Closing Overweight Tactical Tilt

As inflation worries mount, signs of stress are emerging. For example in our monthly update of the WCA Fundamental Conditions Barometer, we see a return to a neutral reading. As Chart A below shows, this is the first time since spring of 2020 our forecast path is down to 50 — a neutral level. In light of this fact, we reduce our tactical tilt toward equity to neutral from overweight versus our policy equity target.

Chart A

WCA “Barometer”

Emerging Signs of Stress

Despite positives such as strong corporate earnings, a booming housing market, and pandemic-era lows in weekly unemployment claims, signs of stress are emerging.

United States

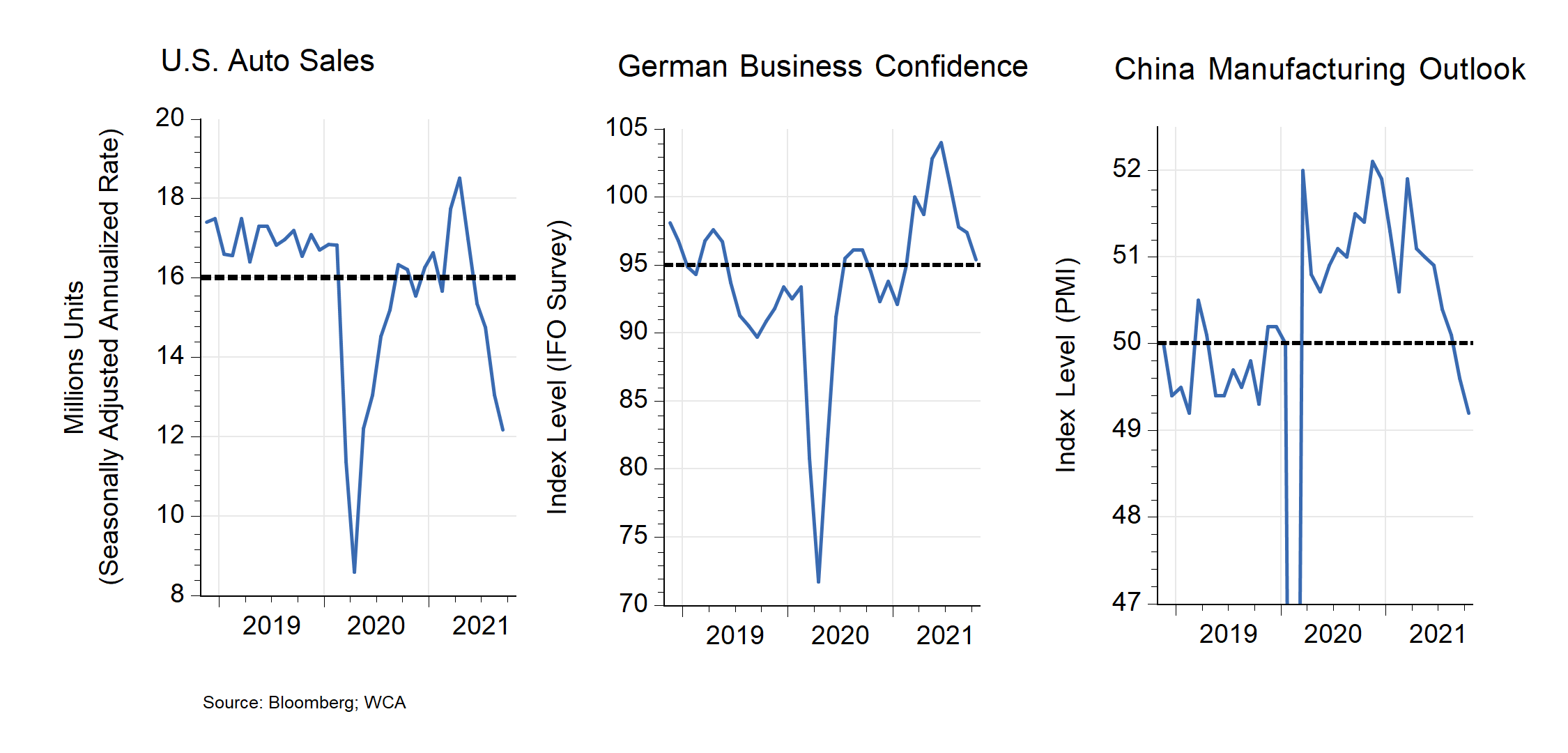

After record-shattering stimulus measures in 2020-2021, supply now fails to keep up with demand in the United States. Consider that automobile sales are expected to fall to about 12 million annualized units sold this month (Chart B, below-left). This is a significant decline, more consistent with recessions. Dealers are short of sellable inventory, given critical parts shortages at car manufacturers.

