The Case for Laddering Bonds

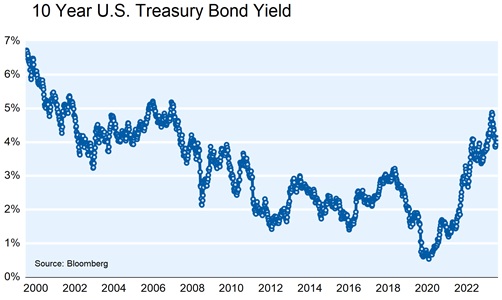

After an extended period of historically low interest rates, income-focused bond investors have finally found relief as interest rates have risen to levels not seen since late 2007 (see Chart A below).

Chart A

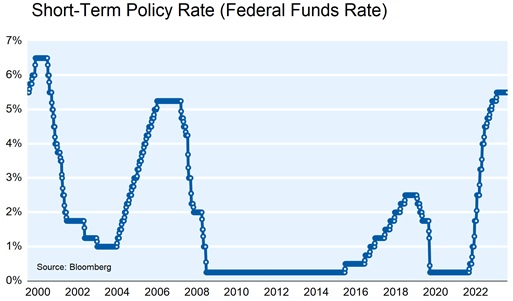

Time to declare victory, right? If only it were that simple. There are external forces that influence the bond market, none more so than the Federal Reserve (Fed). Who knows what the Fed will do and when? Could they start cutting interest rates this year after two years spent increasing them? Chart B below shows the twenty-year history of the Fed Funds Target Rate.

Chart B

Nobody knows for sure what will happen to interest rates in the future. There are potential ranges of plausible outcomes, but in reality, the future direction of interest rates is unknowable. What is knowable is today’s level of interest rates. So, an investor interested in knowing the nominal dollar return of a T-bill or zero-coupon U.S. Treasury can know that future return with certainty today. This is not true for stocks and other fixed-income assets.

Is there a way for bond investors to “win” if interest rates fall? What if they continue to move higher? We think laddering bonds is one way to navigate an uncertain and changing environment.

Building a Ladder

One way of mitigating risk no matter the interest rate environment would be to invest in individual bonds with staggered maturities. The proceeds from maturing bonds are systematically reinvested at the prevailing rate of interest as time passes and bonds mature. This simple strategy is called a bond ladder. It is a strategy that allows ownership of securities that delivers higher yields than money market funds and short-term bonds, while still keeping pace with interest rates. The average income would be lower than owning all long-term bonds, but the risk would be reduced and flexibility increased.

In a 10-year ladder, bonds are staggered across maturities one to ten years. A simple ten-year ladder would have 10% of the portfolio value invested in one-year bonds, 10% invested in two-year bonds, and so on out to year ten. At the beginning of the second year, when the initial one-year bonds mature, the cash proceeds are reinvested into a new ten-year bond. This process can continue indefinitely and the average portfolio yield will adjust as new bonds are introduced into the portfolio gradually over time.

This is a simple and straightforward strategy that is designed to:

• Generate a consistent stream of income;

• Lower risk compared to fixed investment in long-dated bonds;

• Reduce turnover;

• Help manage risk; and

• Adjust to a changing interest rate environment over time

Stable Principal and Income

While the market value of the ladder will fluctuate with the interest rate environment, the principal value of the portfolio will not be affected (provided bonds are held to maturity and the issuer does not default). The principal value, along with the income stream received, is not changed by fluctuating interest rates. If held to maturity, paper gains and losses are never realized, and the income stream remains predictable.

Know Your Risk and Retire From the Forecasting Game

Some bond strategies require making frequent changes to holdings in pursuit of return. In contrast, a laddering strategy makes no attempt to time the bond market. Instead, the portfolio always maintains a relatively fixed average maturity. In the case of a ten-year ladder, the average maturity is approximately 5.5 years. Since average maturity is linked closely to interest rate risk, having a stable average maturity makes it easier to know how much risk is in the portfolio at any point in time.

In exchange for this greater risk clarity, the potential for higher returns from successfully timing turns in the interest rate cycle are foregone. While there have been some successful managers in the past, those investors who can consistently time interest rate changes are the exception rather than the rule.

Instead of basing an investment program on attempting to time the interest rate cycle, laddering offers a simple way of investing in bonds across a variety of interest rate cycles.

Options for Higher Yield

Of course a ladder need not be constructed out of Treasury bonds. Corporate bonds, municipal bonds, and foreign bonds each offer differing levels of after-tax return above Treasuries. They also carry different levels of default risk. While corporate bonds have higher risk of default than the U.S. government, investment grade bonds almost always offer higher yields than U.S. Treasuries. Since the beginning of 1997 through January of this year, long-term AA rated investment grade bonds have generally yielded about 1.0% more than U.S. Treasuries. (Source: Ice Data Indices, LLC).

Conclusion

We believe that bond investors should educate themselves about options to invest in an uncertain environment. We think bond laddering is a sensible and practical way to invest the fixed income part of a balanced portfolio given uncertainties that lie ahead.