|

|

An Adobe Acrobat version of this document can be found

here

|

|

|

December 14, 2009 |

| |

Bernanke’s Prayer

During the 1970s, former Federal Reserve

Chairman Paul Volker reviled inflation and prayed for an end

to rapidly rising prices. Today’s Chairman, Ben Bernanke, is

cursed with a world of falling prices which is hurting the

economy and adding to unemployment and foreclosures. In a

monetary sense, he knows that inflation may be the only

thing left that he can influence that has any chance of

stemming the tide of destabilizing asset write-downs,

defaults, and foreclosures. So in the fall of 2008, the Fed

and Treasury, along with a host of other central bankers and

governments, went “all in” to try to stem the liquidation of

debt and assets that began with the sub-prime mortgage

market in 2007. In some sense, this appears to have worked,

albeit at a very high price.

In the United States alone, over $10 trillion

of loans, investments, and taxpayer-financed guarantees were

put in place just to convince lenders that borrowers will

pay – even if the investments went bad. This backstopping of

private obligations took the form of government guarantees

of private loans, which is to say that the taxpayer was

forced to cosign obligations of private companies regardless

of price or rate of return. Whatever the ethical

implications of such a thing might be, policymakers were in

crisis mode and felt that it was the only possible

alternative to achieve the immediate goal of averting

meltdown. So far, it appears like that objective has been

achieved. Over the past six months, confidence in financial

markets seems to have improved, financial capital has begun

to flow, and asset prices have shown some initial signs of

stabilization. At the same time, inflation expectations have

begun to rise, as seen in a steepened yield curve, higher

commodity prices, and a higher inflation rate priced into

inflation-protected Treasury bonds. Thus, it seems as if

Bernanke’s prayer has been answered.

Our own quantitative assessment of the

economy shows that such backstopping has been effective in

turning around markets and various economic indicators. Our

diffusion index, which measures changes in thirty different

indicators of health in the U.S. and foreign economies,

bottomed last winter and now shows that most measures are in

the process of turning for the better. We see that banks are

lending to one another again at reasonable rates; we see

that larger companies can get access to short-term financing

at economically attractive rates; there are some signs of

slowing in the rate of job losses; inventory levels are

improved relative to sales; and so forth. All of this is

positive news and a welcome development.

The improvement is also seen in new data compiled by the

Federal Reserve. That data shows the value of household real

estate rising right alongside the value of equity markets

since the spring. As a result, household net worth has

increased from $48 to $53 trillion in six months. All of

this is positive and has created some sense of optimism that

the economy may be coming back from the recession and has

already begun an economic recovery. We hear nightly about

“V”-shaped growth and “green shoots.”

Yet, for many, there remain some unsettling aspects about

the current situation. We know this because the savings

rate has risen to 4% from below 1% in April 2005. This

increase in savings is certainly not about capturing a high

rate of interest offered by banks, since those rates are

near 0%. Nor is it about consumers having lots of cash

burning a hole in their pocket. The increase relates to

uncertainty about the future. Based on Federal Reserve

data, the average person now holds 36 weeks of income in the

form of deposits versus 34 weeks a couple of years ago. It

is common now for retirement and other savings plans to be

under-funded – in part because of ten years of an

underperforming stock market but also due to changes in

assumptions about assets such as real estate. Similar

shortfalls are being recognized by national government,

state and local governments, large and small businesses, and

charitable organizations. Individuals are aware of these

imbalances, and the threat of higher tax burdens adds to

already tight personal finances.

Since individuals and businesses are not yet convinced that

a turn is at hand, the drive to savings is also accompanied

by a desire to avoid and reduce debt. As for debt reduction,

it can be achieved through pay-down or default and, in the

case of another government intervention, forgiveness. The

Mortgage Bankers Association now reports a foreclosure rate

of 4.5% on all loans compared with a 1% rate, which has been

the more typical experience over the past couple of decades.

Ironically, just as savers are piling into savings at very

low rates, there is scant evidence to suggest that record

low mortgage rates are encouraging a massive new round of

borrowing.

