Equity Markets Stumble:

Implications for Strategy

The unprecedented series of events of this weekend,

including an expected Lehman bankruptcy, Merrill acquisition

by Bank of America, and AIG’s appeal to the Federal Reserve

for aid is all part of the ongoing de-leveraging of the

economy that we have been discussing for some time. The

implications of this is that the credit system will remain

in a delicate state for an extended period of time, leaving

tighter credit conditions, somewhat higher borrowing cost

for qualified borrowers, and leaving out less qualified

borrowers.

In light of this, our expectation for recovery must now be

pushed out beyond the first quarter of 2009. We are not

changing our asset allocation based upon these events but

have changed the period of time over which we had expected

to increase our equity exposure.

At this juncture, we should take a moment to re-examine some

of the things that the equity markets have going for them

and what continues to work against them:

The equity market a year ago appeared richly valued with the

S&P 500 reaching a peak of 1,565, which was 18.5x our

expected earnings figure of $85 for the full year (keep in

mind that consensus wisdom at the time had earnings for the

S&P 500 well over $100). Today, the S&P 500 is down over

20%, with the financial sector down more than twice that

amount. During this time, Treasury bond prices have risen

and the risk premium paid to own equities, along with many

other kinds of risky assets, has increased. Therefore, an

incentive for new buyers has been reinserted into the

calculus for equity investing.

We estimate, based on a recessionary case for the economy,

that S&P 500 earnings will be closer to $80 in 2008 – a

modest decline from last year’s actual earnings of $82.54 as

reported by Standard & Poor’s on their web site. While

analysts continue to expect a 35% earnings resurgence in

2009 to $106, we find that estimate to be exceedingly

optimistic based on what we expect the economy to deliver in

coming months.

Allowing for the lower interest rate environment and

factoring in much lower than consensus earnings for 2009, we

place a new estimate of the S&P 500’s “fair value” range at

1,260 to 1,390.

This week we should get another installment of quarterly

data on credit demand from the economy in the form of the

Flow of Funds Report. Our readers know that we have been

watching the net new borrowings number from households to

provide us a window into the real condition of the American

household and as an indicator of how deep this credit-driven

contraction will be. We note that, in the past, a two-thirds

contraction in net new borrowing typically marked the bottom

in terms of a credit slowdown. To date, we have seen new

credit demand slip to a 3% annual growth rate after growing

at closer to 16% at the peak of the housing bubble. Any

outright contraction in this figure would be unprecedented

in modern history and would force us to confront an outright

deflation – something not seen in the United States in over

a generation.

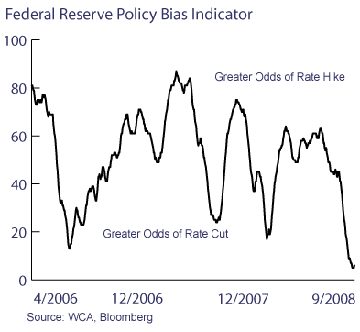

For what it’s worth, we now view further rate cuts a near

certainty. In addition to this weekend’s drama, every

ingredient into our Policy Bias Indicator (seen below) now

signals rate cuts are needed. Specifically, the forward

inflation spread priced into the TIPs market has now

collapsed (now below 2%); the term spread has been moving

sideways for much of the year (rather than rising); the

level of default risk priced into credit markets has been

rising; the cumulative advance/decline line for the major

U.S. exchanges continues to make new lows; and the

trade-weighted value of the dollar has spiked materially

since the housing bailout bill was announced in mid-July.

The earnings correction continues, and we expect it to

continue for several additional quarters. In addition,

analysts seem to be far behind the curve in terms of cutting

their expectations and outlook. From an economy-wide

perspective, for example, after-tax corporate profits

through the second quarter slipped to 9.5% of GDP from its

prior multi-decade peak of 10.9% achieved in the fourth

quarter of 2006. The average ratio has been closer to 6%

since the early 1960s and has been as low as 3%. While

peak-to-trough cycles for profits can last for several

years, typically the negative effect of slipping profits on

stock prices abates once investors and analysts adjust

expectations accordingly. Unfortunately, we believe that

there is further adjustment ahead.

