Signs of Improvement

Broadening Out Portfolios & Raising Equity

Exposure

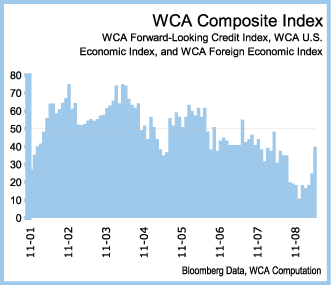

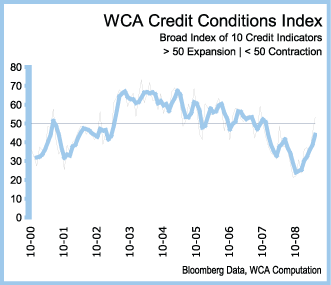

Since our last commentary, we have seen signs of improvement

in a variety of economic indicators (see WCA Economic

Conditions Index), above and beyond the improvement already

seen in the supply indicators of credit (see WCA Credit

Conditions Index). In no particular order, we have seen:

1. a rise in some commodity prices;

2. an improvement in confidence;

3. a slowdown in jobless claims;

4. stabilization in the inventory-to-sales ratio; and

5. signs of increased overseas activity.

.png)

It is difficult to see whether these "green shoots" will grow

deeper roots, or die from the economy's chill in the months

ahead. Despite these improvements, we are aware of the

complexities brought about by over-indebtedness, de-leveraging,

monetization of massive amounts of new Federal debt, and high

levels of government involvement in private sector business.

These all introduce new levels of uncertainty into the investing

equation that cannot be easily understood or anticipated. That

said, we must recognize the good with the bad, and investment

decisions must take all relevant facts into account.

Therefore, we have decided to increase our exposure to equities

(both foreign and domestic) primarily within the growth

categories (technology, consumer discretionary, healthcare)

which are performing better and tend to be less levered than

most value sectors. We also add corporate debt (both high grade

and high yield), and add foreign government bonds (both

developed and emerging market). We are utilizing some of our

cash, Treasury bills, Treasury bonds, and gold positions as

sources of funds to make these investments. As the result of

these changes, our tactical portfolio recommendations will have

a higher equity position, but remain below the midpoint of our

target ranges for equity exposure pending further developments.

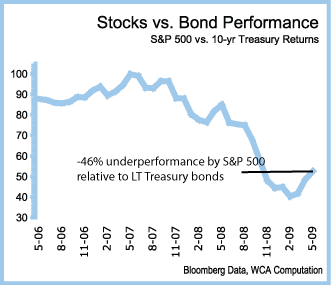

Before the market lows of March, risk investment in equities had

underperformed full "faith and credit" U.S. Treasury bonds by

63% from July 2007. The equity market's recent

improvement from the March lows, coupled with a backing up of

long-term interest rates, narrows this margin of

underperformance to 46% (see chart). By either measure,

this large re-pricing of risk has been consistent with the

enormity of the challenges that have confronted, and will

continue to confront, the economy. Nonetheless, such a

correction ranks among the largest re-pricings of risk seen in

U.S. financial history.

In this corrective process, the equity risk premium has

risen sharply. This can be seen when comparing the

trailing 12-month S&P 500 "earnings yield" (or inverse of the

price-to-earnings ratio) to the yield offered on 10-year U.S.

Government Treasury Bonds. At present, this difference (called

a spread) is 2% higher (200 basis points) for the equity "yield"

than the yield offered on the Treasury (see chart). This level

has not been seen since 1980, and while it can go higher (as was

the case in the 1970s), the purchase of S&P 500 earnings is

today more attractive than the purchase of long-term Treasuries

based on a comparison of current yields. However, the important

question is, “What kind of recovery can we expect in S&P 500

earnings in a post credit bubble environment?”

.png)

We expect to see a slow earnings recovery

starting in 2010-2011. We now expect $51

in 2009 S&P operating earnings; $54 in 2010 earnings (5%

growth); $65

in 2011

operating earnings in 2011 (22% growth); and $84 in 2012 (24% growth).

Using the current S&P 500 index level of approximately 950, we

estimate that the U.S. equity market now trades at 18.5X 2009

earnings, with earnings expected to grow at 15% over the next

four years. A link to a spreadsheet containing our full set of

assumptions can be found

here.

Our assumptions underlying our forecast are:

1) The most severe part of the recession is behind us;

that 2010 will begin a transition toward gradual recovery; and

by 2011, the economy will be well beyond the current period of

negative growth. We place the odds of recession lingering

through 2010 at less than 50% and have no expectation for

recession to continue beyond 2010.

2) A slow process of recovery in employment, output, and

profits will emerge from the initial early signs of

recovery that we have identified in our economic and credit

analysis (as discussed above). This recovery will be typified

by higher unemployment and lower profitability than earlier

cycles because:

1.

the percentage of employment in government and socialized fields

will most likely continue to expand relative to private sector

employment;

2.

the capacity for expansion of private sector debt and credit are

fading;

3.

demographic shifts in the age of the population are underway;

and

4.

highly cyclical sectors such as manufacturing continue to shrink

from cycle to cycle.