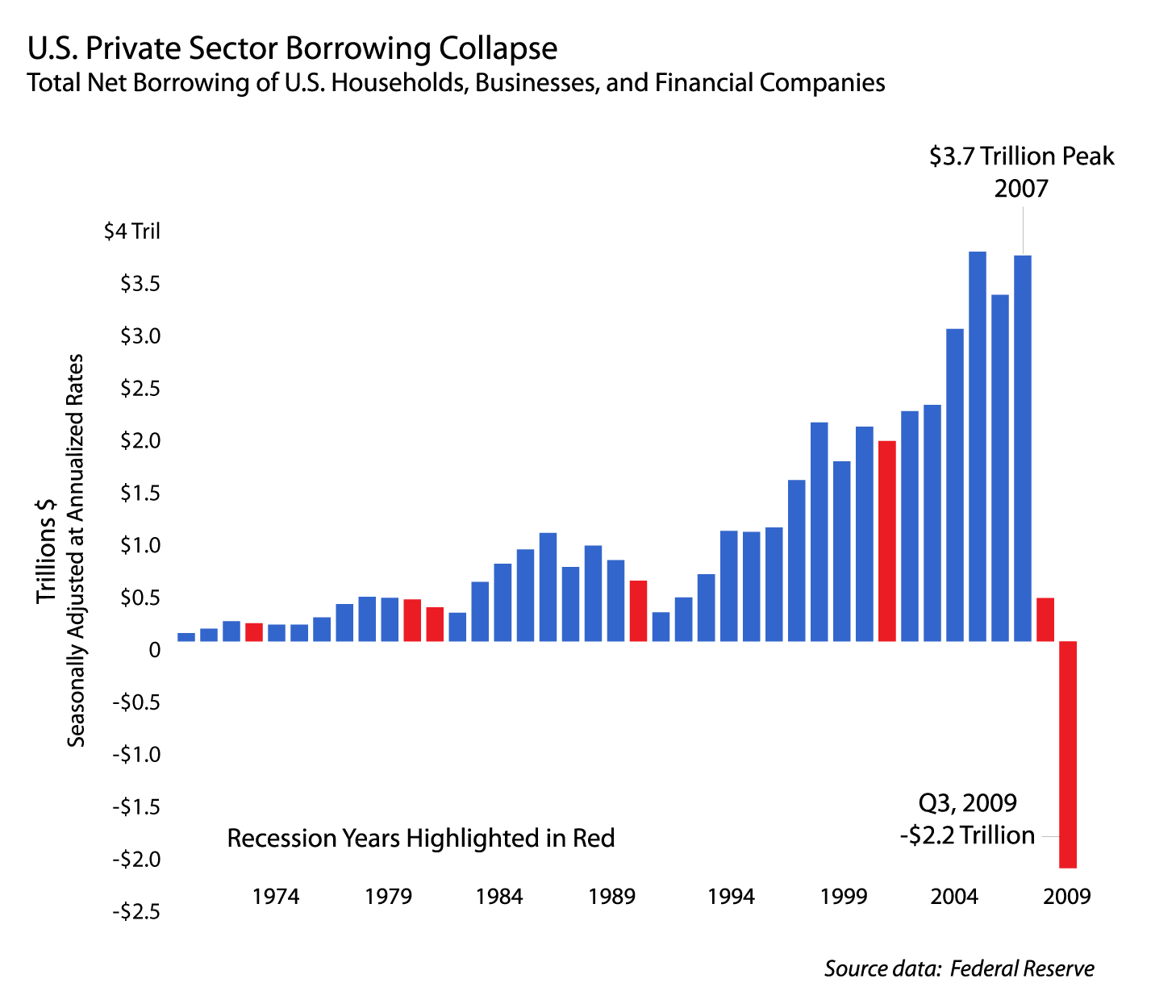

[Click chart to enlarge]