Another spot to check is consumer confidence as a barometer

for economic conditions and attractive entry points to

markets during times of distress. Since past recessions

usually last for a year or more, and since markets

anticipate economic recovery about halfway through, it is

interesting that markets tend to perform best from periods

of very low optimism, which are often associated with low

points or panic in the economy. Current readings on

confidence are very low indeed and near every past recession

bottom since 1969. A long-run-oriented and contrarian

investor (with much fortitude) would tend to find this

environment an attractive one to build positions in

anticipation of recovery in years ahead despite the ominous

overtones in the economy and media.

Housing remains a serious concern to us as the supply of

homes for sale remains excessively high and signals further

deterioration in prices ahead. Of course, such deterioration

is not a welcome forecast for banks and investment banks who

are hoping for stability in order to stop the erosion of

bank capital. Such erosion has the immediate effect of

unleashing the kind of chaos now playing out among venerable

Wall Street financial institutions but also has the

potential to seriously inhibit a recovery in credit

availability and the broader economy in the years ahead.

That outcome could materially affect the outlook for

equities if such credit availability becomes increasingly

scarce.

The events currently unfolding are part of the de-leveraging

process that the economy must now endure. The process is far

from complete, and the secondary, fallout effects on the

economy are not yet fully determinable. What is clear is

that this process is not optional, but mandatory, and the

ultimate course this will run is unknowable with certainty.

We also know that the vetting of issues and the weight of

market forces will cause uncertainty to be removed over time

one issue at a time.

After a careful review of these and other considerations, we

are making no immediate change to our asset allocation as

the result of the current volatility. However, we now expect

that secondary effects as the result of the fallout of the

de-leveraging process will extend the timeline for recovery.

Therefore, while we continue to look to add to our equity

position over time, the pace of such additions will likely

be slower than previously envisioned.

|

Past Commentaries

September 9, 2008

No Change in Portfolio Strategy Despite Treasury GSE

Action

More

July 31, 2008

Quick Take on GDP Report

More

July 21, 2008

Valuation Are Better, But Markets Are Not Out of the

Woods

More

May 20, 2008

Buy the Dips

More

March 10, 2008

Investing During Recession

More

January 22, 2008

Global Sell-off

More

December 27, 2007

Outlook 2008

More

December 7, 2007

NBER President Raises Recession Concerns

More

November 28, 2007

Equity Risk Heightened - Allocation Remains Defensive

More

September 25, 2007

After the Rate Cut

More

July 30, 2007

The Case For Growth

More

June 15, 2007

Data Affirms Tactical Asset Allocation Posture

More

March 19, 2007

Cutting Earnings And Equity Target

More

| |

To unsubscribe, please click here.

Company Name, Address and Contact Details

The information contained herein has been prepared from sources believed to be

reliable but is not guaranteed by us and is not a complete summary or statement

of all available data, nor is it considered an offer to buy or sell any

securities referred to herein. Opinions expressed are subject to change without

notice and do not take into account the particular investment objectives,

financial situation, or needs of individual investors. There is no guarantee

that the figures or opinions forecasted in this report will be realized or

achieved. Employees of Stifel, Nicolaus & Company, Incorporated or its

affiliates may, at times, release written or oral commentary, technical

analysis, or trading strategies that differ from the opinions expressed within.

Past performance is no guarantee of future results. There are special

considerations associated with international investing, including the risk of

currency fluctuations and political and economic events. Investing in emerging

markets may involve greater risk and volatility than investing in more developed

countries. Due to their narrow focus, sector-based investments typically exhibit

greater volatility. Small company stocks are typically more volatile and carry

additional risks, since smaller companies generally are not as well established

as larger companies. Property values can fall due to environmental, economic, or

other reasons, and changes in interest rates can negatively impact the

performance of real estate companies. When investing in bonds, it is important

to note that as interest rates rise, bond prices will fall. High-yield bonds

have greater credit risk than higher quality bonds. The risk of loss in trading

commodities and futures can be substantial. You should therefore carefully

consider whether such trading is suitable for you in light of your financial

condition. The high degree of leverage that is often obtainable in commodity

trading can work against you as well as for you. The use of leverage can lead to

large losses as well as gains. Indices are unmanaged, and you cannot invest

directly in an index.

Stifel, Nicolaus & Company, Incorporated | Member SIPC & NYSE |

www.stifel.com |