Investing During Recession

The economy has lost private sector jobs for three straight

months, credit markets continue to worsen, and confidence

levels for businesses and consumers alike have plummeted.

Corporate profit growth has been declining, especially for

banks, where write-offs are impacting book value and

impinging upon the ability of financial institutions to

extend credit.

This is not an environment that is conducive to growth. We

now believe that the economy has entered into a recession

that began in the fourth quarter of last year. This,

however, should not come as much of a surprise to those who

follow economic cycles. Martin Feldstein, the head of the

National Bureau of Economic Analysis, has patiently

deflected direct questions about recession with

probabilistic answers. However, we now see that there is a

significant decline in economic activity that has spread

beyond homebuilders – notably to banks, automobile

manufacturers, and retailers.

The Federal Reserve, despite their best intentions to create

an environment that stimulates credit creation, has not been

successful. Since the first Fed Funds rate cut last

September, the Dow has lost an additional 12%; bonds have

advanced 7%; gold has advanced another 35%; home prices have

slipped 7%; and the dollar has declined 7%. The banks have

become less willing and able to lend as much of the

economy’s recently minted — and poorly collateralized — debt

has become too much for financial institutions to hold on

their balance sheets.

The real issue is the amount of debt (credit) that has been

taken on (extended) by banks in the last cycle for the

funding of everything from mortgages to private equity

deals. Based on Federal Reserve data, the ratio of

debt-to-disposable income has risen to 140% of income from

an already elevated 100% ratio seen at the end of the 1990s

equity-led economic boom.

Before the clamor for a “super-SIV” and government-sponsored

efforts to save the housing market, there were banks and

borrowers who, through a carefully orchestrated dance,

created additional money (also known as “liquidity”) which

primed the economic machine. There are limits, however, to

how much liquidity can be absorbed by the economy the same

way that there are limits to how much can be consumed at any

given meal (and consequences that arise when we go

overboard).

Between 2000 and 2005, new borrowing as a percent of GDP

rose to 17.5% — far higher than the 9% ratio seen in the

1990s but not quite as high as the prior peak of 22% set in

1985. During these five years, total household debt

increased to $14.3 trillion from $6.7 trillion while incomes

grew to $10.3 trillion from $6.7 trillion. As mentioned

earlier, the ratio of debt-to-income now stands at 1.4 to 1

versus 1 to 1 in just seven years.

The resulting increase in money supply that accompanied such

massive credit formation has hurt the value of the dollar

and propelled asset prices, notably housing, to previously

unheard of levels. Now, the unwinding of the asset bubble

and the re-evaluation of the creditworthiness of the

borrowers is throwing the cycle in reverse.

In short, the inability and unwillingness of banks to extend

loans relates directly to the fact that residential real

estate prices have begun to fall and what little underlying

collateral there was for newly minted mortgages is now

impaired. According to a Goldman Sachs economist, if home

prices continue to slide by an additional 10% in 2008 that

30% of all mortgaged homeowners will have negative equity in

their homes. In other words, $3 trillion of mortgages will

have a face value in excess of the underlying real estate.

As employment trends head negative, the effect will likely

accelerate the foreclosure rate, force additional home price

adjustments nationally (there are nearly 5 million unsold

home and condominium units), and further erode banks’

capital and capacity to lend. Thus, the Federal Reserve must

take action on two fronts -- address the credit market's

immediate problems and cut short-term rates to help the

economy through recession.

The rate cuts to date, 2.25 percentage points, with

additional cuts likely should help the economy later this

year and into 2009. Rate cuts, while quite visible and

welcomed by investors, are not solutions for the credit

market squeeze which is expanding. Most credit spreads are

now wider (worse) than they were when the credit crisis

first hit last summer.

The Fed's plan to combat this condition is to pump another

$200 billion into short-term funding markets through a newly

created term auction facility alongside traditional

repurchase agreements. While such short-term facilities have

been in use since last summer, this time the Fed is

accepting a wider variety of collateral, including mortgages

and corporate loans which are part of the credit market's

problem to date. Providing liquidity for assets that have

been harder to sell in the open market is a tangible relief

step for bank capital. But the Fed can only do so much.

