Mixed Messages

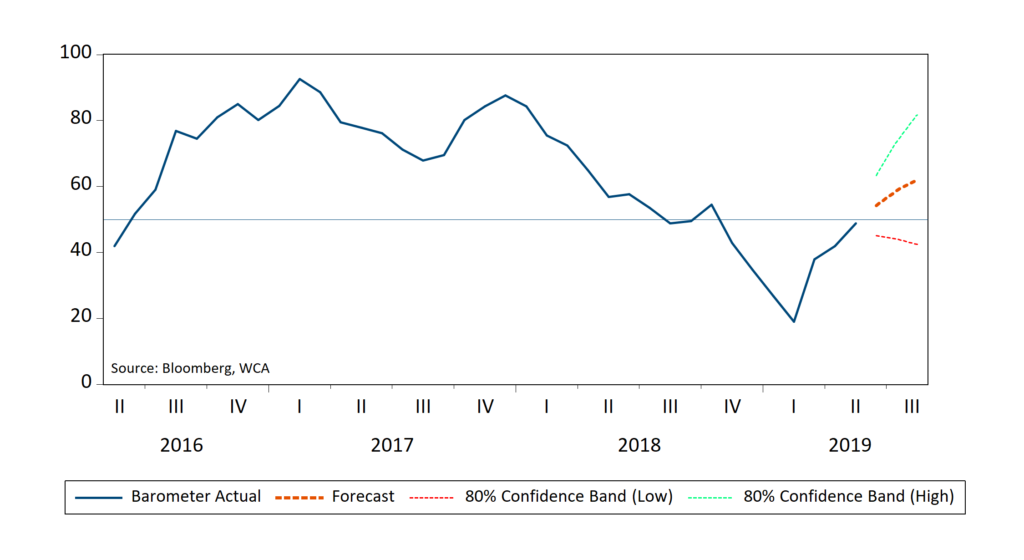

A read of incoming data puts our WCA Fundamental Conditions Barometer near 50 with an upward trend. While the current overall reading is about average, a closer look within the component parts of the barometer reveal some interesting takeaways. Notably, market based measures of risk appetite have moved in the right direction while indicators of actual economic performance have softened. Stocks and bonds have rallied together this year. The S&P 500 and the Barclays Aggregate Bond Index are up roughly 15% and 5% respectively. For now, investors are looking past signs of slowing growth, and focusing instead on the benefits of lower interest rates. Leading the stock market advance this year are safer sectors like consumer staples and utilities.

Growth Slows

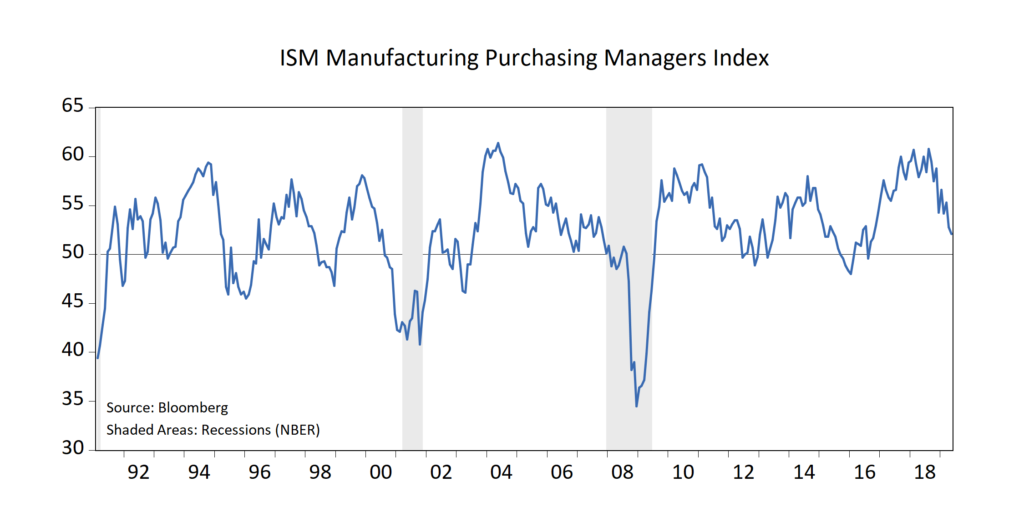

Manufacturing orders (chart, below), which tend to do a good job highlighting the economy’s ebbs and flows, are softening. Trade worries and tariffs may be a contributing factor. This pattern fits and confirms a growing set of other data trends. Capital goods orders, employment trends, commodity prices, and corporate earnings are also slowing. The World Bank recently cut their 2019 global growth estimate to 2.6% from a prior estimate of 2.9% growth. The period of accelerating growth, which dominated our view during 2016-2017, seems to be giving way to a period of slower growth, somewhat below our long-run global growth trend assumption (3.25%).