Economic growth is being hurt by these kinds of disruptions. Advance estimates of third-quarter U.S. economic growth are near 2%. This contrasts sharply with earlier forecasts which had the economy growing near 6% as recently as August. Higher fuel prices at airlines, parts shortages at manufacturers, and widespread labor shortages have suddenly begun to bite hard into growth.

Europe

Stress is apparent in Europe as well. Manufacturing-heavy Germany, for example, is also feeling the pinch of disrupted global supply chains. Last week’s German business confidence survey for October conducted by the Munich-based Ifo Institute showed a fourth consecutive monthly decline (Chart B, below-center). Slack is building for German factories, a negative sign for Euro-Area growth in the months ahead.

China

New COVID-19 restrictions, fuel shortages, and a shaky property sector are cutting into Chinese growth, too. This is now clearly seen in the outlook for Chinese manufacturers, where the Chinese Purchasing Manager’s Index has fallen for seven straight months (Chart B, below-right). Hopes for a fast post-pandemic rebound are now all but gone. Given China’s position as a global manufacturing powerhouse, continued weakness in the manufacturing outlook is also a negative for near-term global growth prospects.

Chart B

Emerging Signs of Global Stress

“Animal Spirits” Soar Weaker Signs

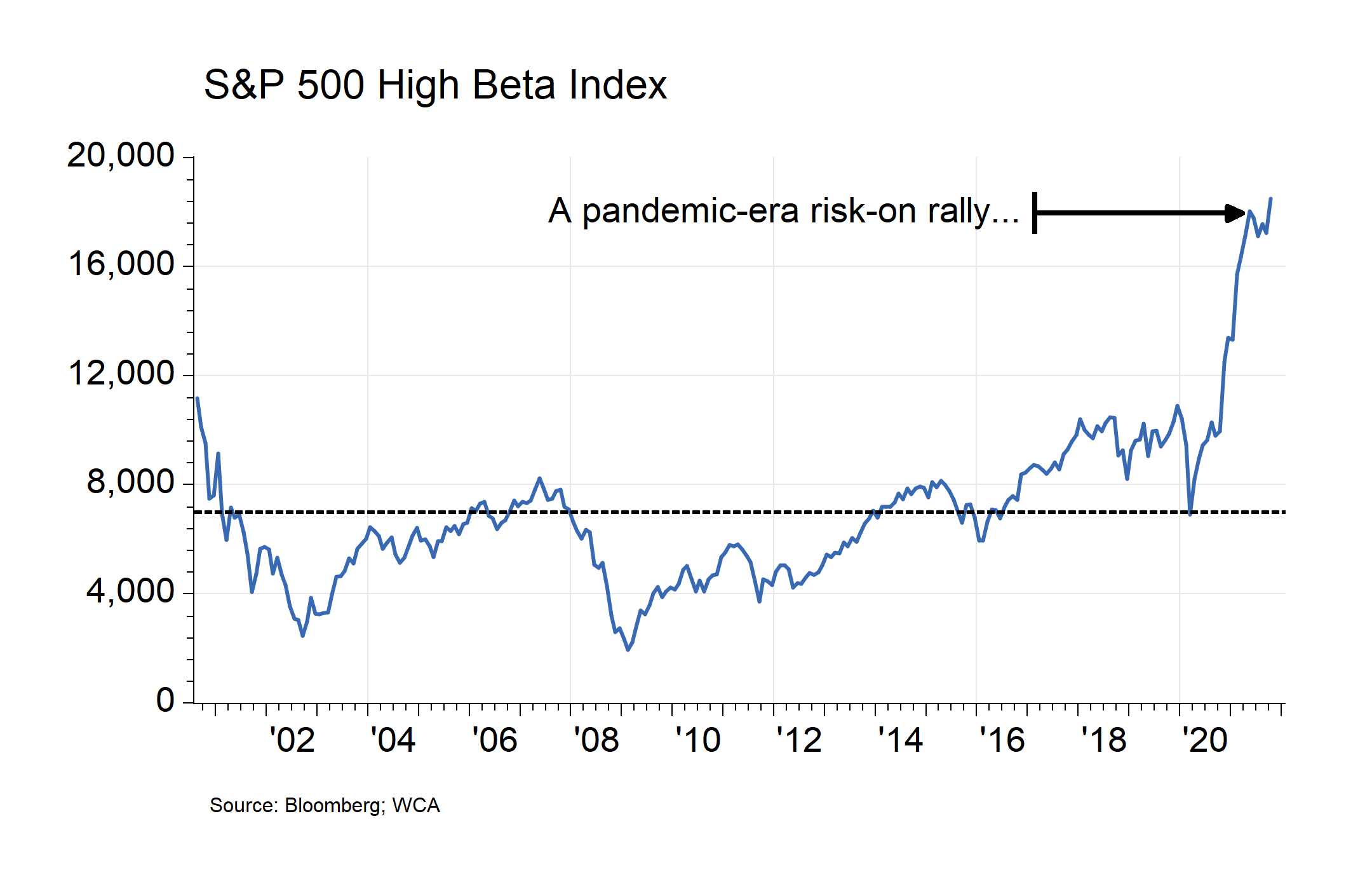

Despite these signs of stress, U.S. asset values are priced to reflect strong growth. We see signs of enthusiasm in both the stock and bond markets. Consider the low-quality stock rally of the past year, for example. The United States stock market value is now approaching $54 trillion, up $20 trillion from just before the start of the pandemic. What’s more, the rally of the past several months has been led by the highest risk, highest “beta” stocks (Chart C, below). Notice the surge in interest in the riskiest stocks represented by the S&P High Beta index (the index tracks higher than average risk stocks). In our view, this reflects soaring “animal spirits” nurtured by stimulus and hopeful of powerful growth post-pandemic.

Chart C

U.S. Stocks Rally, Led by Highest-Risk Companies

Similar risk-loving behavior can be seen in the corporate bond market. The spread between corporate bonds and U.S. Treasuries, which can serve as a proxy for market expectations about corporate health, is near cycle lows (Chart D, below). Over $11 trillion in total corporate debt, surging junk bond issuance, and massive bank debt deals have done nothing to cause investors to worry here. Here is a snapshot of some of the recent developments in the corporate bond market.

Chart D

Corporate Bond Investors Not Yet Worried

Recent Debt Issuance Trends

As Reported by The Wall Street Journal

Corporate Debt: Nonfinancial companies issued $1.7 trillion of bonds in the U.S. last year, nearly $600 billion more than the previous high, according to Dealogic. According to the Federal Reserve, their total debt stood at $11.2 trillion, about half the size of the U.S. economy.

Junk Bonds: In the junk-bond market alone, U.S. companies have issued more than $361 billion of bonds with speculative-grade credit ratings through Sept. 14, according to S&P Global Market Intelligence’s LCD. That is the second-most junk bonds ever sold in a single year and on pace to surpass 2020’s $435 billion record.

Banks: The six largest U.S. banks have issued some $314 billion of bonds this year, already the most for any year since 2008, according to Dealogic.

