Monday Morning Minute 091216

This week’s Consumer Price Index data will shed more light on underlying inflation ahead of the Federal Reserve’s (Fed’s) September 21 meeting.

MACRO VIEW

In 1919, the Federal Reserve Bulletin stated that inflation is the process of making addition to currencies not based on a commensurate increase in the production of goods. We like this definition because it recognizes inflation as essentially a “monetary phenomenon,” to borrow Milton Friedman’s words. It also clarifies the central bank’s role as chief steward of the money supply and inflation rate. Inflation, or lack thereof, is the key feature in the debate over the path for monetary policy.

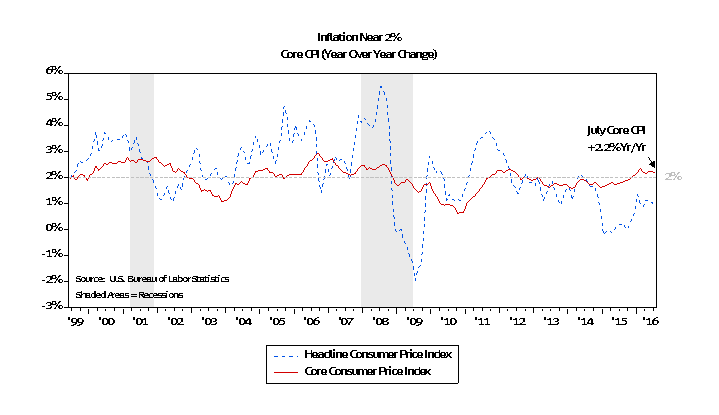

The Federal Reserve is expected to meet on September 21. They will likely address improving near-term growth and financial conditions. At the same time, they may also express concern about longer-term growth issues (i.e. low productivity and workforce dynamics). Core inflation (chart, below) seems to be holding steady near the Fed’s 2% target level. Most of the decline in headline inflation can be explained by falling commodity prices in 2014-2015. Without a recession, we see commodity prices firming, giving global headline inflation a lift too.

The debate over Fed policy is complicated by disparate growth paths around the world. Last week’s decision by the European Central Bank to forego additional asset purchases came despite their weak inflation forecast and concerns about downside risk. Similarly, the Bank of Japan (meeting on September 21) also seems less willing to increase asset purchases. Disappointing results from asset purchases quantitative easing (QE) on growth, already lifted asset prices, rising inequality, historically low rates, and bond scarcity are all raising questions over whether extensions to QE are appropriate. The European Central Bank, Bank of Japan, and Bank of England have QE programs at some stage of operation totaling approximately $250 billion of monthly purchases.

Although the Federal Reserve will consider global conditions, their first responsibility is maintaining domestic price stability. This week’s Consumer Price Index data will shed more light on underlying inflation.

ECONOMIC RELEASES THIS WEEK

| Date | Report | Period | Survey | Prior |

| Tuesday, September 13: | NFIB Small Business Optimism Survey | August | 94.8 | 94.6 |

| Thursday, September 15: | Retail Sales | August | -0.1% | 0.0% |

| Retail Sales (Ex-Autos) | August | 0.2% | -0.3% | |

| Industrial Production | August | -0.2% | 0.7% | |

| Capacity Utilization | August | 75.7% | 75.9% | |

| Friday, September 16: | Consumer Price Index | August | 0.1% | 0.0% |

| Consumer Price Index (Core) | August | 0.2% | 0.1% | |

| Consumer Price Index Core Yr. / Yr. | August | — | 2.2% | |

| Consumer Sentiment | September | 91 | 89.8 |

ASSET ALLOCATION PORTFOLIO POSTURE

LONG-RUN STRATEGIC POSTURE: Our long-run forecasts lead us to overweight large cap domestic growth stocks, high-yield corporate bonds, and gold in the diversified “core” of portfolios. Underweight positions in “core” are long-term U.S. Treasuries, foreign-developed equities, and REITs. Meanwhile the equity allocation in the short-term tactical “satellite” portion of portfolios was increased to 40% equity / 60% fixed income from 33% equity / 66% fixed income. Mid-year rebalancing took place at the end of June to reflect updated long-run forecasts.

The information contained herein has been prepared from sources believed to be reliable but is not guaranteed by us and is not a complete summary or statement of all available data, nor is it considered an offer to buy or sell any securities referred to herein. Opinions expressed are subject to change without notice and do not take into account the particular investment objectives, financial situation, or needs of individual investors. There is no guarantee that the figures or opinions forecasted in this report will be realized or achieved. Employees of Stifel, Nicolaus & Company, Incorporated or its affiliates may, at times, release written or oral commentary, technical analysis, or trading strategies that differ from the opinions expressed within. Past performance is no guarantee of future results. Indices are unmanaged, and you cannot invest directly in an index.

Asset allocation and diversification do not ensure a profit and may not protect against loss. There are special considerations associated with international investing, including the risk of currency fluctuations and political and economic events. Investing in emerging markets may involve greater risk and volatility than investing in more developed countries. Due to their narrow focus, sector-based investments typically exhibit greater volatility. Small company stocks are typically more volatile and carry additional risks, since smaller companies generally are not as well established as larger companies. Property values can fall due to environmental, economic, or other reasons, and changes in interest rates can negatively impact the performance of real estate companies. When investing in bonds, it is important to note that as interest rates rise, bond prices will fall. High-yield bonds have greater credit risk than higher quality bonds. The risk of loss in trading commodities and futures can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. The high degree of leverage that is often obtainable in commodity trading can work against you as well as for you. The use of leverage can lead to large losses as well as gains.

The WCA Fundamental Conditions Barometer measures the breadth of changes to a wide variety of fundamental data. The barometer measures the proportion of indicators under review that are moving up or down together. A barometer reading above 50 generally indicates a more bullish environment for the economy and equities, and a lower reading implies the opposite. Quantifying changes this way helps us incorporate new facts into our near-term outlook in an objective and unbiased way. More information on the barometer is found in our latest quarterly report, available at www.washingtoncrossingadvisors.com/insights.html.

Client-approved reports and commentaries click here

Kevin Caron, Portfolio Manager Chad Morganlander, Portfolio Manager Matthew Battipaglia, Analyst

Suzanne Ashley, Junior Analyst

(973) 549-4052