Monday Morning Minute 121916

THE WEEK AHEAD

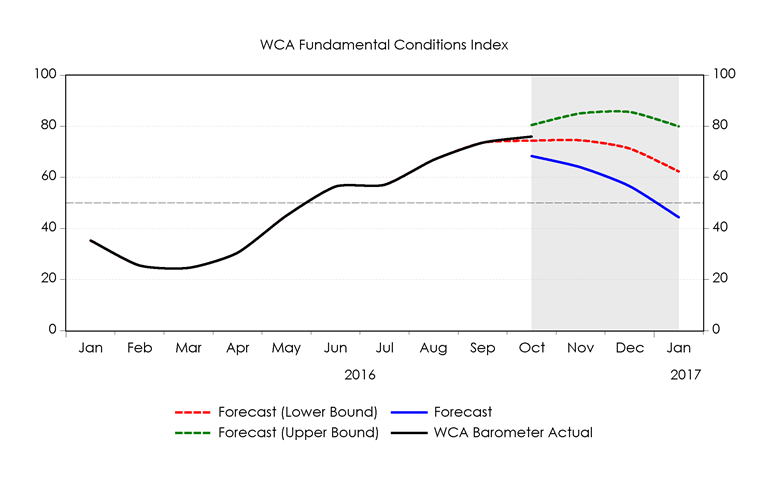

A surprise boost in optimism is impacting financial markets and has the potential to feed into growth as we start 2017. The WCA Fundamental Conditions Index ends 2016 on a strong footing, suggesting better growth through the fourth quarter.

MACRO VIEW

Today’s Monday Morning Minute will be our last weekly commentary of the year, and we would like to say thank you to all our readers. Our best wishes to you for a joyous holiday season and a prosperous 2017!

Our final update is also a positive one for the stock market and the economy. Although the year started off with a whimper, economic momentum started to pick up around mid-year. A further surge in confidence post-election reflects hopes of a fiscal push in late 2017 or 2018 through a variety of tax cuts, regulatory reform, and spending proposals. Rallies across equity, credit, and oil markets, along with a rise in the U.S. dollar, underscore this attitudinal shift.

As we discussed in previous commentaries, the increased potential for a cut in corporate taxes is directly beneficial to shareholders and indirectly beneficial for long-run growth. Lowering of taxes not only directly lifts after-tax earnings, but the more favorable treatment of capital investment has the potential to enliven growth in capital formation across the economy at large, lifting long-run growth potential. Back in the here-and-now, however, we continue to look for signs of changes in the outlook through the lens of our WCA Fundamental Conditions Index (graph, below).

As readings moved north through the summer and into the fall, we moved to overweight U.S. equities and underweighted long-term Treasuries. Our models suggest that the lift in growth should begin to moderate as we head toward the start of the year. The sharp improvement in risk attitude since the November 8 election will likely provide some additional lift to the barometer as we head into the new year, suggesting a smaller likelihood of a recession. We suspect that once this confidence boost shows up in real data, the barometer will trend upward toward the upper bound indicated in the graph.

Most of the improvement in recent weeks is reflected in financial markets rather than economic data. A “risk-on” environment has caused a sharp jump in stock prices, a large drop in credit spreads, a rise in inflation expectations, a ratcheting higher of earnings forecasts, a lifting of commodity prices, and a steepening of the yield curve. The Federal Reserve (Fed), taking its cue from the data responded by raising rates last week, is striking a more hawkish tone regarding the future path of interest rates. Long-term bond yields have backed up dramatically, reflecting a pricing in of reflation and better growth.

The next step will be to see actual economic data pick up. The Federal Reserve Bank of Atlanta’s “GDP Now” service, pins fourth quarter GDP near 2.6%. Given the miserable ~1% pace of growth at the start of the year, it is nice to see growth and optimism picking up as we close out the year.

Best holiday wishes to all!