The emergence of these problems during a Presidential

election cycle multiplies the number of proposed solutions

and amplifies the sense of urgency. It is appropriate to

recall, however, that wrong-headed policies can make matters

worse. Attempts by bank regulators in Japan during the 1990s

to sweep their banking issues under the rug backfired, and

decisions made by our Federal Reserve in the 1920s and 1930s

to raise interest rates while remaining tied to the gold

standard further compounded the problems of that era. Today,

there are a variety of proposals to fix what ails the

housing market, and ultimately, the economy. There has been

talk of mortgage remediation, expansion of the government

and their sponsored agencies, and now a dialogue is emerging

about direct write-downs of mortgages by banks. As all of

this unfolds, falling home prices does improve housing

affordability and increases expected rates of return to

prospective buyers of property and mortgage-related assets.

In the end, the prospective rate of return to new investors

must be sufficient to attract risk capital. In the coming

years, however, the difficult lessons now being (re)learned

will likely result in more costly credit with greater

requirements for collateral on the part of borrowers.

“time heals all wounds..."

The adjustment process that has led us to these current,

more difficult economic times began in 2005. The cost of

money began to move higher as the Federal Reserve raised

interest rates; hurricane Katrina brought about destruction

in the Gulf, which fanned existing concerns about energy

prices; and for the first time in many years, the national

homeownership rate began to decline due to the

unaffordability of homes.

Meanwhile, credit and equity markets remained oblivious to

these changes and continued to price assets (especially

mortgage-related assets) to levels that seemed to imply a

riskless environment despite ongoing rate increases that led

to an inverted yield curve — a classic warning signal for

the economy.

As reality began to set in last summer, we saw markets start

to reprice risk. For example, real estate investment trusts

offered very little yield to investors prior to last July as

evidenced by the yield on the National Association of Real

Estate Investment Trusts’ index which fell far below the

yield on risk-free Treasury bonds. Today, that yield is more

than 2% over long-term Treasury bond yields and close to

their historic average. This, and the repricing of many

other markets, is healthy and creates incentive for new

capital to enter markets.

This is not to suggest that markets have completed this

process. One meaningful measure of overall market

expectations is the relative performance between stocks and

bonds. Here, we see equities (measured broadly by the

Russell 3000 Index) down 25% over eight months. While that

performance is about average for a bond-led cycle, it is

less severe than a bond-led cycle that also coincides with

recession. The average bond-led cycle during those periods

is closer to 1.5 years and a 35% underperformance by stocks

(outperformance by bonds). Thus, with recession looking

increasingly like reality, we would expect that equity

markets will likely correct for an additional period of

time.

The four key items to watch in order to gauge where we are

in the economy have been and remain:

• Trends in Household Demand for credit;

• Trends in Private Sector employment;

• Trends in corporate behavior vis-à-vis capital

expenditures and hiring plans in response to uncertainty and

declining profit growth;

• Rate of drawdown of excess supply of real estate still for

sale.

Unfortunately, we are unable to convincingly say that any of

these four trends have improved. Each category continues to

show accelerating deterioration at this time, with household

credit expanding at just 5% in the last quarter of ’07, with

corporate hiring and capital spending flat-to-down according

to the Federal Reserve’s recently released Flow of Funds

Survey, and last week’s negative employment report for

February and the recent data from the National Association

of Realtors on housing supply.

