Monday Morning Minute 110716

THE WEEK AHEAD

Voters head to the polls.

MACRO VIEW

Markets are pricing in greater political risk headed into this week’s election. Looking beyond the market action, however, we see encouraging fundamental signs. Employment gains, steady job growth, stable demand, and a return to earnings growth all speak to a better backdrop for stocks. Domestic economic growth should be near our 2-3% range in the second half, marking a clear turnaround from the pattern of weakening growth through 2015 to the first half of 2016. It is even likely that business investment is picking up, now that the ill effects of a strong dollar and sliding energy prices are fading. Still, uncertainty over the election is impacting risk appetite.

Although we won’t know the outcome of the election for a few more days, markets have begun to contemplate what change at the top might mean. The candidates differ on taxation and spending policies, but the details are far from clear. Moreover, there is little doubt that moving either candidate’s agenda through the legislature will be an uphill battle. Not only will congress likely remain divided, but divisions within each party are also apparent. Ultimately, whoever becomes the next Commander in Chief will have an impact in shaping the next chapter in American history. Trade policy, regulation, energy, foreign policy, and appointments in the courts and the Federal Reserve (Fed) are all important and will carry long-term implications. For now, however, knee-jerk market reactions to a change in administration will largely be a function of conjecture and clouded expectations, rather than tangible policy changes. Thus, any such market moves should be taken with a grain of salt.

Short-Term View A Clinton win likely is the case most priced into markets given polling data. Stronger currencies for trading partners, including Mexico and Canada, is likely in the cards under a Clinton win. Markets, preferring knowns over unknowns, may also unwind some of the risk premia built in in recent weeks under a Clinton win. Equities could stage a rally and bonds could give up some ground, pushing Treasury yields moderately higher, and tightening credit spreads.

A Trump win might have the opposite effect. Since polling indicates this to be the less likely outcome, we might expect a Trump win to put some short-run pressure on risk assets given the greater uncertainty over Trump’s proposals. A less known quantity in Washington, a Trump win would introduce some uncertainty into the outlook, likely requiring at least a short-run bump up in risk premia.

Long-Term View

Regardless of who wins, the passing of the election (and hopefully it passes uncontested) should allow for political uncertainty to subside. If the din of politics fades a bit, perhaps it will then become possible for markets to focus on some of the more constructive trends in fundamentals seen in recent weeks.

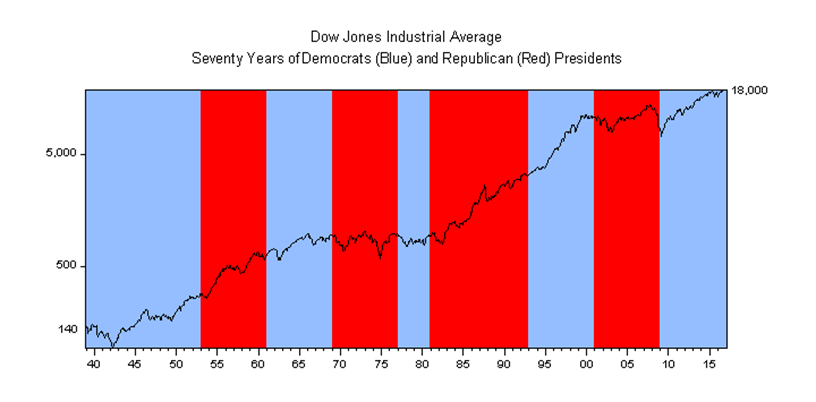

Since our focus tends to be of the longer-term variety, we are reminded that fundamentals tend to win over politics. Growth in the economy and corporate earnings, over time, are key to long-run equity returns. Monetary and fiscal policy, along with regulation, trade, and rule of law are also important. Still, we are humbled by the decades of past administrations (graph, below) who have presided over a wide array of conditions. War, peace, growth, stagnation, inflation, deflation, social tranquility, and strife were all experienced since the end of World War II. While the sample size is not large enough to provide a robust answer to which party is best for the markets, it is clear that both parties held the White House during periods of both prosperity and stagnation. History has shown that betting on markets based only politics can be a costly and difficult proposition.

Ultimately fundamentals, not politics, determines the direction of the economy and markets. This is why a focus on fundamentals is at the core of the WCA investment discipline.

ECONOMIC RELEASES THIS WEEK

| Date | Report | Period | Survey | Prior |

| Monday, November 7: | Labor Market Conditions Index | October | — | -2.2 |

| Tuesday, November 8: | JOLTS | September | — | 5.4 M |

| Wednesday, November 9: | No Economic Releases | |||

| Thursday, November 10: | Weekly Jobless Claims | November 5 | — | 265 K |

| Monthly Treasury Budget Statement | October | -$88.7 B | $33.4 B | |

| Friday, November 11: | Veterans Day: Banks Closed, Markets Open | |||

| Consumer Sentiment | November | 87.0 | 87.2 |

ASSET ALLOCATION PORTFOLIO POSTURE

LONG-RUN STRATEGIC POSTURE: Our long-run forecasts lead us to overweight large cap domestic growth stocks, high-yield corporate bonds, and gold in the diversified “core” of portfolios. Underweight positions in “core” are long-term U.S. Treasuries, foreign developed equities, and REITs. The equity allocation in the short-term tactical “satellite” portion of portfolios currently stands at 60% equity / 40% fixed income.

The information contained herein has been prepared from sources believed to be reliable but is not guaranteed by us and is not a complete summary or statement of all available data, nor is it considered an offer to buy or sell any securities referred to herein. Opinions expressed are subject to change without notice and do not take into account the particular investment objectives, financial situation, or needs of individual investors. There is no guarantee that the figures or opinions forecasted in this report will be realized or achieved. Employees of Stifel, Nicolaus & Company, Incorporated or its affiliates may, at times, release written or oral commentary, technical analysis, or trading strategies that differ from the opinions expressed within. Past performance is no guarantee of future results. Indices are unmanaged, and you cannot invest directly in an index.

Asset allocation and diversification do not ensure a profit and may not protect against loss. There are special considerations associated with international investing, including the risk of currency fluctuations and political and economic events. Investing in emerging markets may involve greater risk and volatility than investing in more developed countries. Due to their narrow focus, sector-based investments typically exhibit greater volatility. Small company stocks are typically more volatile and carry additional risks, since smaller companies generally are not as well established as larger companies. Property values can fall due to environmental, economic, or other reasons, and changes in interest rates can negatively impact the performance of real estate companies. When investing in bonds, it is important to note that as interest rates rise, bond prices will fall. High-yield bonds have greater credit risk than higher quality bonds. The risk of loss in trading commodities and futures can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. The high degree of leverage that is often obtainable in commodity trading can work against you as well as for you. The use of leverage can lead to large losses as well as gains.

The WCA Fundamental Conditions Barometer measures the breadth of changes to a wide variety of fundamental data. The barometer measures the proportion of indicators under review that are moving up or down together. A barometer reading above 50 generally indicates a more bullish environment for the economy and equities, and a lower reading implies the opposite. Quantifying changes this way helps us incorporate new facts into our near-term outlook in an objective and unbiased way. More information on the barometer is found in our latest quarterly report, available at www.washingtoncrossingadvisors.com/insights.html.

Client-approved reports and commentaries click here

Kevin Caron, Portfolio Manager Chad Morganlander, Portfolio Manager Matthew Battipaglia, Analyst

Suzanne Ashley, Junior Analyst

(973) 549-4052