Hence, the level of “full employment” in recovery may well be

less than in previous cycles, and the sharp “snap backs” in

labor trends may not repeat themselves in this recovery as they

have in most post-war recoveries. Under these special

circumstances, our initial assessment is that we see contracting

nominal GDP this year (of 1-3%), a return to muted-but-positive

(1-2.5%) growth in the transitional 2010-2011 timeframe, and a

“new normal" growth rate of 3-5% not returning until 2012.

3) We expect further top-line pressure on profits

as further de-leveraging in the economy mutes the normally sharp

earnings recovery that typically follows recessions. While

bottom-line results have been beating estimates due to

cost-cutting, top-line results still seem to be falling below

most analysts’ expectations. While inventory and cost-cutting

provide some positive support to earnings, challenges in

generating top-line growth lead us to conclude that pre-tax

corporate profits will likely return to a range of 6-10% of GDP

rather than the 12-15% levels which were experienced during the

credit and commodity boom of recent years. Currently, corporate

profits as a percent of GDP stand at 9.5%.

4) A key assumption is that the tax burden on

corporations remains steady. Here, we have chosen to

assume no increase in corporate profits until we learn more

about the legislative agenda for this in 2010. While it is

likely that corporate tax rates will prove to be an appealing

political target, it is far too soon to assess whether this

issue is ultimately a viable one given economic conditions. As

of the last period, after-tax corporate profits amounted to

roughly 78% of pre-tax profits according to National Income and

Product Account data.

Beyond the assumptions affecting operating earnings, several

considerations must be made given the special nature of bank

write-offs. Recently, the International Monetary Fund estimated

that total bank write-offs around the world will near $3

trillion. However, global banks have only recognized $1.5

trillion in losses and raised only $1.3 trillion in new capital,

according to Bloomberg data. Thus, we find it difficult to say

that we are completely out of the woods and anticipate that

additional hits are likely to be taken as more foreclosures in

residential real estate surface, as commercial real estate

losses are made evident, and as asset prices that back loan

portfolios continue to slip.

Against these challenges, more liberal mark-to-market

accounting, high lending margins, renewed investor interest in

bank secondary equity offerings, and some improvement in

depressed asset-backed security and credit markets offer some

near-term sense of stability for the banks. It would not

surprise us if there are even some near-term improvements in the

accounting measure for assets at some banks.

Foreign assets have outperformed U.S. dollar-denominated assets

in recent weeks, and the dollar sell-off was echoed in U.S.

Treasury markets. A zero-interest rate policy coupled with

significant new borrowings by the United States to fund these

deficits are contributing factors to dollar weakness. At the

same time, inflationary expectations have increased in

anticipation of the monetization of this debt. Under these

circumstances, it would not surprise us to see global capital

seek a more diversified "basket" of investments in other

currencies and assets to be held alongside existing dollar

assets.

For more clarity on debt and deficits, we look to the

Congressional Budget Office (CBO). According to the CBO, debt

held by the public will increase to 82% of GDP by 2019 from 57%

of GDP today under current spending plans. If we add in new

guarantees and obligations of companies in conservatorship (not

to mention under-funded entitlement programs and state

deficits), the fiscal "house" of the United States has

deteriorated markedly. One cause of the expected increase in

Federal debt burden is increased Federal spending relating to

"stimulus." The CBO now estimates that the new budget will

produce deficits of $1.7 trillion (11.9 percent of gross

domestic product, or GDP) this year and $1.1 trillion (7.9

percent of GDP) next year. These deficits will be the largest

deficits as a share of GDP since 1945 and the largest peacetime

deficits in history. Whatever the cause, these deficits must be

financed through taxes and borrowing — both of which have

negative implications for the dollar.

The most important factor (and most difficult to understand and

forecast) is the level of prices as seen through the value of

the dollar. We have seen a marked and historic shift away from

the private sector acting as the economy's borrower of last

resort. The Federal government is now taking up that role.

While it might seem odd that we need a "borrower of last resort"

at all, the fact is that the supply of money is dependent on

having willing borrowers. This is because the monetary

structure of the economy is tied to debt. Bank credit

(deposits) is the primary form of money in the modern economy,

and these deposits result from new borrowings. The retirement

of debt, on net, will produce a drain of the same. Hence, the

new drive for debt pay-down in the private sector, either

through defaults or early retirement, is a drain on the

availability of money and produces downward pressure on prices.

If falling prices become the expected outcome, it is

difficult to get spending and investing back on track, and the

economy can remain mired in a prolonged slump.