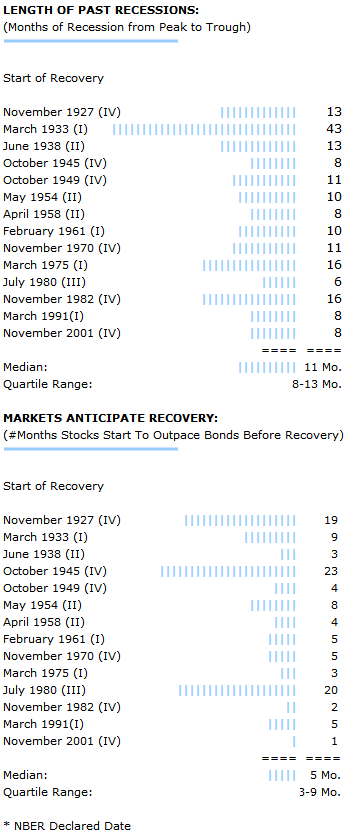

While the ultimate outcome is anyone’s guess, history has

shown that bonds tend to outperform stocks headed into

recessions. The table to the right looks at past recessions;

the length of the recession; and the performance of stocks

compared to bonds headed into recovery.

If we assume that a recession began late last year and will

last for a median length of time (about 8-13 months

historically, see table below) we might conclude that an

ordinary recession would take us through most of the year

this year with some hope for recovery in the later part of

the year or in the first part of 2009. Since markets also

tend to anticipate recovery about 3-9 months prior to the

start of recovery (see table below), we might expect to see

some change in market leadership, from bonds to stocks in

the second or third quarter of the year. If we do not see

such a change in leadership the market’s message would

obviously be more ominous as it relates to the economy in

2009.

Our tactical asset allocation recommendations continue to

offer a highly conservative profile for the current market.

In light of the ongoing issues confronting markets and the

economy, we continue to emphasize large over small

capitalization stocks, growth over value, and consistent

sectors such as staples, healthcare, and utilities

(including telecommunications). Outside of the domestic

equity component, we maintain a diversified portfolio of

bonds, foreign equities, and a modest exposure to gold as a

hedge against potential future erosion of dollar-based

assets.

March 10, 2008

Joseph V. Battipaglia

Market Strategist, Private Client Group |

Past Commentaries

January 22, 2008

Global Sell-off

More

December 27, 2007

Outlook 2008

More

December 7, 2007

NBER President Raises Recession Concerns

More

November 28, 2007

Equity Risk Heightened - Allocation Remains Defensive

More

September 25, 2007

After the Rate Cut

More

July 30, 2007

The Case For Growth

More

June 15, 2007

Data Affirms Tactical Asset Allocation Posture

More

March 19, 2007

Cutting Earnings And Equity Target

More

| |

To unsubscribe, please click here.

Company Name, Address and Contact Details

The information contained herein has been prepared from sources believed to be

reliable but is not guaranteed by us and is not a complete summary or statement

of all available data, nor is it considered an offer to buy or sell any

securities referred to herein. Opinions expressed are subject to change without

notice and do not take into account the particular investment objectives,

financial situation, or needs of individual investors. There is no guarantee

that the figures or opinions forecasted in this report will be realized or

achieved. Employees of Stifel, Nicolaus & Company, Incorporated or its

affiliates may, at times, release written or oral commentary, technical

analysis, or trading strategies that differ from the opinions expressed within.

Past performance is no guarantee of future results. There are special

considerations associated with international investing, including the risk of

currency fluctuations and political and economic events. Investing in emerging

markets may involve greater risk and volatility than investing in more developed

countries. Due to their narrow focus, sector-based investments typically exhibit

greater volatility. Small company stocks are typically more volatile and carry

additional risks, since smaller companies generally are not as well established

as larger companies. Property values can fall due to environmental, economic, or

other reasons, and changes in interest rates can negatively impact the

performance of real estate companies. When investing in bonds, it is important

to note that as interest rates rise, bond prices will fall. High-yield bonds

have greater credit risk than higher quality bonds. The risk of loss in trading

commodities and futures can be substantial. You should therefore carefully

consider whether such trading is suitable for you in light of your financial

condition. The high degree of leverage that is often obtainable in commodity

trading can work against you as well as for you. The use of leverage can lead to

large losses as well as gains. Indices are unmanaged, and you cannot invest

directly in an index.

Stifel, Nicolaus & Company, Incorporated | Member SIPC & NYSE | www.stifel.com |