WCA Barometer Back Near 50

A read of incoming data puts our WCA Fundamental Conditions Barometer (below) near 50 with an upward trend. The rebound in financial conditions following last fall’s selloff, is helped by a more supportive tone from the Federal Reserve. Generally improved financial conditions masks some signs of slippage in the economic data as discussed above. Expected rate cuts are seen as “insurance” rather than a harbinger of recession. This, in turn, could help extend the cycle as lower yields are viewed as positive inputs helping to support asset values. Earnings forecasts continue to remain relatively solid, providing support to the equity market.

WCA Barometer

Portfolio Posture

The drop in bond yields and expected rate cuts are, for now, being seen by investors as temporary and providing a valuation boost to stocks. If rate cuts and falling bond yields become seen as harbingers of a recession, and earnings start to falter, the implications for stock values will be negative. For now, equity markets seem to be maintaining the more hopeful view that growth will eventually return to a better footing. As a result of trends in the data, expressed in the WCA Barometer, tactical equity exposure remains slightly elevated relative to benchmark exposure, and was increased modestly again this month in keeping with our near-term forecast path for the barometer (above).

Kevin Caron, CFA, Senior Portfolio Manager

Chad Morganlander, Senior Portfolio Manager

Matthew Battipaglia, Portfolio Manager

Steve Lerit, CFA, Client Portfolio Manager

Suzanne Ashley, Analyst

(973) 549-4168

www.washingtoncrossingadvisors.com

www.stifel.com

Disclosures

WCA Fundamental Conditions Barometer Description: We regularly assess changes in fundamental conditions to help guide near-term asset allocation decisions. The analysis incorporates approximately 30 forward-looking indicators in categories ranging from Credit and Capital Markets to U.S. Economic Conditions and Foreign Conditions. From each category of data, we create three diffusion-style sub-indices that measure the trends in the underlying data. Sustained improvement that is spread across a wide variety of observations will produce index readings above 50 (potentially favoring stocks), while readings below 50 would indicate potential deterioration (potentially favoring bonds). The WCA Fundamental Conditions Index combines the three underlying categories into a single summary measure. This measure can be thought of as a “barometer” for changes in fundamental conditions.

The information contained herein has been prepared from sources believed to be reliable but is not guaranteed by us and is not a complete summary or statement of all available data, nor is it considered an offer to buy or sell any securities referred to herein. Opinions expressed are subject to change without notice and do not take into account the particular investment objectives, financial situation, or needs of individual investors. There is no guarantee that the figures or opinions forecasted in this report will be realized or achieved. Employees of Stifel, Nicolaus & Company, Incorporated or its affiliates may, at times, release written or oral commentary, technical analysis, or trading strategies that differ from the opinions expressed within. Past performance is no guarantee of future results. Indices are unmanaged, and you cannot invest directly in an index.

Asset allocation and diversification do not ensure a profit and may not protect against loss. There are special considerations associated with international investing, including the risk of currency fluctuations and political and economic events. Investing in emerging markets may involve greater risk and volatility than investing in more developed countries. Due to their narrow focus, sector-based investments typically exhibit greater volatility. Small company stocks are typically more volatile and carry additional risks, since smaller companies generally are not as well established as larger companies. Property values can fall due to environmental, economic, or other reasons, and changes in interest rates can negatively impact the performance of real estate companies. When investing in bonds, it is important to note that as interest rates rise, bond prices will fall. High-yield bonds have greater credit risk than higher-quality bonds. The risk of loss in trading commodities and futures can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. The high degree of leverage that is often obtainable in commodity trading can work against you as well as for you. The use of leverage can lead to large losses as well as gains.

All investments involve risk, including loss of principal, and there is no guarantee that investment objectives will be met. It is important to review your investment objectives, risk tolerance and liquidity needs before choosing an investment style or manager. Equity investments are subject generally to market, market sector, market liquidity, issuer, and investment style risks, among other factors to varying degrees. Fixed Income investments are subject to market, market liquidity, issuer, investment style, interest rate, credit quality, and call risks, among other factors to varying degrees.

This commentary often expresses opinions about the direction of market, investment sector and other trends. The opinions should not be considered predictions of future results. The information contained in this report is based on sources believed to be reliable, but is not guaranteed and not necessarily complete.

Washington Crossing Advisors LLC is a wholly owned subsidiary and affiliated SEC Registered Investment Adviser of Stifel Financial Corp (NYSE: SF).