Debt Negotiations and Uncertainty: Importance of Quality Focus

Like it or not, debt negotiations and shutdowns are integral to the political process, recurring over the past 50 years. The fear of a budget impasse, shutdown, default, and debt downgrade has again gripped the markets. However, it is unlikely that lawmakers will allow a debt default, following instead a familiar pattern of bipartisan argument, brinksmanship, and, finally, compromise.

While an outright U.S. government debt default is improbable, we should emphasize quality due to its numerous benefits. Durable, flexible, and predictable firms tend to fare better in uncertain times. In contrast, financially weak firms are more susceptible to government default or downgrade.

Default Unlikely

Defaulting on U.S. Treasury debt, leading to a downgrade, would raise the cost of government funding and impact various entities. The concept of Treasury bonds as “risk-free” would be challenged, causing rating agencies to downgrade U.S. debt ratings and increase interest rates. This would harm borrowers, dent asset values, and weaken confidence. The consequences of a disorderly default on U.S. debt would be far-reaching, affecting both sides of the political divide.

It is more probable that a compromise or a deal will be reached before the X-date, when the Treasury exhausts its funding ability, or after a period of discretionary federal spending shutdown. However, a prolonged impasse would almost certainly increase market volatility, raising funding costs for entities, especially those closely tied to the government or with weak financials. Thus, limiting the scope of any potential default is incentivized to avoid missed interest payments and resolve the situation promptly.

Although a U.S. government default is unlikely, focusing on quality remains crucial. The central idea behind the “quality” theme is understanding and managing risk effectively. Risk is inherent in investing and can present opportunities, but not all risks are adequately rewarded. Global debt, disruptive technologies, and political instability exemplify such risks.

Redouble Focus on “Quality”

While risks cannot be entirely avoided, minimizing exposure to unrewarded and unexpected risks is essential. Even holding cash carries dangers like theft or inflation eroding purchasing power. A U.S. debt default would almost certainly qualify as a situation where unrewarded and unexpected risk would surface. Even a protracted battle that rattles markets, but where an outright default is ultimately avoided, could take a toll on confidence. Pivotal players in this process are rating agencies and their reaction to a perceived threat of default. So, it is important what rating agencies think about the prospects of default.

Moody’s Investors Service is one such agency and they recently issued a report on the U.S. debt-limit standoff. The report concludes, not surprisingly, that financially weak firms are most vulnerable to a government default or downgrade1:

“Lowest-rated issuers are most vulnerable to heightened market uncertainty between now and the X-date.”

Moody’s Investors Service, 4 May 2023

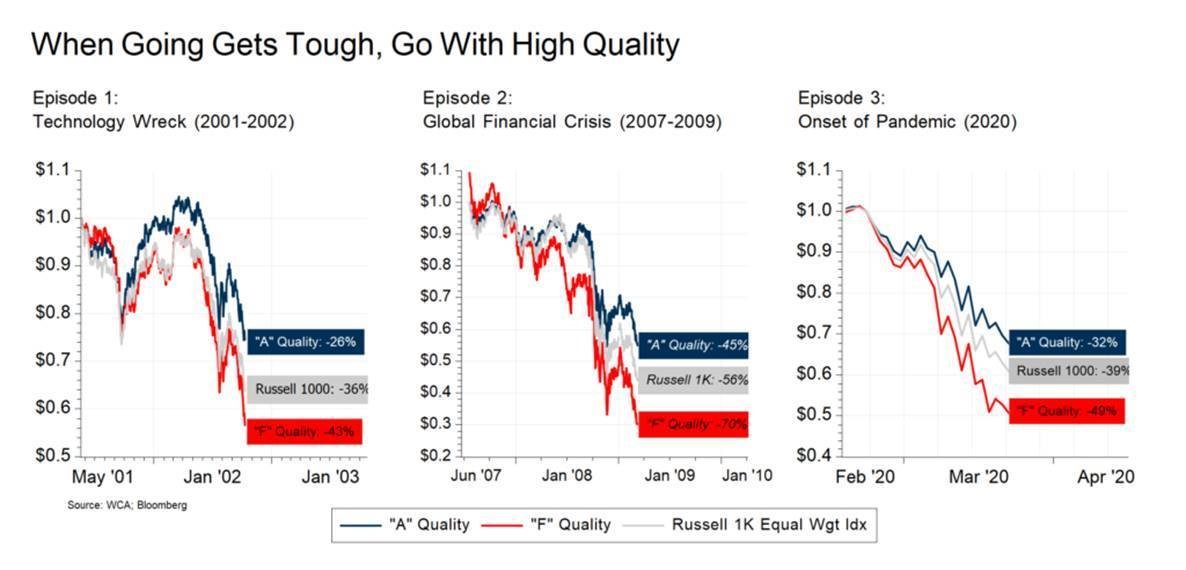

We agree with this assessment but take our own approach to defining quality. The 2008 financial crisis showcased the limitations of rating agencies’ debt ratings when venerable firms with high investment-grade ratings collapsed. We conducted our own fundamental analysis, therefore, to evaluate companies based on asset profitability, indebtedness, and consistency, assigning them to different quality groups (“A” and “F” Quality). Notice in the chart below, that financially strong, high-quality stocks (“A” Quality) held up better under stress than low-quality ones (“F” Quality).

A strong correlation exists between fundamental quality and stock price performance during turbulent times. Investors tend to favor high-quality assets in times of uncertainty or economic downturns. Therefore, prioritizing quality is paramount in assessing risk for equity investing, followed by growth, valuation, and yield considerations.

In conclusion, while an outright U.S. government default is unlikely, focusing on quality is crucial for two reasons. First, investors seek durability, flexibility, and predictability (i.e., “quality”) in uncertain times. Second, financially weak firms are most vulnerable to a potential government default or downgrade.

Despite the messiness of debt negotiations, the process nonetheless does prompt needed public discussion, ensuring government accountability to the people it serves.

1Scenario analysis: US debt-limit standoff elevates credit risk for various debt issuers, Moody’s Investors Service