Shifting Ground

The news of a Biden/Harris election win and heightened prospects for a COVID-19 vaccine are being digested by markets today. As for the former, news agencies declared Democrat Joe Biden president-elect and control of the Senate is to come down to two run-off races in Georgia. For the latter, hopes of a COVID-19 vaccine linked to an announcement of progress toward a vaccine sent global stock indices soaring this morning. The ground beneath this year’s two most dominant themes — politics and pandemic — is moving.

The political shift is assumed to be toward the “middle” with an expectation of divided government. While the Senate race outcome may be held off until January, a Biden win and divided Congress is likely to give way to incremental, rather than sweeping, change. Such an outcome narrows the range of potential effects for investors, providing some sense of stability for markets. The country has encountered deadlocked situations before, at times, with surprisingly positive outcomes for financial markets.

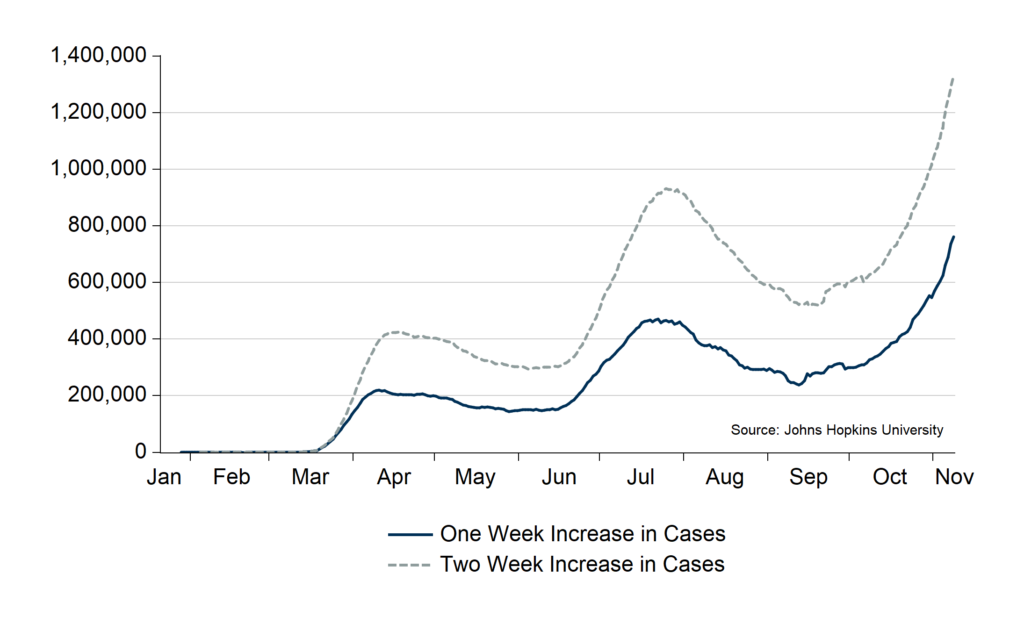

Just as divided governance may provide some temperance in the political sphere, so too does the current reality of COVID-19 in the realm of health and welfare. As we write this, the United States is reporting record numbers of new cases with almost 800,000 cases in the past week and over 1.3 million new cases in the past two weeks (Chart A, below), according to data from Johns Hopkins University. The country now has more than 9.4 million active cases as of last Wednesday. These numbers are significantly higher than in the spring and summer waves. Several states are implementing or planning to implement new restrictions to curb the spread of the virus. In this way, the potential for a difficult winter ahead due to COVID-19 weighs on the minds of many, despite good news on the vaccine front.

Chart A

U.S. COVID-19 Cases

Lift Continues

As the summer ended and fall set in, we found that most trends seemed to support continued expansion. The bounce-back from the onset of the pandemic and related shutdowns, supported by $2.4 trillion (11.8% of GDP) fiscal measures and massive monetary policy supports, continued into the fall. For example, the October ISM Manufacturing Index, a measure of expected manufacturing output, rose to a two-year high of 59.3 from 55.4 in September. Also, the 4-week average of weekly jobless claims fell to 787,000, down from an April record of 5.5 million, implying continued progress toward job market recovery. Lastly, the U.S. stock market has risen in value to a record high of nearly $39 trillion, 8% above the February pre-COVID-19 high of $36 trillion, and 70% above the March low of $23 trillion.