Conclusion

We now close out a long period of overweighting stocks versus bonds on a tactical basis. While the economy remains on a growth path, signs are emerging that growth is slowing. However, markets continue to be priced in anticipation of faster growth.

Under these circumstances, we believe a more neutral tactical posture and focus on higher-quality issues seems to make sense at this point.

Kevin R. Caron, CFA

Senior Portfolio Manager

973-549-4051

Chad Morganlander

Senior Portfolio Manager

973-549-4052

Matthew Battipaglia

Portfolio Manager

973-549-4047

Steve Lerit, CFA

Senior Risk Manager

973-549-4028

Tom Serzan

Analyst

973-549-4335

Suzanne Ashley

Internal Relationship Manager

973-549-4168

Eric Needham

Director, External Sales and Marketing

312-771-6010

Jeffrey Battipaglia

Client Portfolio Manager

973-549-4031

Disclosures

The information contained herein has been prepared from sources believed to be reliable but is not guaranteed by us and is not a complete summary or statement of all available data, nor is it considered an offer to buy or sell any securities referred to herein. Opinions expressed are subject to change without notice and do not take into account the particular investment objectives, financial situation, or needs of individual investors. There is no guarantee that the figures or opinions forecast in this report will be realized or achieved. Employees of Stifel, Nicolaus & Company, Incorporated or its affiliates may, at times, release written or oral commentary, technical analysis, or trading strategies that differ from the opinions expressed within. Past performance is no guarantee of future results. Indices are unmanaged, and you cannot invest directly in an index.

Asset allocation and diversification do not ensure a profit and may not protect against loss. There are special considerations associated with international investing, including the risk of currency fluctuations and political and economic events. Changes in market conditions or a company’s financial condition may impact a company’s ability to continue to pay dividends, and companies may also choose to discontinue dividend payments. Investing in emerging markets may involve greater risk and volatility than investing in more developed countries. Due to their narrow focus, sector-based investments typically exhibit greater volatility. Small-company stocks are typically more volatile and carry additional risks since smaller companies generally are not as well established as larger companies. Property values can fall due to environmental, economic, or other reasons, and changes in interest rates can negatively impact the performance of real estate companies. When investing in bonds, it is important to note that as interest rates rise, bond prices will fall. High-yield bonds have greater credit risk than higher-quality bonds. Bond laddering does not assure a profit or protect against loss in a declining market. The risk of loss in trading commodities and futures can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. The high degree of leverage that is often obtainable in commodity trading can work against you as well as for you. The use of leverage can lead to large losses as well as gains. Changes in market conditions or a company’s financial condition may impact a company’s ability to continue to pay dividends, and companies may also choose to discontinue dividend payments.

