Real Estate and Confidence

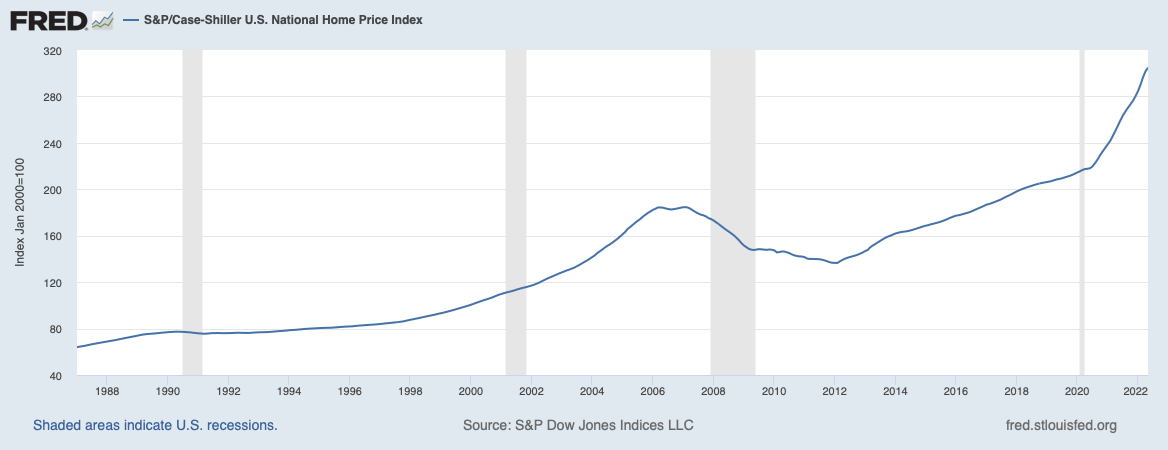

In 2018-2019, real estate company Zillow showed “for sale” inventory of U.S. homes between 1.2 and 1.4 million units. After the pandemic in 2020, that “for sale” inventory began a sharp decline to 440 thousand units in March 2022. In other words, in March, the supply of homes was about 1 million units short of, or 60-70% below, pre-pandemic levels based on Zillow’s data. At the same time supply was falling, demand was surging. Existing home sales surged by 1 million units above normal in 2020-2021, and new mortgages for purchases surged 40%. Remote work trends, federal stimulus, and record-low, sub-3% 30-year mortgages all fueled the fire. So, an average U.S. home became about 40% more expensive, based on the S&P/Case-Shiller National Home Price Index (chart, below).

S&P/Case-Shiller National Home Price Index

However, this pattern seems to be changing in the other direction. Now, the housing supply is increasing, and demand is falling. The same Zillow data, which showed a collapse in available homes for sale from 2020 through March 2022, now reveals some sizeable recent increases. Available supply from Zillow shows there are now 642 thousand units for sale, up 46% from the low point of March, for example. We see confirming trends from the National Association of Realtors (NAR) data. NAR’s most recent housing report shows a 10% inventory increase in June versus May and a 5.4% drop in existing home sales to 5.1 million homes (annual rate, seasonally adjusted). The monthly decline was the fifth in a row, and NAR cited affordability issues for buyers.

Housing’s Importance

This all matters because housing is vital to the U.S. economy in direct and indirect ways. Housing represents a significant source of household wealth at roughly $38 trillion in value or over one-quarter of net worth. Residential housing activity accounts for around 4% of U.S. economic output and nearly 1 million jobs. The myriad of housing activities spreads like ripples across the broader economy, too. As we saw in the 2007-2009 financial crisis, financing of housing activities feeds directly into the financial system.

Above all, housing is a significant personal commitment requiring significant trust and confidence. A home is often the costliest investment a person ever makes, and mortgage debt now accounts for 65% of Americans’ household liabilities. For those who own a home, surging values convey a feeling of wealth, but for those who don’t own a home, a boom can give a sense of deep anxiety. Thus, housing goes beyond other investments like stocks and bonds, representing a fundamental form of physical and social security. Because of the size and importance of the commitment, real estate offers a window into the vital dynamic of “confidence.”

Conclusion

We thought we should write about real estate, even though our main focus is usually financial assets, because of how it can influence the economy, wealth, and confidence. As you can see, real estate is important because of the direct and indirect influences it can have on the broader economy. It is part of a more comprehensive view of assets exhibiting weakness this year. The discussion could extend to other speculative assets like used cars, collectors’ watches, and decentralized digital assets.