The Federal Reserve’s data shows that total borrowing coming

from the private sector (households, businesses, and

financial companies) is not only lower, but sharply

contracting at a -$2.2 trillion annualized rate as seen in

the above chart. There are three things I want to bring to

your attention about this -$2.2 trillion number. First, the

-$2.2 trillion is a “net” number. In other words, there is

some amount of new borrowing that is occurring, but the

amount of borrowing that is being paid off or written off is

greater than the amount being incurred by -$2.2 trillion. So

the amount of debt extinguishment is actually much higher

than the -$2.2 trillion net number. Second, the -$2.2

trillion number is the only negative number on record with

the Federal Reserve’s data series dating all the way back to

1946. When debt expansion slows, there is a strong tendency

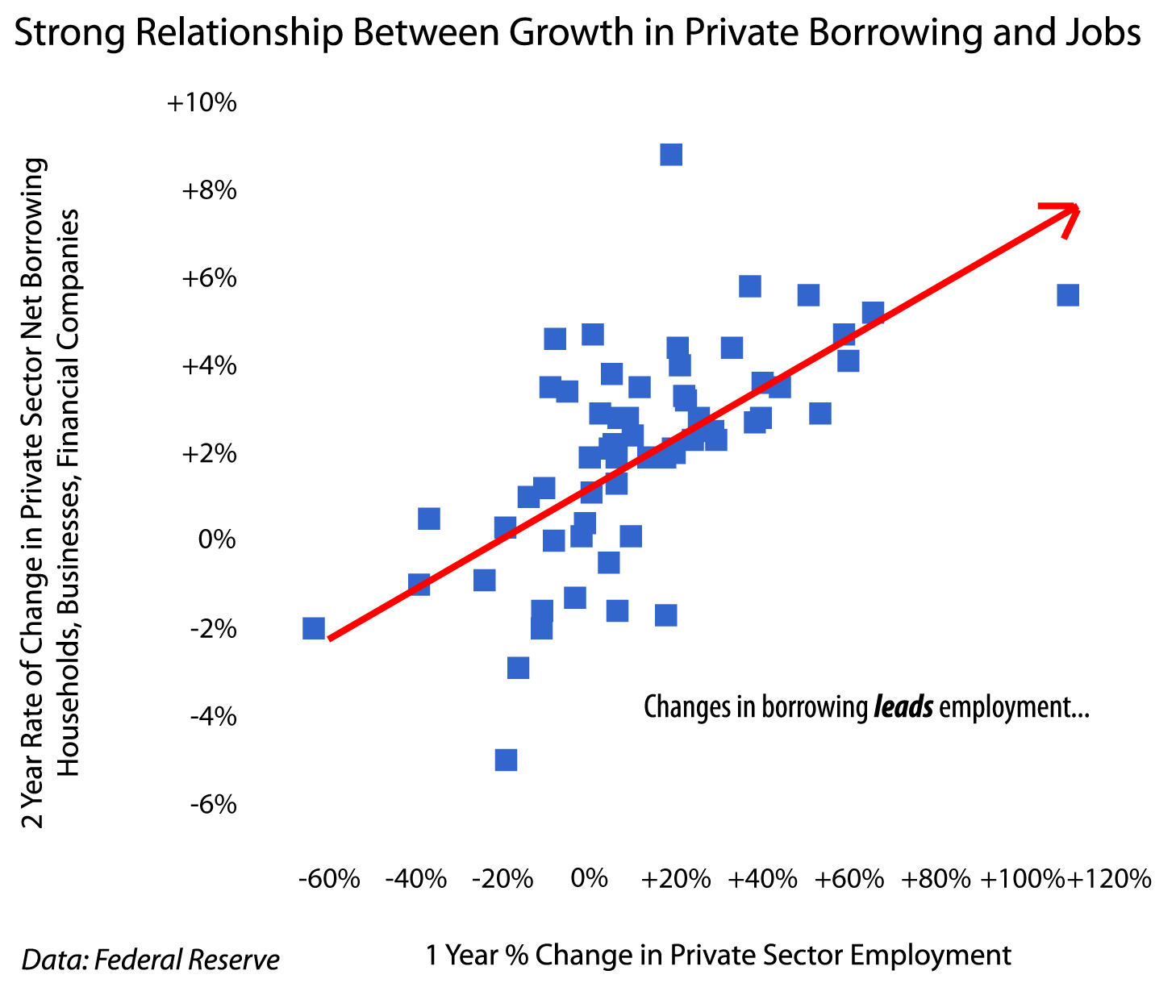

for the economy to falter. This is apparent when comparing

changes in private sector net borrowing to changes in

private sector employment. The following graph depicts the

relationship between debt and employment growth in the

private sector. We see here that there is a strong tendency

for private sector employment (seen along the x-axis) to

rise and fall in response to a change in private sector

borrowing (seen along the y-axis). Thus, the larger the

contraction in private borrowing, the larger the expected

falloff in private employment. It is not at all surprising

that the rate of unemployment has reached 10% with the rate

of underemployment reaching near 17%, in light of the fact

that private borrowing peaked in the third quarter of 2007

at a net annualized growth rate of $4.7 trillion and has now

slid to a contracting rate of -$2.2 trillion on an

annualized basis. It is hard to envision how private sector

employment would increase alongside private sector debt

liquidation.

[Click chart to enlarge]

One other surprising fact about this data is that, despite the

improvement in financial markets during the second and third

quarter, the pace of debt liquidation appears to be

accelerating. Households were liquidating debts at an annualized

rate of -$160 billion in Q1; -$215 billion in Q2; and -$351

billion in Q3. Similarly, companies were growing debt at an

annualized rate of $53 billion in Q1; began net liquidation to

the tune of approximately -$249 billion in Q2; and liquidated at

a rate of -$283 billion in Q3. Financial companies, which hold

the largest concentration of debt among any sector at over $16

trillion, have been liquidating debt at a $1.5-$2 trillion pace

this year. This process has been aided by the Federal Reserve,

which has injected capital into the banks by buying up roughly

$1 trillion of assets from those same banks. We anticipate that

the Fed will attempt to engineer additional purchases well into

2010, which could further balloon the size of their balance

sheet. Stay tuned.