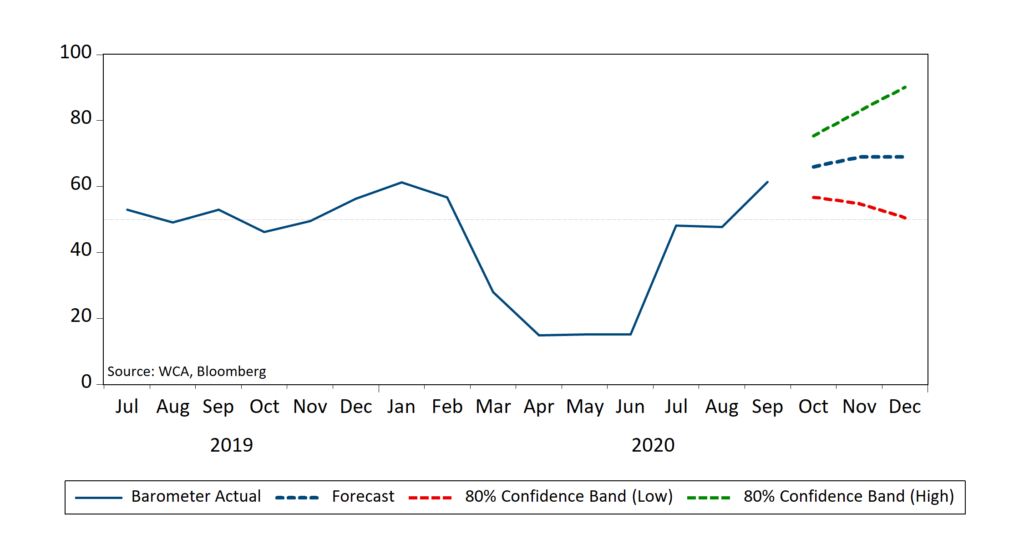

Based on this and other incoming data, we see conditions as remaining favorable for growth, and our near-term forecast path for the WCA Barometer (below) remains favorable for equities. Equity exposure was increased, and bond exposure decreased to account for some improvement in the near-term outlook at the start of the month.

Indeed, major themes are shifting in important new ways. Politics and the pandemic have the potential to shape markets in the weeks and months ahead.

Chart B

WCA Conditions Barometer

Disclosures:

The Washington Crossing Advisors’ High Quality Index and Low Quality Index are objective, quantitative measures designed to identify quality in the top 1,000 U.S. companies. Ranked by fundamental factors, WCA grades companies from “A” (top quintile) to “F” (bottom quintile). Factors include debt relative to equity, asset profitability, and consistency in performance. Companies with lower debt, higher profitability, and greater consistency earn higher grades. These indices are reconstituted annually and rebalanced daily. For informational purposes only, and WCA Quality Grade indices do not reflect the performance of any WCA investment strategy.

Standard & Poor’s 500 Index (S&P 500) is a capitalization-weighted index that is generally considered representative of the U.S. large capitalization market.

The S&P 500 Equal Weight Index is the equal-weight version of the widely regarded Standard & Poor’s 500 Index, which is generally considered representative of the U.S. large capitalization market. The index has the same constituents as the capitalization-weighted S&P 500, but each company in the index is allocated a fixed weight of 0.20% at each quarterly rebalancing.

The information contained herein has been prepared from sources believed to be reliable but is not guaranteed by us and is not a complete summary or statement of all available data, nor is it considered an offer to buy or sell any securities referred to herein. Opinions expressed are subject to change without notice and do not take into account the particular investment objectives, financial situation, or needs of individual investors. There is no guarantee that the figures or opinions forecast in this report will be realized or achieved. Employees of Stifel, Nicolaus & Company, Incorporated or its affiliates may, at times, release written or oral commentary, technical analysis, or trading strategies that differ from the opinions expressed within. Past performance is no guarantee of future results. Indices are unmanaged, and you cannot invest directly in an index.

Asset allocation and diversification do not ensure a profit and may not protect against loss. There are special considerations associated with international investing, including the risk of currency fluctuations and political and economic events. Changes in market conditions or a company’s financial condition may impact a company’s ability to continue to pay dividends, and companies may also choose to discontinue dividend payments. Investing in emerging markets may involve greater risk and volatility than investing in more developed countries. Due to their narrow focus, sector-based investments typically exhibit greater volatility. Small-company stocks are typically more volatile and carry additional risks since smaller companies generally are not as well established as larger companies. Property values can fall due to environmental, economic, or other reasons, and changes in interest rates can negatively impact the performance of real estate companies. When investing in bonds, it is important to note that as interest rates rise, bond prices will fall. High-yield bonds have greater credit risk than higher-quality bonds. Bond laddering does not assure a profit or protect against loss in a declining market. The risk of loss in trading commodities and futures can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. The high degree of leverage that is often obtainable in commodity trading can work against you as well as for you. The use of leverage can lead to large losses as well as gains. Changes in market conditions or a company’s financial condition may impact a company’s ability to continue to pay dividends, and companies may also choose to discontinue dividend payments.

All investments involve risk, including loss of principal, and there is no guarantee that investment objectives will be met. It is important to review your investment objectives, risk tolerance, and liquidity needs before choosing an investment style or manager. Equity investments are subject generally to market, market sector, market liquidity, issuer, and investment style risks, among other factors to varying degrees. Fixed Income investments are subject to market, market liquidity, issuer, investment style, interest rate, credit quality, and call risks, among other factors to varying degrees.

This commentary often expresses opinions about the direction of market, investment sector, and other trends. The opinions should not be considered predictions of future results. The information contained in this report is based on sources believed to be reliable, but is not guaranteed and not necessarily complete.

The securities discussed in this material were selected due to recent changes in the strategies. This selection criterion is not based on any measurement of performance of the underlying security.

Washington Crossing Advisors, LLC is a wholly-owned subsidiary and affiliated SEC Registered Investment Adviser of Stifel Financial Corp (NYSE: SF). Registration with the SEC implies no level of sophistication in investment management.