Retail Sales Ex Auto & Gas M/M | June | 0.3% | 0.3% | |

| Industrial Production M/M | June | 0.2% | -0.4% | |

| Empire State Manufacturing Survey | July | 5.0 | 6.0 | |

| Business Inventories | May | 0.2% | 0.1% | |

| Consumer Sentiment | July | 93.5 | 93.5 |

ASSET ALLOCATION PORTFOLIO POSTURE

LONG-RUN STRATEGIC POSTURE: Our long-run forecasts lead us to overweight large cap domestic growth stocks, high-yield corporate bonds, and gold in the diversified “core” of portfolios. Underweight positions in “core” are long-term U.S. Treasuries, foreign developed equities, and REITs. Meanwhile the equity allocation in the short-term tactical “satellite” portion of portfolios was increased to 40% equity / 60% fixed income from 33% equity / 66% fixed income. Mid-year rebalancing took place at the end of June to reflect updated long-run forecasts.

Kevin Caron, Portfolio Manager

Chad Morganlander, Portfolio Manager

Matthew Battipaglia, Analyst

Suzanne Ashley, Junior Analyst

(973) 549-4052

www.washingtoncrossingadvisors.com

The information contained herein has been prepared from sources believed to be reliable but is not guaranteed by us and is not a complete summary or statement of all available data, nor is it considered an offer to buy or sell any securities referred to herein. Opinions expressed are subject to change without notice and do not take into account the particular investment objectives, financial situation, or needs of individual investors. There is no guarantee that the figures or opinions forecasted in this report will be realized or achieved. Employees of Stifel, Nicolaus & Company, Incorporated or its affiliates may, at times, release written or oral commentary, technical analysis, or trading strategies that differ from the opinions expressed within. Past performance is no guarantee of future results. Indices are unmanaged, and you cannot invest directly in an index.

Asset allocation and diversification do not ensure a profit and may not protect against loss. There are special considerations associated with international investing, including the risk of currency fluctuations and political and economic events. Investing in emerging markets may involve greater risk and volatility than investing in more developed countries. Due to their narrow focus, sector-based investments typically exhibit greater volatility. Small company stocks are typically more volatile and carry additional risks, since smaller companies generally are not as well established as larger companies. Property values can fall due to environmental, economic, or other reasons, and changes in interest rates can negatively impact the performance of real estate companies. When investing in bonds, it is important to note that as interest rates rise, bond prices will fall. High-yield bonds have greater credit risk than higher quality bonds. The risk of loss in trading commodities and futures can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. The high degree of leverage that is often obtainable in commodity trading can work against you as well as for you. The use of leverage can lead to large losses as well as gains.

The WCA Fundamental Conditions Barometer measures the breadth of changes to a wide variety of fundamental data. The barometer measures the proportion of indicators under review that are moving up or down together. A barometer reading above 50 generally indicates a more bullish environment for the economy and equities, and a lower reading implies the opposite. Quantifying changes this way helps us incorporate new facts into our near-term outlook in an objective and unbiased way. More information on the barometer is found in our latest quarterly report, available at www.washingtoncrossingadvisors.com/insights.html.