Quality and Certainty

The only sure thing in investing is the uncertain.

When we began the year, bearishness was rampant. Most Wall Street forecasters were expecting a recession, and the International Monetary Fund (IMF) warned the “worst is yet to come.” Thus far, the dismal outlook of these forecasters has yet to materialize. The lesson is that accurate and precise forecasts are rare. So how do we deal with uncertainty? We plan for the unexpected by continually focusing on quality. Fixing the roof when the sun is shining is far easier than when it rains!

The S&P 500 is up 18% year-to-date, with earnings forecasts primarily unchanged. Growth expectations and interest rates are flat compared to the year’s start. So, a big reason stocks are up for the year is likely an increase in risk appetite, expressed as a rise in multiples. The S&P 500’s price-earnings-multiple is up to 19.7x from 16.8x, or 17.3%, through the time of this writing.

We are pleased that the economy has fared well thus far this year. Yet, we are mindful that we have experienced roughly 5 bear markets in the past 20 years. Those markets brought declines of 20% to over 50%. Accordingly, thinking as much about having a solid defense is just as important as generating a return.

Quality vs Risk

Consider the riskiness of two stocks. One is the stock of an unprofitable, debt-ridden, unpredictable business. The other is that of a profitable, debt-free, steady business. The former is a low-quality stock, and the latter a high-quality one. We would expect the high-quality business to be less risky. By contrast, lower-quality companies ought to have higher risk. Based on our research, stock movements usually reflect the business’s fundamental nature. Consequently, it pays to focus on business fundamentals when considering portfolio risk.

Quality and Yield

If you want to reduce volatility and uncertainty, it makes sense to quantify what is meant by “quality.” Here, we use our WCA Quality grading system to illustrate the concept. To do this, we grade companies from “A” to “F” based on three questions:

• First: To what extent does debt play a role in the company’s capital structure? Where debt occupies a significant position, grades are lower, and vice-versa.

• Second: How profitable are the company’s assets? Comparing profit to assets gives us a high-level understanding of profitability.

• Third: Does the business generate profit dependably and predictably? This is critical for forecasting and surviving tough times.

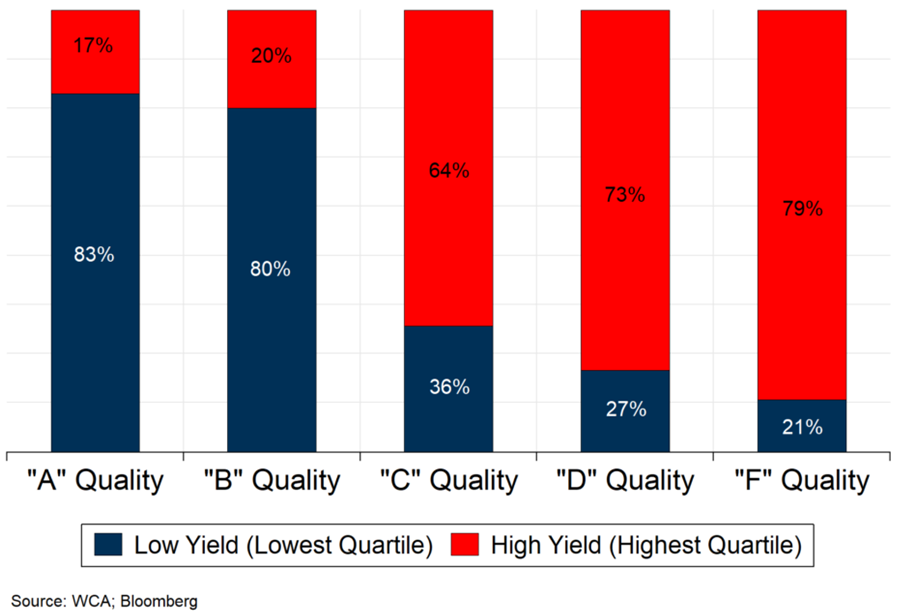

Notice what is missing. We are not looking for companies with high dividend yields. Instead, we focus on factors that contribute to growth, profitability, cash flow, and survival. In fact, over-emphasizing yield can lead directly to low quality and high risk. We offer Chart A below to show what happens to quality as yield increases.

What do we notice? It is clear that as we move from low to high current dividend yield, the quality of companies generally declines. There is a clear tendency for higher yield to equate to lower quality. Next, we will show how lower quality translates into higher risk and uncertainty. Be careful about “reaching” for yield.

Chart A: High Dividend Yield Tends to Be Low Quality

Risk and Quality

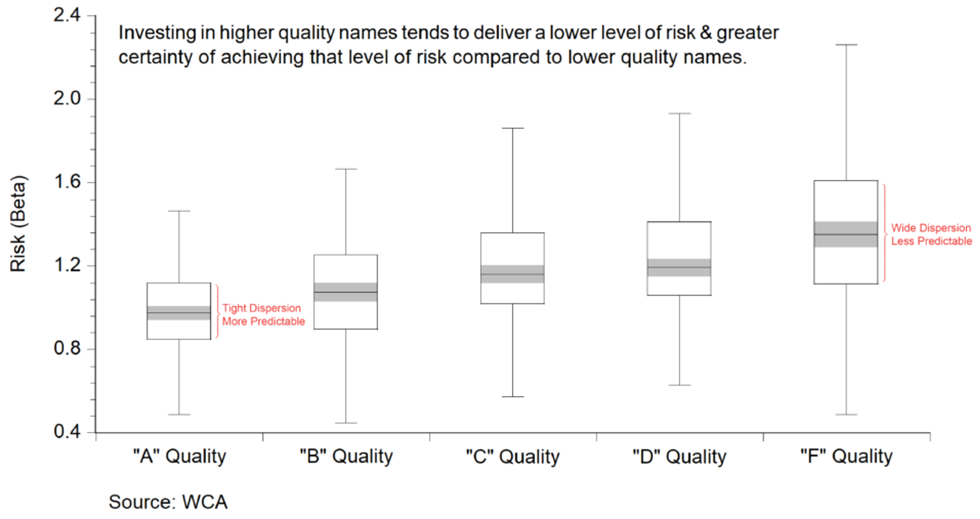

As we move from high to low quality, risk relative to the market also increases. The Chart below shows the range of risk, measured as beta (a market-relative risk measure). Notice two things about the graph. There is a tendency for “A” quality (high quality) stocks to not only have lower relative risk (beta), but the dispersion among “A” stocks is tighter than “F.” This means that stock picking becomes much trickier, with much less certainty of success, when picking low-quality, “F” stocks. By contrast, higher quality “A” stocks offer lower overall volatility with far more consistent risk characteristics from one high-quality stock to another. Lower quality tends to offer wildly divergent levels of risk (beta).

Chart B: Risk Rises and Becomes Less Predictable as Quality Declines

Conclusion

Hopefully, we have made the case that a high-quality focus should come before other considerations, especially yield. Companies build value by staying in business, generating cash, and reinvesting for growth. Buying those same companies at reasonable prices is a good place to start for building a solid portfolio.

So as we start the back half of the year with most forecasters feeling better about the outlook, we remain on guard. Given the inherent uncertain world in which we live, we should remain committed to quality as a deterrent against excessive risk.