High and rising prices, the end of various government subsidies, a surging U.S. dollar, and rising interest rates all contribute to the adjustment process. But in the future, these adjustments should again be part of regular market functioning and considered healthy. To wit, we want to point out that today’s better valuations are helping to lift longer-run expectations of returns (for more on this, please see our Q2 Tactical Asset Allocation report).

In the meantime, a focus on owning “quality at the right price” seems to be the most appropriate guiding mantra. For tactical positioning, we remain underweight stocks and overweight bonds versus our policy portfolio (for more on this, see the Q2 Tactical Asset Allocation report).

Disclosures:

The Washington Crossing Advisors’ High Quality Index and Low Quality Index are objective, quantitative measures designed to identify quality in the top 1,000 U.S. companies. Ranked by fundamental factors, WCA grades companies from “A” (top quintile) to “F” (bottom quintile). Factors include debt relative to equity, asset profitability, and consistency in performance. Companies with lower debt, higher profitability, and greater consistency earn higher grades. These indices are reconstituted annually and rebalanced daily. For informational purposes only, and WCA Quality Grade indices do not reflect the performance of any WCA investment strategy.

Standard & Poor’s 500 Index (S&P 500) is a capitalization-weighted index that is generally considered representative of the U.S. large capitalization market.

The S&P 500 Equal Weight Index is the equal-weight version of the widely regarded Standard & Poor’s 500 Index, which is generally considered representative of the U.S. large capitalization market. The index has the same constituents as the capitalization-weighted S&P 500, but each company in the index is allocated a fixed weight of 0.20% at each quarterly rebalancing.

The information contained herein has been prepared from sources believed to be reliable but is not guaranteed by us and is not a complete summary or statement of all available data, nor is it considered an offer to buy or sell any securities referred to herein. Opinions expressed are subject to change without notice and do not take into account the particular investment objectives, financial situation, or needs of individual investors. There is no guarantee that the figures or opinions forecast in this report will be realized or achieved. Employees of Stifel, Nicolaus & Company, Incorporated or its affiliates may, at times, release written or oral commentary, technical analysis, or trading strategies that differ from the opinions expressed within. Past performance is no guarantee of future results. Indices are unmanaged, and you cannot invest directly in an index.

Asset allocation and diversification do not ensure a profit and may not protect against loss. There are special considerations associated with international investing, including the risk of currency fluctuations and political and economic events. Changes in market conditions or a company’s financial condition may impact a company’s ability to continue to pay dividends, and companies may also choose to discontinue dividend payments. Investing in emerging markets may involve greater risk and volatility than investing in more developed countries. Due to their narrow focus, sector-based investments typically exhibit greater volatility. Small-company stocks are typically more volatile and carry additional risks since smaller companies generally are not as well established as larger companies. Property values can fall due to environmental, economic, or other reasons, and changes in interest rates can negatively impact the performance of real estate companies. When investing in bonds, it is important to note that as interest rates rise, bond prices will fall. High-yield bonds have greater credit risk than higher-quality bonds. Bond laddering does not assure a profit or protect against loss in a declining market. The risk of loss in trading commodities and futures can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. The high degree of leverage that is often obtainable in commodity trading can work against you as well as for you. The use of leverage can lead to large losses as well as gains. Changes in market conditions or a company’s financial condition may impact a company’s ability to continue to pay dividends, and companies may also choose to discontinue dividend payments.

All investments involve risk, including loss of principal, and there is no guarantee that investment objectives will be met. It is important to review your investment objectives, risk tolerance, and liquidity needs before choosing an investment style or manager. Equity investments are subject generally to market, market sector, market liquidity, issuer, and investment style risks, among other factors to varying degrees. Fixed Income investments are subject to market, market liquidity, issuer, investment style, interest rate, credit quality, and call risks, among other factors to varying degrees.

This commentary often expresses opinions about the direction of market, investment sector, and other trends. The opinions should not be considered predictions of future results. The information contained in this report is based on sources believed to be reliable, but is not guaranteed and not necessarily complete.

The securities discussed in this material were selected due to recent changes in the strategies. This selection criterion is not based on any measurement of performance of the underlying security.

Washington Crossing Advisors, LLC is a wholly-owned subsidiary and affiliated SEC Registered Investment Adviser of Stifel Financial Corp (NYSE: SF). Registration with the SEC implies no level of sophistication in investment management.