Investing In The Age of Rising Rates

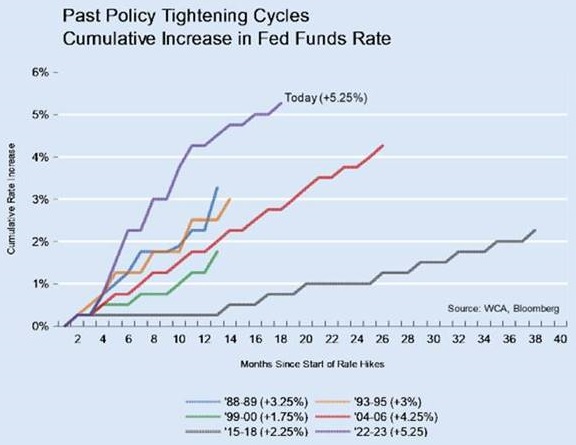

As 2023 comes to a close and investors look back over the past two years, one can’t ignore the paradigm shift in rising interest rates and its far-reaching effects on markets and the economy. After all, investment portfolios, mortgages, savings accounts, and auto loans, to name a few, have been drastically impacted by rising interest rates, which stand at 5.25% today. To put it into perspective, we have not seen a Fed Funds Rate this high, achieved in such a short period, in over 35 years (see Chart A). Against a backdrop of high rates, risk, and recession uncertainty, it seems prudent to revisit how we got here and how Washington Crossing Advisors considers these challenges when choosing investments in our equity portfolios.

Chart A

The Seeds of Inflation

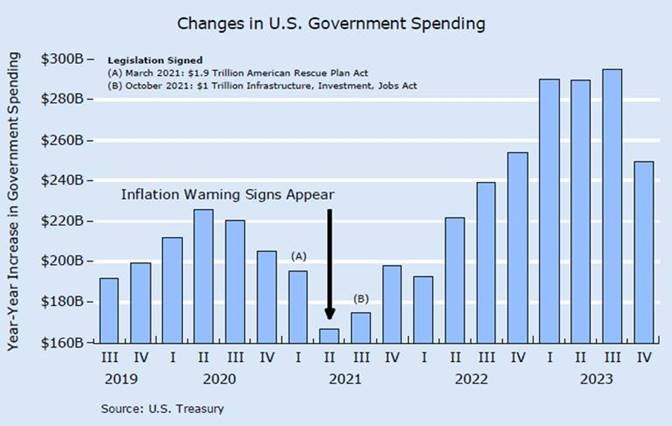

Nearly four years ago, Americans learned about the COVID-19 pandemic. Looking beyond the tragic loss of life, the U.S. government had to quickly intervene to keep the economy functioning and provide relief for millions of Americans who suddenly lost their jobs. The Paycheck Protection Program and other financial assistance programs took effect later in 2020 and beyond. More recently, two significant pieces of legislation were signed into law in 2021 that would drastically increase government spending in subsequent years. The timeline and impact on government spending for the $1.9 trillion American Rescue Plan Act and $1 trillion Infrastructure, Investment, and Jobs Act are depicted in Chart B. It was also around this time that inflation warning signs first appeared in the spring/summer of 2021.

Chart B

As fiscal policy became more expansionary, monetary policy remained extremely accommodative, and the Fed Funds Rate hovered near 0%. With both fiscal and monetary policies firmly on the accelerator, inflation followed, which we warned about in a May 2021 market commentary piece titled “A Discussion Worth Having.” In particular, Chart C below examined expected inflation and rates expectations. Essentially, the Treasury TIPS market (green line) expected 4+% inflation into 2022, followed by a slight moderation, but still ahead of the Federal Reserve’s (Fed) stated 2% target. The forwards rate markets (orange line), looking at short-term rates, and Federal Reserve forecasts (blue line), both expected near-zero policy rates for several more years. As it would turn out, the Federal Reserve and forwards markets significantly underestimated the historic rise in rates we’ve lived through the past two years.

Chart C

Where’s the Recession?

After brutal declines in equity and bond prices in 2022, many forecasters expected 2023 to be a most challenging year. For example, in a Bloomberg Survey of Professional Investors in December 2022, 60% of those surveyed predicted a recession in 2023. Another firm forecasted “the worst downturn in decades.” As of 10 November 2023, this feared downturn has yet to materialize. The job market remains solid, disinflationary trends persist, and corporate earnings indicate a resilient consumer. Indeed, credit spreads and the equity risk premium are both at 20-year low levels, meaning a “risk on” sentiment that flies in the face of a recessionary environment (Chart D).

Chart D

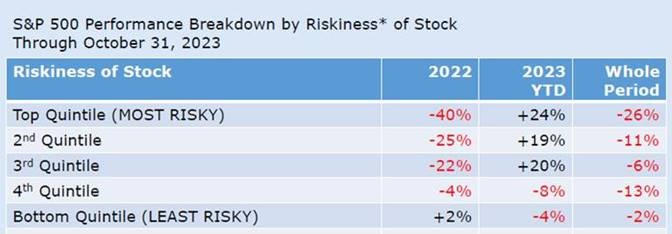

Having dodged an imminent recession this year, risky stocks have been the best-performing equities, as measured by their beta, underscoring the above attitudes favoring risk. However, looking at the whole rising rate period tells a very different story. Table A below shows how less risky stocks have outperformed riskier stocks as interest rates unexpectedly soared.

Table A

Conclusion

We believe basing investing decisions on interest rate predictions or recession probabilities is a fool’s errand. Events of the past two years, as discussed above, prove that it is tough to correctly estimate or model the path of interest rates and understand when or if a recession will ever materialize. Instead, at Washington Crossing Advisors, we construct our equity portfolios with high-quality companies that have had low debt levels, profitable assets, and consistent earnings. Additionally, our strategies maintain lower betas (risk) than the broader averages. Focusing on high-quality, lower-risk stocks helped insulate portfolios from outsized risk since interest rates started a historic rise early in 2022.