A Questionable Plan

and a Free Market Silver Lining

The new stimulus plan is designed to replace the loss of private sector spending as that sector attempts to reduce debt and increase savings in response to excess mortgage debt, falling asset prices, and the nearing of retirement for the largest segment of the population. It also puts the government in the role of “borrower and spender of last resort” to complement the actions taken by the Treasury and the Fed to stabilize the money supply. According to The Wall Street Journal, the plan amounts to $1.4 trillion of new taxes, $5 trillion in additional debt, and $1 trillion in new entitlements, on top of the $9 trillion of combined “rescue efforts” already put in place through previous stimulus, loans, and guarantees.

Despite the lack of credible evidence that government spending can replace private sector spending, government policy advocates insist that the spending plan is clearly stimulative. But the market’s “Bronx cheer” response to the new initiatives has been deafening, and with good reason. The primary reason is that the arrangement is devoid of financial incentives that foster spending and risk-taking in the private sector and focuses, instead, on the distribution of income. In the language of John Maynard Keynes, there is little in the package that stimulates private risk-taking and “autonomous investment” in things like factories, or even homes, for that matter.

By not changing financial incentives, the proposed government spending will likely be short-lived and require round after round of additional spending, taxation, and debt issuance. Like trying to ignite wet logs to start a fire, if the private sector is not receptive to the government’s attempts to ignite the economy, the net effect will likely be a waste of matches and not much to show for it.

While light on financial incentives, the plan is heavy in the area of moral and coercive incentives in the form of income and wealth redistribution. Simultaneous pursuit of two separate agendas, altering wealth and income distribution while simultaneously aiming to lift production, is not likely to produce the V-shaped recovery the market is hoping for.

Additionally, the plan comes at a time when aggressive government intervention is being perceived as threatening to capital and capital investment. These threats are not only the result of higher tax burdens, but also protectionist rhetoric on trade, and encroachment on private property rights relating to bailouts. The combination of a lack of a “carrot” in the form of financial incentives and a “stick” in terms of hostile government actions toward private capital threatens the supply of private capital necessary for sustaining recovery and job growth.

This is not a political statement. Rather, it is our best assessment of the economic impact of policy choices. Apart from the political aspects of wealth and income redistribution, it should be remembered that it is impossible to affect the distribution of production (through income and wealth) without affecting the level of production as well: a 100% percent tax on profits, for example, would certainly have a terrific impact on how much production occurs, as well as who receives its benefit. Thus, the current plan, which seeks to both stimulate output and production while simultaneously reorganizing the distribution of the wealth created through production, is a highly complex remedy born of a mixed agenda. In our judgment, such complexity increases the risk that the desired stimulative effect may become lost in execution, with negative consequences for all individuals regardless of income strata.

Markets are growing weary and skeptical of government intervention, and the Federal Reserve is under growing scrutiny as well. The continued slide in prices continues to beg the question whether fiscal and monetary policymakers are simply on the wrong path. Our last piece, Can Policymakers Create Just a Little Inflation, states that the shift in consumer attitudes away from leverage toward thrift, along with a parallel shift in investor attitudes away from risk, is having a direct impact on the value of money and assets. Wrongheaded policy has the potential to do more harm than good – just ask the Japanese. In the meantime, we still ask the same question: “Can policymakers create the inflation they desire while the private sector economy attempts to save more, spend less, and pay off debt?”

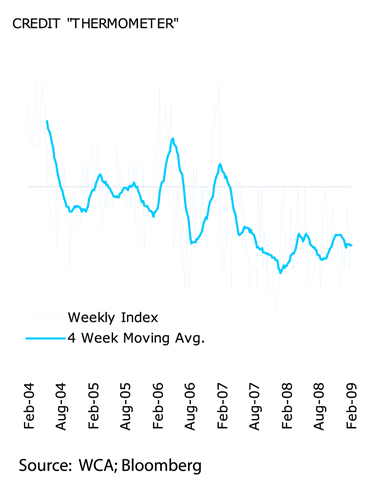

We are using various measures of credit market conditions to evaluate the forward-looking prognosis for the economy in response to policy decisions (for more on our "Credit Thermometer" see our September 24, 2008 Commentary. The markets, as measured by our Credit Thermometer (see chart), have been, on balance, unresponsive to the collective “rescue efforts” and “stimulation” since the fall. Some areas, such as inter-bank lending (as measured by the Libor-OIS spread), have narrowed; the dollar has strengthened versus other currencies; and commercial paper spreads have narrowed. However, other aspects of our review show continued deterioration. Notable is the ongoing underperformance by stocks in relation to bonds, and within that category the further underperformance by homebuilders and financial companies. In addition, there has been no letup in the ongoing acceleration in job losses. Even those credit markets that have shown improvement deserve an “asterisk” next to their performance, because they have been artificially enhanced by the intervention of the Federal Reserve and Treasury.