The seemingly counter-intuitive fact that accelerating private

sector debt liquidation is occurring alongside a wide variety of

observations showing improvement in the economy can only be

explained by two potential phenomena. It could be that the

public senses that the improvements are superficial and

tentative because they do not see the positive effect of

government actions in their immediate circumstances. On the

other hand, the trend toward higher savings rates and debt

liquidation could have longer-lived secular characteristics.

As we have written about in the past, potential drivers for

longer-run, secular shifts are:

1. A much higher degree of private sector debt and leverage than

in the past;

2. Boomers’ exit from peak spending years;

3. A negligible change in the cost of money from boom years;

4. Structural changes to regulatory and tax code that inhibit

risk-taking.

Ultimately, time will whether this is just another credit cycle

and will follow the normal cyclical pattern leading to a

sustained recovery, or whether these secular changes produce a

markedly different outcome. So far, markets have answered Ben

Bernanke’s prayer. Soon, we will see if the private sector is

similarly inclined.

|

Past Commentaries

September 30, 2009

Fourth Quarter Tactical Asset Allocation Observations

More

August 24, 2009

Trough Earnings and the Path Forward

More

July 20, 2009

Third Quarter Tactical Asset Allocation Observations

More

March 13, 2009

A Big Hit to Wealth and What to Do Now?

More

March 5, 2009

A Questionable Plan and a Free Market Silver Lining?

More

January 7, 2009

Can Policymakers Create Just a Little Inflation?

More

December 11, 2008

Household Credit Turns Negative...

More

November 21, 2008

Credit: Don't Want It... Can't Get It...

More

September 24, 2008

Downgrading Outlook Based on Credit Freeze

More

September 15, 2008

Equity Markets Stumble on Lehman, Merrill, and AIG

More

September 9, 2008

No Change In Strategy On GSE Action

More

July 31, 2008

Quick Take on GDP Report

More

July 21, 2008

Valuation Are Better, But Markets Are Not Out of the

Woods

More

March 10, 2008

Investing During Recession

More

January 22, 2008

Global Sell-off

More

December 27, 2007

Outlook 2008

More

December 7, 2007

NBER President Raises Recession Concerns

More

November 28, 2007

Equity Risk Heightened - Allocation Remains Defensive

More

September 25, 2007

After the Rate Cut

More

July 30, 2007

The Case For Growth

More

June 15, 2007

Data Affirms Tactical Asset Allocation Posture

More

March 19, 2007

Cutting Earnings And Equity Target

More

| |

To unsubscribe, please click here.

Company Name, Address and Contact Details

Opinions expressed are subject to change without notice and do not take into

account the particular investment objectives, financial situation, or needs of

individual investors. There is no guarantee that the figures or opinions

forecasted in this report will be realized or achieved.

The information contained herein has been prepared from sources believed to be

reliable but is not guaranteed by us and is not a complete summary or statement

of all available data, nor is it considered an offer to buy or sell any

securities referred to herein. Employees of Stifel, Nicolaus & Company, Incorporated or its

affiliates may, at times, release written or oral commentary, technical

analysis, or trading strategies that differ from the opinions expressed within.

Past performance is no guarantee of future results.

Indices are unmanaged, and you cannot invest directly in an index.

There are special

considerations associated with international investing, including the risk of

currency fluctuations and political and economic events. Investing in emerging

markets may involve greater risk and volatility than investing in more developed

countries. Due to their narrow focus, sector-based investments typically exhibit

greater volatility. Small company stocks are typically more volatile and carry

additional risks, since smaller companies generally are not as well established

as larger companies. Property values can fall due to environmental, economic, or

other reasons, and changes in interest rates can negatively impact the

performance of real estate companies. When investing in bonds, it is important

to note that as interest rates rise, bond prices will fall. High-yield bonds

have greater credit risk than higher quality bonds. The risk of loss in trading

commodities and futures can be substantial. You should therefore carefully

consider whether such trading is suitable for you in light of your financial

condition. The high degree of leverage that is often obtainable in commodity

trading can work against you as well as for you. The use of leverage can lead to

large losses as well as gains.

Stifel, Nicolaus & Company, Incorporated | Member SIPC & NYSE |

www.stifel.com |

|

| | |