All investments involve risk, including loss of principal, and there is no guarantee that investment objectives will be met. It is important to review your investment objectives, risk tolerance, and liquidity needs before choosing an investment style or manager. Equity investments are subject generally to market, market sector, market liquidity, issuer, and investment style risks, among other factors to varying degrees. Fixed Income investments are subject to market, market liquidity, issuer, investment style, interest rate, credit quality, and call risks, among other factors to varying degrees.

This commentary often expresses opinions about the direction of market, investment sector, and other trends. The opinions should not be considered predictions of future results. The information contained in this report is based on sources believed to be reliable, but is not guaranteed and not necessarily complete.

The securities discussed in this material were selected due to recent changes in the strategies. This selection criterion is not based on any measurement of performance of the underlying security.

Washington Crossing Advisors, LLC is a wholly-owned subsidiary and affiliated SEC Registered Investment Adviser of Stifel Financial Corp (NYSE: SF). Registration with the SEC implies no level of sophistication in investment management.

WCA Fundamental Conditions Barometer:

We regularly assess changes in fundamental conditions to help guide near-term asset allocation decisions. The analysis incorporates approximately 30 forward-looking indicators in categories ranging from Credit and Capital Markets to U.S. Economic Conditions and Foreign Conditions. From each category of data, we create three diffusion-style sub-indices that measure the trends in the underlying data. Sustained improvement that is spread across a wide variety of observations will produce index readings above 50 (potentially favoring stocks), while readings below 50 would indicate potential deterioration (potentially favoring bonds). The WCA Fundamental Conditions Index combines the three underlying categories into a single summary measure. This measure can be thought of as a “barometer” for changes in fundamental conditions.

Disclosures

The information contained herein has been prepared from sources believed to be reliable but is not guaranteed by us and is not a complete summary or statement of all available data, nor is it considered an offer to buy or sell any securities referred to herein. Opinions expressed are subject to change without notice and do not take into account the particular investment objectives, financial situation, or needs of individual investors. There is no guarantee that the figures or opinions forecast in this report will be realized or achieved. Employees of Stifel, Nicolaus & Company, Incorporated or its affiliates may, at times, release written or oral commentary, technical analysis, or trading strategies that differ from the opinions expressed within. Past performance is no guarantee of future results. Indices are unmanaged, and you cannot invest directly in an index.

Asset allocation and diversification do not ensure a profit and may not protect against loss. There are special considerations associated with international investing, including the risk of currency fluctuations and political and economic events. Changes in market conditions or a company’s financial condition may impact a company’s ability to continue to pay dividends, and companies may also choose to discontinue dividend payments. Investing in emerging markets may involve greater risk and volatility than investing in more developed countries. Due to their narrow focus, sector-based investments typically exhibit greater volatility. Small-company stocks are typically more volatile and carry additional risks since smaller companies generally are not as well established as larger companies. Property values can fall due to environmental, economic, or other reasons, and changes in interest rates can negatively impact the performance of real estate companies. When investing in bonds, it is important to note that as interest rates rise, bond prices will fall. High-yield bonds have greater credit risk than higher-quality bonds. Bond laddering does not assure a profit or protect against loss in a declining market. The risk of loss in trading commodities and futures can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. The high degree of leverage that is often obtainable in commodity trading can work against you as well as for you. The use of leverage can lead to large losses as well as gains. Changes in market conditions or a company’s financial condition may impact a company’s ability to continue to pay dividends, and companies may also choose to discontinue dividend payments.

All investments involve risk, including loss of principal, and there is no guarantee that investment objectives will be met. It is important to review your investment objectives, risk tolerance, and liquidity needs before choosing an investment style or manager. Equity investments are subject generally to market, market sector, market liquidity, issuer, and investment style risks, among other factors to varying degrees. Fixed Income investments are subject to market, market liquidity, issuer, investment style, interest rate, credit quality, and call risks, among other factors to varying degrees.

This commentary often expresses opinions about the direction of market, investment sector, and other trends. The opinions should not be considered predictions of future results. The information contained in this report is based on sources believed to be reliable, but is not guaranteed and not necessarily complete.

The securities discussed in this material were selected due to recent changes in the strategies. This selection criterion is not based on any measurement of performance of the underlying security.

Washington Crossing Advisors, LLC is a wholly-owned subsidiary and affiliated SEC Registered Investment Adviser of Stifel Financial Corp (NYSE: SF). Registration with the SEC implies no level of sophistication in investment management.