These market-based indicators overlay our basic economic observations that housing remains in a state of oversupply with more declines in value a near certainty; that credit remains in tighter supply with slack private sector demand; that corporate profits remain under intense pressure; and that private sector job losses continue to mount. Combining our real-time assessment of markets in our Credit Thermometer with these observations causes us to remain defensive in our portfolio posture. This is why we recently further increased our cash holdings in our model portfolios while reducing our equity exposure.

There is, however, a silver lining. That silver lining is in the potential for future returns in risk assets once the current economic downturn begins to subside. Stock prices, the quintessential risk asset, have fallen so dramatically that long-run investors are arguably much better compensated, relative to other “safe” assets, for assuming risk.

Consider the following:

1. Stocks have underperformed bonds by 63% since June 2007; by 73% since January 2000; and by 42% since December 1992.

2. Stocks have underperformed gold by 190% since June 2007; by 400% since January 2000; and by 25% since December 1992.

3. Stocks have underperformed real estate by 36% since June 2007; by 33% since January 2000; and by 20% since December 1992.

4. Stocks have underperformed cash by 58% since June 2007; by 55% since January 2000; but outperformed cash by 2% since December 1992.

The re-pricing of equities of late has been part of a broader decline in asset prices, which suggests that the issues confronting global markets are not unique to stocks, but speaks instead to a de-leveraging of the global economy and a temporary change in the intrinsic value of money. We recognize that the re-pricing of risk is an important pre-condition to an eventual bull market, but it does not cause the start of a bull market, nor does it sustain a bull market. That is why we await further confirmation that global housing, debt, and financial asset markets are beginning to clear naturally before committing new capital to equities in our tactical asset allocation models.

|

Past Commentaries

January 7, 2009

Can Policymakers Create Just a Little Inflation?

More

December 11, 2008

Household Credit Turns Negative...

More

November 21, 2008

Credit: Don't Want It... Can't Get It...

More

September 24, 2008

Downgrading Outlook Based on Credit Freeze

More

September 15, 2008

Equity Markets Stumble on Lehman, Merrill, and AIG

More

September 9, 2008

No Change In Strategy On GSE Action

More

July 31, 2008

Quick Take on GDP Report

More

July 21, 2008

Valuation Are Better, But Markets Are Not Out of the

Woods

More

May 20, 2008

Buy the Dips

More

March 10, 2008

Investing During Recession

More

January 22, 2008

Global Sell-off

More

December 27, 2007

Outlook 2008

More

December 7, 2007

NBER President Raises Recession Concerns

More

November 28, 2007

Equity Risk Heightened - Allocation Remains Defensive

More

September 25, 2007

After the Rate Cut

More

July 30, 2007

The Case For Growth

More

June 15, 2007

Data Affirms Tactical Asset Allocation Posture

More

March 19, 2007

Cutting Earnings And Equity Target

More

| |

To unsubscribe, please click here.

Company Name, Address and Contact Details

The information contained herein has been prepared from sources believed to be

reliable but is not guaranteed by us and is not a complete summary or statement

of all available data, nor is it considered an offer to buy or sell any

securities referred to herein. Opinions expressed are subject to change without

notice and do not take into account the particular investment objectives,

financial situation, or needs of individual investors. There is no guarantee

that the figures or opinions forecasted in this report will be realized or

achieved. Employees of Stifel, Nicolaus & Company, Incorporated or its

affiliates may, at times, release written or oral commentary, technical

analysis, or trading strategies that differ from the opinions expressed within.

Past performance is no guarantee of future results.

Indices are unmanaged, and you cannot invest directly in an index.

There are special

considerations associated with international investing, including the risk of

currency fluctuations and political and economic events. Investing in emerging

markets may involve greater risk and volatility than investing in more developed

countries. Due to their narrow focus, sector-based investments typically exhibit

greater volatility. Small company stocks are typically more volatile and carry

additional risks, since smaller companies generally are not as well established

as larger companies. Property values can fall due to environmental, economic, or

other reasons, and changes in interest rates can negatively impact the

performance of real estate companies. When investing in bonds, it is important

to note that as interest rates rise, bond prices will fall. High-yield bonds

have greater credit risk than higher quality bonds. The risk of loss in trading

commodities and futures can be substantial. You should therefore carefully

consider whether such trading is suitable for you in light of your financial

condition. The high degree of leverage that is often obtainable in commodity

trading can work against you as well as for you. The use of leverage can lead to

large losses as well as gains.

Stifel, Nicolaus & Company, Incorporated | Member SIPC & NYSE |

www.stifel.com |