ECONOMIC RELEASES THIS WEEK

| Date | Report | Period | Survey | Prior |

| Monday, Dec 19: | PMI Services Flash | December | 54.0 | 54.7 |

| Tuesday, Dec 20: | No Economic Releases | |||

| Wednesday, Dec 21: | Existing Home Sales M/M | November | 2.0% | |

| Existing Home Sales Y/Y | November | 5.9% | ||

| Thursday, Dec 22: | Weekly Jobless Claims | December 17 | 254 K | |

| Durable Goods: New Orders M/M | November | -3.1% | 4.8% | |

| Durable Goods: New Orders Y/Y | November | 2.1% | ||

| Durable Goods: Ex-Transportation M/M | November | 0.4% | 1.0% | |

| Durable Goods: Ex-Transportation Y/Y | November | 0.3% | ||

| Core Capital Goods M/M | November | 0.4% | 0.4% | |

| Core Capital Goods Y/Y | November | -4.3% | ||

| Real GDP Q/Q | 3Q16 | 3.2% | 3.2% | |

| Personal Income M/M | November | 0.3% | 0.6% | |

| Consumer Spending M/M | November | 0.5% | 0.3% | |

| PCE Price Index M/M | November | 0.2% | 0.2% | |

| Core PCE Price Index M/M | November | 0.1% | ||

| PCE Price Index Y/Y | November | 1.4% | ||

| Core PCE Price Index Y/Y | November | 1.7% | ||

| Friday, Dec 16: | New Home Sales | November | 572 K | 563 K |

| Consumer Sentiment | December | 98.0 | 98.0 |

ASSET ALLOCATION PORTFOLIO POSTURE

Based on our long-run capital market expectations, the “core” equity allocation in portfolios are underweight foreign equities / overweight large cap domestic growth, and underweight REITs / overweight Gold. The “core” bond allocation is underweight long-term Treasuries / overweight corporate high-yield bonds.

Based on shorter-term expectations, the “tactical” allocation within portfolios is underweight bonds / overweight stocks.

Disclaimer

The information contained herein has been prepared from sources believed to be reliable but is not guaranteed by us and is not a complete summary or statement of all available data, nor is it considered an offer to buy or sell any securities referred to herein. Opinions expressed are subject to change without notice and do not take into account the particular investment objectives, financial situation, or needs of individual investors. There is no guarantee that the figures or opinions forecasted in this report will be realized or achieved. Employees of Stifel, Nicolaus & Company, Incorporated or its affiliates may, at times, release written or oral commentary, technical analysis, or trading strategies that differ from the opinions expressed within. Past performance is no guarantee of future results. Indices are unmanaged, and you cannot invest directly in an index.

Asset allocation and diversification do not ensure a profit and may not protect against loss. There are special considerations associated with international investing, including the risk of currency fluctuations and political and economic events. Investing in emerging markets may involve greater risk and volatility than investing in more developed countries. Due to their narrow focus, sector-based investments typically exhibit greater volatility. Small company stocks are typically more volatile and carry additional risks, since smaller companies generally are not as well established as larger companies. Property values can fall due to environmental, economic, or other reasons, and changes in interest rates can negatively impact the performance of real estate companies. When investing in bonds, it is important to note that as interest rates rise, bond prices will fall. High-yield bonds have greater credit risk than higher quality bonds. The risk of loss in trading commodities and futures can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. The high degree of leverage that is often obtainable in commodity trading can work against you as well as for you. The use of leverage can lead to large losses as well as gains.

The WCA Fundamental Conditions Barometer measures the breadth of changes to a wide variety of fundamental data. The barometer measures the proportion of indicators under review that are moving up or down together. A barometer reading above 50 generally indicates a more bullish environment for the economy and equities, and a lower reading implies the opposite. Quantifying changes this way helps us incorporate new facts into our near-term outlook in an objective and unbiased way. More information on the barometer is found in our latest quarterly report, available at www.washingtoncrossingadvisors.com/insights.html