No Change in Portfolio Strategy Despite Treasury GSE Action

Now that the Treasury has made clear it's plan of action for

the Government Sponsored Entities (GSEs), we see little in

it's construction that forestalls the ongoing housing

recession, prevents rising joblessness, or reverses the

recessionary tendencies which have become even more

entrenched in recent months. While the action gives

comfort to agency debt-holders that the United States'

government will likely make good on all GSE debt

obligations, there remains significant questions about the

long-term role that the GSEs will play in credit markets

once the 2008-2009 period passes.

In addition, neither the equity injections, credit lines,

purchase arrangements, or temporary increases in portfolio

limits offer any guarantee that credit terms will be changed

to make mortgages more available to potential homebuyers

than they currently are. Therefore, there is no reason

to expect a quick and material improvement in the imbalances

that continue to confront real estate markets.

In fact, over the short-run, the plan could have the

negative effect of making credit even tighter as the

government sponsored entities are forced to comply with the

new set of standards that will emerge under conservatorship.

Looking beyond the next year, the call to materially shrink

the entities in the post-2010 period would profoundly change

the structure of banking and credit markets. Without

an alternative structure in place, the pace of credit

creation would likely slow and the cost of credit would

likely rise. Unfortunately, the Treasury's

recent actions stop short of offering a vision of what such

a system may look like and, instead, leaves that debate to

the Congress and the next administration while, at the same

time, leaving the GSEs intact as functioning entities.

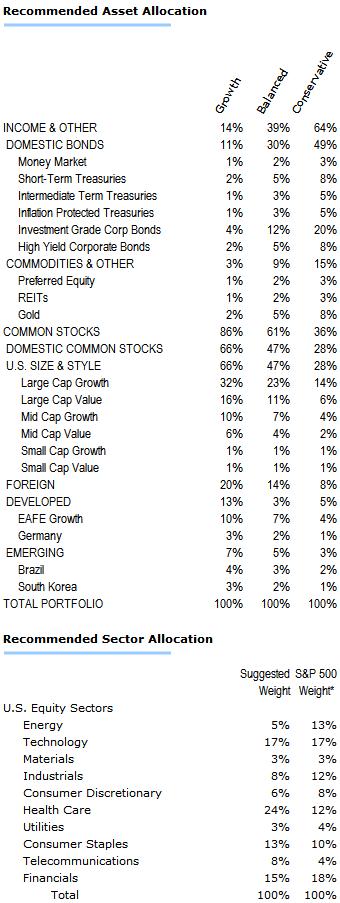

We welcome the action as a first step to reform, but are

making no change to our recommended

tactical asset allocation in response to the Treasury's

recently announced GSE action.

Instead, we remain focused on monitoring changes in the five

key indicators which we believe are most important as it

relates to portfolio decisions and the outlook for the

economy. By way of reminder, these five indictors have

been and remain:

D

Housing

(continuing oversupply, prices falling)

D

Credit

(shrinking

availability and demand for loans)

D

Corporate profits

(peak margins,

declining level)

D

Private sector employment

(mounting job losses)

C

Pricing of risk in financial markets

(risk better priced versus a year ago)

|

Past Commentaries

July 31, 2008

Quick Take on GDP Report

More

July 21, 2008

Valuation Are Better, But Markets Are Not Out of the

Woods

More

May 20, 2008

Buy the Dips

More

March 10, 2008

Investing During Recession

More

January 22, 2008

Global Sell-off

More

December 27, 2007

Outlook 2008

More

December 7, 2007

NBER President Raises Recession Concerns

More

November 28, 2007

Equity Risk Heightened - Allocation Remains Defensive

More

September 25, 2007

After the Rate Cut

More

July 30, 2007

The Case For Growth

More

June 15, 2007

Data Affirms Tactical Asset Allocation Posture

More

March 19, 2007

Cutting Earnings And Equity Target

More

| |

To unsubscribe, please click here.

Company Name, Address and Contact Details

The information contained herein has been prepared from sources believed to be

reliable but is not guaranteed by us and is not a complete summary or statement

of all available data, nor is it considered an offer to buy or sell any

securities referred to herein. Opinions expressed are subject to change without

notice and do not take into account the particular investment objectives,

financial situation, or needs of individual investors. There is no guarantee

that the figures or opinions forecasted in this report will be realized or

achieved. Employees of Stifel, Nicolaus & Company, Incorporated or its

affiliates may, at times, release written or oral commentary, technical

analysis, or trading strategies that differ from the opinions expressed within.

Past performance is no guarantee of future results. There are special

considerations associated with international investing, including the risk of

currency fluctuations and political and economic events. Investing in emerging

markets may involve greater risk and volatility than investing in more developed

countries. Due to their narrow focus, sector-based investments typically exhibit

greater volatility. Small company stocks are typically more volatile and carry

additional risks, since smaller companies generally are not as well established

as larger companies. Property values can fall due to environmental, economic, or

other reasons, and changes in interest rates can negatively impact the

performance of real estate companies. When investing in bonds, it is important

to note that as interest rates rise, bond prices will fall. High-yield bonds

have greater credit risk than higher quality bonds. The risk of loss in trading

commodities and futures can be substantial. You should therefore carefully

consider whether such trading is suitable for you in light of your financial

condition. The high degree of leverage that is often obtainable in commodity

trading can work against you as well as for you. The use of leverage can lead to

large losses as well as gains. Indices are unmanaged, and you cannot invest

directly in an index.

Stifel, Nicolaus & Company, Incorporated | Member SIPC & NYSE |

www.stifel.com |