In 2002, Ben Bernanke explored the deflation problem and

concluded that, "under a paper money system, a determined

government can always generate higher spending and, hence,

positive inflation.” This was a very telling statement, because

it reminds us that the Fed, by itself, cannot bring about

inflation through the direct printing of money. It suggests

that only in "partnership" with Congress and other investors is

the Fed capable of converting government-issued debt into new

dollars that could prevent dollars and bank credit from

contracting. Therefore, the Fed Chair’s statement assumes that

there will be both a commitment by government to expand debt at

a rate sufficient to offset private sector contraction and that

foreign investors will remain committed to buying and holding

their dollar assets. It is far too early to assess

whether or not the Fed will be successful in their undertaking

to create just the right amount of inflation.

Recently, there has been a sharp increase in commodity prices in

both the industrial and precious metal markets. Gold prices

have crossed above $950 an ounce, silver has just had its

strongest monthly return since 1987, and the Commodity Research

Bureau's index of commodities is 25% higher than February. This

suggests monetary inflation, especially as stockpiles of oil and

other commodities remain curiously high. At the same time, the

decline in the trade-weighted dollar seems to be calling out for

the Fed to raise interest rates. Again, this suggests monetary

inflation. The difference in yield between the 10-year Treasury

and the 10-year Inflation Protected Treasury bond has risen to

nearly 2% from 0%. Again, this is another potential indication

of monetary inflation. And, lastly, the "term spread" or

difference between 3-month bond yields and 10-year bond yields

has risen to 345 basis points (3.45%) which are near record

highs. All of this is suggesting not only monetary inflation,

but that the Fed is now "in a box" on interest rates. They

appear “boxed in” because they cannot respond to inflationary

signals for fear of undoing improvements they have seen to date

and, at the same time, they are limited in the use of

traditional policy tools (setting short-term interest rates and

changing reserve requirements) because these policy tools have

already been exhausted. Instead of being focused on the

longer-term inflationary impact of large-scale debt

monetization, we believe that Fed policy is more focused on:

1.

the "output gap" (the economy is running well below potential

output);

2.

the lack of inflationary wage and employment trends;

3.

potential new losses in commercial real estate and consumer

credit; and

4.

a new and large wave of Option ARM and ALT-A mortgage resets.

Therefore, they will be forced to continue down the road of

direct purchases and guarantees of a wide variety of assets that

were once considered too risky for the Fed to own under past

governance. The long-run effects of these programs (both good

and bad) are unknown, but it is our sense that the Fed will find

it difficult to withdraw from these programs now that market

participants have come to expect Fed involvement in these

markets. These observations, together with a lack of hawkish

language from the Fed, suggest to us that Fed policy will remain

on the current track for some time to come, and the dollar to

remain relatively weak.

There has been improvement in our credit and economic "diffusion

indices." Market-based indicators suggest fading deflationary

pressure, along with some improvement in economic activity.

These improvements come on top of government-sponsored

improvement in the supply conditions for credit. At the same

time, there has been some improvement in the relative

performance between stocks and bonds, but the equity risk

premium still suggests a potentially attractive entry point for

equities from a historic perspective (assuming that the

economy and earnings continue to improve from here).

We still have concerns about what the quality of the recovery

will ultimately be, but believe it is appropriate to add some

exposure to equities and broaden out portfolios to include

foreign assets and corporate bonds, given recent improvement in

our indices. We continue to see relatively better performance

from growth sectors such as technology, healthcare, and consumer

discretionary over value sectors.

These changes are subject to change in either direction

depending upon the progression of inputs on the economy from

this point going forward. We may add or reduce exposure to

assets based on the relative performance of those assets and

changes to the macro-economic environment as demonstrated though

our various economic indicators. We will continue to monitor

and update you on the progress of the economy and our

recommendations as we track progress from here. |

Past Commentaries

March 13, 2009

A Big Hit to Wealth and What to Do Now?

More

March 5, 2009

A Questionable Plan and a Free Market Silver Lining?

More

January 7, 2009

Can Policymakers Create Just a Little Inflation?

More

December 11, 2008

Household Credit Turns Negative...

More

November 21, 2008

Credit: Don't Want It... Can't Get It...

More

September 24, 2008

Downgrading Outlook Based on Credit Freeze

More

September 15, 2008

Equity Markets Stumble on Lehman, Merrill, and AIG

More

September 9, 2008

No Change In Strategy On GSE Action

More

July 31, 2008

Quick Take on GDP Report

More

July 21, 2008

Valuation Are Better, But Markets Are Not Out of the

Woods

More

May 20, 2008

Buy the Dips

More

March 10, 2008

Investing During Recession

More

January 22, 2008

Global Sell-off

More

December 27, 2007

Outlook 2008

More

December 7, 2007

NBER President Raises Recession Concerns

More

November 28, 2007

Equity Risk Heightened - Allocation Remains Defensive

More

September 25, 2007

After the Rate Cut

More

July 30, 2007

The Case For Growth

More

June 15, 2007

Data Affirms Tactical Asset Allocation Posture

More

March 19, 2007

Cutting Earnings And Equity Target

More

| |